April 11, 2025

As the Digital Finance Landscape accelerates, one phenomenon is reshaping how consumers engage with financial services: the rise of the SuperApp. These integrated platforms blend Financial, Lifestyle, and Commercial Services into a single user experience—driving higher engagement, loyalty, and digital inclusion.

According to a recent whitepaper co-authored by IBS Intelligence and Mobifin, 79% of consumers express interest in using a single app to manage daily activities, while 77% say they would increase their usage of SuperApps if a broader set of lifestyle and other needs were integrated in the same app. This shift is more than a convenience play—it’s a call for ecosystem thinking, where banks, FinTech’s, and platform providers reimagine their roles in the digital economy.

Asia has the highest number of implementations for superapp innovation. WeChat in China and Grab in Southeast Asia have evolved into multi-service platforms by embedding finance into social, mobility, and retail experiences. WeChat’s mini-program architecture allows third-party services to thrive within a single interface, while Grab’s use of operational data enables real-time underwriting and tailored micro-finance products.

These platforms show that the future of Finance lies not in isolated apps, but in integrated ecosystems—where banking is contextually woven into everyday life.

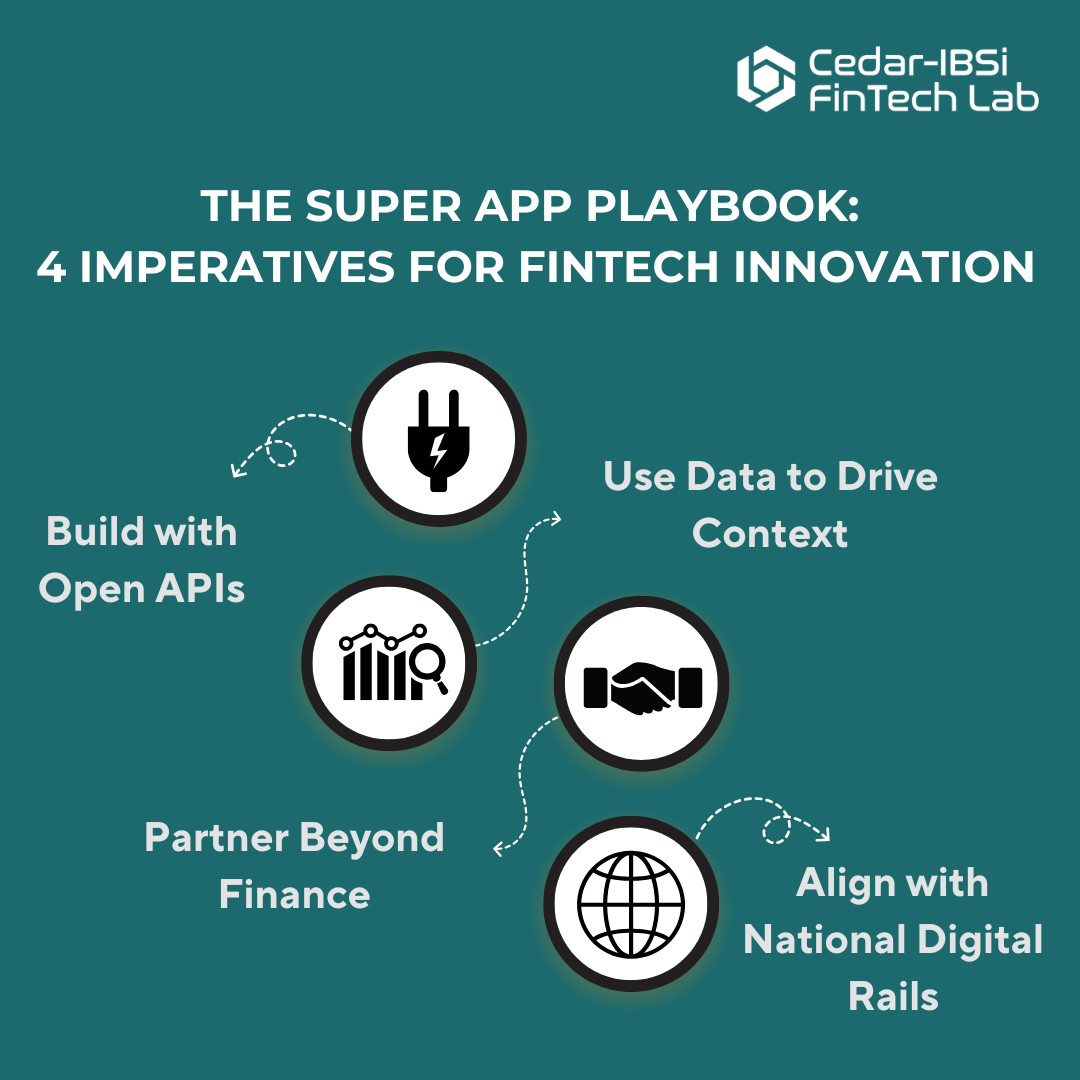

India is rapidly emerging as one of the most exciting markets for super app innovation. With over a billion mobile connections and a robust digital infrastructure, India’s FinTech growth is underpinned by a unique blend of public policy, entrepreneurial momentum, and user readiness.

The foundation lies in India Stack—a suite of interoperable public digital goods including Aadhaar (identity), UPI (real-time payments), and eKYC. These layers enable rapid onboarding, seamless compliance, and cost-efficient delivery of services across urban and rural populations.

Paytm, a frontrunner in this space, has evolved into a multi-vertical platform offering payments, lending, insurance, investments, ticketing, and commerce. Its ability to serve semi-urban and rural users exemplifies the inclusive promise of the super app model. Meanwhile, PhonePe has built a robust financial and merchant ecosystem, and Tata Neu brings cross-sector capabilities by integrating retail, travel, finance, and healthcare into a unified digital experience.

Government-led initiatives like the Digital India Mission and ONDC (Open Network for Digital Commerce) are pushing the envelope further by encouraging open-access platforms and reducing digital monopolies. This supportive policy environment has enabled India’s FinTech players to test, scale, and innovate at an unmatched pace.

The Indian model offers global players an important reference point—how digital infrastructure, when combined with agile platforms and interoperable policy frameworks, can drive both scale and inclusivity.

Markets across the Americas and Europe face more complex regulatory environments and stronger consumer preferences for app specialization. However, open banking initiatives and real-time payment systems (e.g., FedNow in the U.S.) are laying the groundwork for change.

Platforms like Revolut, Cash App, and PayPal are gradually expanding into savings, crypto, remittances, and wealth products. While they haven’t yet reached the scale or breadth of their Asian counterparts, their strategic direction signals a growing interest in integrated digital ecosystems.

The competitive advantage for banks lies beyond transactions—in creating seamless experiences that integrate finance with everyday life. It demands a platform-first thinking.

India’s FinTech landscape provides a compelling example of how inclusive growth, platform strategy, and infrastructure alignment can power the next wave of global super apps. For financial institutions around the world, the opportunity lies not in replicating Asia’s success, but in interpreting its core principles in a way that aligns with local consumer needs, regulatory frameworks, and ecosystem dynamics.