The beginning of the year is so often the time of fresh starts, new initiatives and renewed hope. But given the seismic challenge global banks face to accurately calculate how much capital is needed to shield themselves from sharp price falls, some could be forgiven for abstaining from any New Year vigour.

From January, banks have been given less than two years to iron out all the operational wrinkles (of which there are many) involved in implementing the market risk and regulatory capital rules known as the Fundamental Review of the Trading Book (FRTB). While this may seem like a way off, and while delays might occur, as they often do with regulatory timetables, one look at the scale of the work ahead shortens the timeframe somewhat. From fundamentally reorganising their trading operations to upgrading their technology capabilities and improving procedures – that’s a lot to get done.

No bank wants to start the New Year in 2020 feeling completely overwhelmed, which is why when it comes to FRTB, decisions need to be made on whether to adopt a Standardised Sensitivity-Based Approach (SBA) or Internal Model Approach (IMA). Historically, all firms with trading operations have been required to use their own internal models, due to the fact that the standard approach relied on notional instead of risk sensitivities. The problem is that under FRTB, current internal models won’t be up to scratch when it comes to enforcing the right level of capital to cope with times of stress. And let’s face it, with the geopolitical climate the way it is, trading desks may be in for more than a few bouts of stress throughout 2018.

New management structures

In order to reduce this reliance on internal models, SBA provides a credible alternative for trading desks to operate under a capital regime that is conservative, but not punitive. But those taking the IMA route will need to get approval for individual trading desks, as outlined by the European Banking Authority (EBA) recently. This presents a significant challenge as it places additional responsibility with each desk head for the capital-output, and increases the complexity of bulge bracket institutions running hundreds of trading desks. Each desk will need to put in place a management structure which controls the information driving its internal model, not to mention understand how the output can be used for risk management.

Regardless of the model banks adopt, the standard vs. IMA approach underpinning FRTB brings specific data challenges, both in terms of the volume and granularity of underlying data sets required to run risk and capital calculations, including the model ability of risk factors for IMA. This is why, regardless of the selected approach, the banks that have identified how to get the most out of their internal and external data sets will be best positioned to get their FRTB preparations off to the best possible start.

Time was when the local bank manager was a pillar of the local community, a figure of solemn solidity; trusted by his customers and potentially known to them all by name. Today, the image of the traditional bank manager seems almost as outdated as that of the village blacksmith. We live in an era of virtual shops, virtual friendships – and even virtual banks. What place has the bank manager in the digital age?

Not much, if banks themselves are to be believed. Earlier this year, Avanade released its latest report into digital disruption in the banking sector, which polled senior IT decision makers from across Europe. The poll found that almost three fifths (59%) plan to eliminate human interaction from banking service in the next 10 years.

Doubtless, some customers will see this as a long-overdue development, used as they are to a new generation of banking services delivered entirely online or through apps. Others may welcome the elimination of lengthy queues in the branch, or the lost lunch breaks spent trying to get through to a customer services representative.

Certainly, a host of digital startups and challenger institutions have begun to revolutionise our relationships with financial services providers, showing that day-to-day banking can be conducted quickly and conveniently through a digital interface. Three-quarters of respondents to our research state that their organisation is concerned about the impact that disruptive competition such as fintech start-ups are going to have on the banking sector.

Improving the customer experience with technology

As these ‘disruptors’ become popular, established banks are scrambling to reinvent themselves. Nine in ten of our respondents say they are investigating how they can use technology to improve the customer experience – an area where traditional banks admit they have fallen far behind their digital-first competitors.

As the banks embrace technology and seek to imitate their online-only and app-based rivals, it’s natural that the traditional bank branch – and the staff within – will become a thing of the past, their solid stone facades providing a perfect setting for a new clutch of trendy wine bars. Just over a quarter of senior IT decision makers from Europe say that an increased focus on digital-centric customer relationships will “inevitably” lead to the closure of some or all branches.

Is the decline of the high street bank and its manager something to be lamented? The banks will point to the immense popularity of digital financial services, and point out that eliminating the cost of maintaining a nationwide branch network can be passed on as savings to customers.

Sleepwalking towards disaster

Or is the banking sector sleepwalking towards a future where they risk sacrificing one of the few remaining unique selling points they have over their digital challengers, and merely attempting to copy what other fintech companies are already on their way to perfecting? Is it wise for them to eliminate the human touch entirely from their operations?

There are two compelling reasons why established banks should think carefully about how they can learn from the new wave of digital upstarts. The first relates to their ability to provide the same slick functionality and reliability for their digital services. Traditional retail banks are based on technology stacks that have been augmented and updated over years, yet still contain a vast amount of legacy systems that are completely unsuited to developing, testing and deploying at speed.

Of course, banks are beginning to realise that they need to replace legacy infrastructure and embrace new technologies such as the cloud. But this process will take some considerable time, during which the fintech challengers will forge further ahead with more sophisticated services, stealing, even more, market share along the way.

The second reason is that physical branches and trained, knowledgeable staff represent a unique and valuable asset – one which banks should think very carefully of consigning to the history books. In spite of the popularity of app-based services, there are some transactions that rely on human interaction – one could even say, on human relationships.

But what is the direction of travel?

Complex, high-value or long-term financial products such as loans, mortgages and investments are obvious areas where humans can make a real difference: for example, by recommending different products, discussing risks and rewards, or even just providing a commiserating explanation for why a customer has been turned down for a loan or credit card.

No-one would claim that banks don’t need to invest in new technology so that they can develop new, more relevant services for their customers. Rather, it is the direction of travel that banks need to examine. Will they profit more from slavishly copying the fintech startups or, what seems more likely, will they do better to reinvent the way they communicate with customers while retaining, where possible, the human touch?

The traditional image of the bank manager might be a thing of the past, but could there be a place for a successor – one armed with an iPad with which to talk customers through their financial future? It makes sense – in fact, you can almost certainly bank on it.

The past five years has seen an incredible rise in awareness around bribery and corruption in both the public and private sectors. While bribery and corruption detection has typically been the purview of whistle-blowers in the finance and audit areas of organisations – the era of whistle-blowers as the only ones exposing these issues is ending. Advanced analytics and other technology processes are lending support to the complicated challenge of following payments and other indicators of corruption.

Since the passage of the UKBA and other updated legislation in nearly 60-plus countries, the world has seen FIFA, Petrobras, Samsung, Shell, Rolls Royce, Unaoil, Embraer, Pfizer, and other organizations exposed for “back room” and other deals to secure multi-million and even billion dollar contracts. In 2017 alone, two companies, Odebrecht and JBS SA have both been fined over $3B a piece for bribes. What does this history of corporate malfeasance mean for the audit function at an organization?

The Audit function, both internal and external, has often been the unsung hero in the identification, investigation and subsequent alerting for many anti-bribery and corruption cases. The primary challenge that audit faces is the complex task of finding these schemes manually. This is where analytics and specialised technology can help significantly.

So how can analytics help the auditor work faster and more accurately? There are three main areas that provide benefits to the audit process:

Integrating Automation: Auditors primarily rely on their experiences to identify potential ABC issues. With the use of analytics, an organization can depend on sophisticated algorithms to detect potential problem areas by continually looking for schemes within a company’s books.

Staying Up-to-date: Criminals are always looking for new ways to push their money through the system. Analytics can learn to look for shifting patterns of unusual behaviour by a company’s vendors, customers and even employees and raise an alert to auditors before a problem may have even started.

Gathering Evidence: Auditors spend significant amounts of time gathering evidence to support a case. Analytics can significantly reduce this effort by providing continuous monitoring of transactions and quickly bringing back linked transactions related to the case.

Analytics is now viewed as a complimentary tool to an auditor’s function by reducing the time spent identifying problems, and by providing better quality alerts and cases back.

Micah Willbrand

Global head of anti-bribery and corruption solutions

Suresh Rajagopalan, President Software Products, Financial Software and Services

The Indian market is one of the world’s fastest growing economies with US$2.2 trillion in GDP but still has more than 85 per cent of personal consumer expenditure made up of cash. Despite its growing middle class and relatively strong cardholder base of 645M cardholders, debit and credit cards usage at point of sale (PoS)) is 1.7 transactions per cardholder in India.

A principal reason for slow progress towards greater adoption of electronic payments is the absence of available acceptance locations, preventing greater usage of and spending via cards. Currently, India has an approximate 2.7M point of sale devices, resulting in spotty and underdeveloped POS infrastructure coverage. Further, the acceptance network and volume that exists is concentrated in India’s primary cities, which account for an estimated 70 per cent of terminals and spend. The India Central Bank has indicated the country needs an approximate 20M POS devices to create a card acceptance infrastructure equal in size to other BRIC countries.

Overcoming barriers to developing acceptance is a key imperative for the country seeking to further expand electronic payments. Currently, an approximate 90 per cent of non-cash payments are processed through established card network infrastructures. At the heart of the traditional POS payment acceptance network is the interchange fee averaging between 0.75 per cent and 2.5 per cent —usually charged by a consumer’s bank to a merchant’s bank to facilitate a card transaction. The rate of electronic payment acceptance is low, as the high processing fee renders the value proposition non-compelling, especially for micro and small merchants, who form the bulk of India’s retail sector, and are the most important in serving low-income consumer segments.

Aadhaar Pay leverages alternate clearing and settlement rails for person-to-merchant transactions originating at the point of sale. Rather than ride on traditional card rails, Aadhaar Pay leverages the real-time interbank network for transaction clearing and settlement. By disintermediating traditional interchanges and riding on less expensive bank rails, Aadhaar-based person to merchant payments lower processing fee and promote higher merchant uptake. The service uses Aadhaar, a unique national identity number issued by the Government to every citizen based on their biometric and demographic information, as a proxy for the customer’s bank account to facilitate transactions at the point of sale.

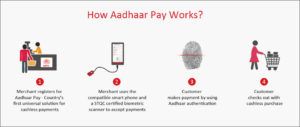

How it Works?

FSS Aadhaar Pay exploits three critical elements — bank accounts, mobility and digital identity — to disrupt traditional POS business models. The service leverages the universal availability of the mobile device and Aadhaar — India’s biometrically-enabled digital identity — that covers 99 per cent of the population to advance the growth of digital payments. Envisaged as an open platform, the Unique Identification Authority of India (UIDAI Stack), allows payment service providers to consume APIs, “on-demand” to authenticate customers. Besides leveraging Aadhaar for establishing user credentials, the national identity also serves as a financial address that can be directly linked to the customer’s bank account.

Any merchant with a biometric reader and an Android phone can download the Aadhaar Pay application, self-register for the service using e-KYC, and start receiving payments. Customers make payments by scanning the fingerprint and entering the amount at the point-of-sale (PoS) terminal. Aadhaar Pay uses Aadhaar APIs to authenticate the customer’s biometric credentials mapped to the social security number. On successful authentication, the transactions are routed to the customer’s issuing bank. In contrast to setting-up a POS terminal, which takes between two and three weeks, FSS Aadhaar Pay takes a few minutes to set-up. Further, the cost of the POS is 80 per cent lower than the cost of the conventional POS terminal.

Delivering a Multiplier Impact

Aadhaar Pay has a multiplier impact on the growth of the acceptance payment ecosystem by bringing quick-to-deploy, mobile-based affordable POS infrastructure to merchants whilst creating a seamless transactional experience for customers.

Specifically, it triggers a virtuous cycle of growth by:

Creating A Ready Market of 900 Million Captive Customers

Traditional acceptance networks need a large base of cardholders to be profitable. In emerging markets with a low base of carded users and unfamiliarity with digital payments, adoption remains slow. On the demand-side, Aadhaar Pay creates a ready addressable market of 900+ million customers by leveraging Aadhaar, as a primary transaction identifier. Customers can initiate payments using their fingerprint and Aadhaar number, eliminating hassles related to downloading multiple apps, swiping cards, remembering PIN/passwords, downloading e-wallets or carrying a phone.

Broadening the Merchant Ecosystem

On the acquirer side, Aadhaar Pay reshapes expensive acquirer distribution models by allowing banks to target previously under-penetrated micro-merchant segments with an efficient technology and commercial framework, easing the way for rapid onboarding and expansion of new acceptance points. The smallest street vendor, with the aid of a basic 2G phone and a fingerprint scanner device, can accept digital payments. To promote rapid uptake, there are no restrictions related to transaction amount, type of business, transaction volume, time, location, demography, and goods category

Offering a Low-Cost Solution

The cost of a point-of-sale (POS) terminal in India ranges between INR 8,000 (USD 120) to INR 12,000 (USD 180); countervailing duties and taxes account for about 20 per cent of the price. In addition, the annual operating cost per terminal ranges between INR 3,000 (USD 45) and INR 4,000 (USD 60). FSS Aadhaar Pay mobile application, in comparison, can be downloaded online even on a 2G Android phone, connected to a biometric reader costing INR 2,000 (USD 30). The significant reduction in Capex and OPEX makes it an ideal solution for all merchant segments, especially micro-merchants with a small turnover and low transaction volumes.

Delivering Differentiated Added Value Services

The “secret ingredient” to engineering the digital payments transformation is software. Hardware can be replicated easily, but software and services are much harder to copy, and this is where Aadhaar Pay brings a sustainable competitive advantage. Beyond the transaction, Aadhaar Pay potentially would take on a more sophisticated, innovative approach to VAS. Merchants, big or small, could benefit from a complete packaged business solution, with the ability to customize specific components. This includes:

support for QR codes

ability to dynamically configure offers and discounts

electronic invoices

analytics and reporting: to sift through payment transactions and make recommendations to merchants for optimal inventory ordering or delivering offers to customers based on buying patterns and preferences.

Settling Transactions in Real-Time

In the traditional interchange four-party payment models, settlement follows a typical T+1 cycle. Aadhaar Pay uses the bank account as a source of funds and all transactions are cleared and settled using the IMPS network (India’s real-time fund transfer network), ensuring immediate crediting of accounts, freeing funds and lowering working capital requirements for merchants.

Lowering Fraud Liability

As AadhaarPay leverages the bank account, it offers a low-risk product, with usage directly linked to the availability of funds in the customer’s account. For acquirers, there is no direct credit risk involved in processing transactions. This significantly lowers fraud liability and enables on-boarding of merchants traditionally deemed high-risk under the conventional acquiring models.

Whilst the service is in the initial rollout stages, Aadhaar Pay removes the multiple layers of friction that, merchants and customers encounter whilst making payments. For banks in India, who have recently opened Jan Dhan (no frills) accounts for the low-income demographic, a broad-based acceptance network would prevent instant encashment and improve the circulation of money in the digital format. Further, with the regulator waiving merchant fees, Aadhaar Pay would help to develop sustainable acceptance that can enhance and fast-track the benefits of electronic payments.

Taking an early lead in the market, FSS launched Aadhaar Pay in April 2017. Currently, one of India’s top merchant acquirers, with an approximate 20 per cent share of the total POS market, has implemented Aadhaar Pay.

Sources

JM Financial Report Card Penetration in India; March 2016

Reserve Bank of India; ATM POS Statistics; June 2017

World Bank, India Report — https://data.worldbank.org/country/india

Notes

A small merchant fee may be levied by UIDAI in the days ahead

Banking is steeped in tradition – particularly when it comes to image. It is hard to think of a dress code that evokes a stronger stereotype than the Gordan Gekko red braces, pinstripe suit and shiny silver cufflinks. But change is afoot, as a new wave of button-loosening fintech firms enter the market – and it is not just the dress code they are changing, it is also the old ways of working.

It is not wholly surprising that the wave of digitisation sweeping the industry has been met with a degree of caution by many senior figures. C-level execs find themselves leading new teams from a generation far more familiar with the technology, and it can be difficult to create a culture of digitisation from the top down.

Adapting to these digital changes and confronting them with efficient solutions across all lines of business is key to ensuring banks remain competitive. Bringing digital capabilities up to speed has become essential to a banks’ ability to adapt to the new market dynamic. However, the level of research and planning required to implement new services puts large banks at an immediate disadvantage. After all, the same rules don’t apply to smaller, younger, more technologically savvy companies without decades of technology debt to carry around. Moving too slow into digital may mean that the damage has already been done and the bank lost out on market share.

Integrated digitisation is necessary

Efforts to digitise can be seen across the industry – voice passwords, user-friendly apps and robo advisers are all positive steps. But for its full potential, digitisation needs to be incorporated throughout, not just in the customer facing channels. Integrating front-to-back technology frees up resources and streamlines business. Scanning paper into a PDF, for example, is not “digital” as it perpetuates content that cannot be easily processed by computers. Encouraging clients to use smart forms and submitting electronic orders, on the other hand, is clearly a better way forward. On top of this, c-level execs need to ensure that they and their employees have an understanding of new technologies while also encouraging innovation in day-to-day activities so that fluidity becomes the norm, taking a leaf out of tech giants books.

A key issue remains as to what the most effective way is to implement digital transformation. Banks who retain a quarterly ‘water-fall’ release cycles find themselves quickly behind the curve. This is why an ‘agile’ approach to IT solutions delivery and change is essential, asking project and IT operations teams to carry out small but very frequent modifications in an iterative process. This calls for a change in the business operating model, bringing the relationship and level of involvement between business and IT much closer to each other. It is a learning curve both ways and takes time to master. Business needs to accept that daily work with agile IT teams is part of their job. IT needs to learn to be much more business savvy. This is a cultural change that needs to be supported accordingly.

Modern technology is like fintech workers are to banking attire, very different from 10 or 20 years ago when many, if not most, current banking platforms were designed. The underlying database and application technologies, and the fundamental engineering behind them, have little to do with how firms such as Amazon, Google and Apple run their IT today. Few IT departments are fully up-to-date on the latest engineering options that could be used to build systems in more efficient and fast ways. As a case in point, the databases and integration fabrics underlying “big data” platforms can be used for building business applications in addition to analytics. All this requires mindset and skillset changes in IT. Going agile, without changing at least some of the technology platforms used to build and operate business applications, is akin to driving in the first gear only. You can get going, but you will not get far fast.

In this article, Fraedom chief commercial officer Henry Pooley shares his top five tips to help banks get more value from their commercial card programme.

1. Embrace Client data

If banks are going to begin to capitalize on opportunities within the fast-growing commercial banking sector, they must begin to achieve a fuller understanding and more comprehensive insight into their clients’ purchasing patterns and trends.

Client data is a tool that cannot afford to be underutilised, it allows banks to monitor parameters such as ‘Average Transaction Value’ (ATV) and ‘Spend Per Account’ (SPA), allowing them effectively to create an in-depth ‘DNA’ of each client. In turn, this enables them to identify potential commercial card opportunities and ultimately maximise the return on investment they can extract and solve any underlying issues such as high delinquency rates.

2. Simplify the payment process

By making the commercial card payment process easier and offering added value such as improvements to working capital, banks can strengthen the hand of the CFO by allowing them to clearly see the true benefits of using this method of payment – which will increase expenditure flows

Issuing banks must realise that by enhancing the technology used to support these schemes both from the end user and back end perspectives, they can help to drive up revenues.

Currently, many banks are falling short in this respect. Even larger institutions that may have commercial card programmes worth billions of pounds annually, often do not have any systems in place to analyse overall spend per account.

3. Transparency

Transparency is always highly valued, yet remains rare in the world of commercial finance. CFOs struggle to manage the constant stream of time consuming reporting techniques from different sources.

Issuers that can clearly highlight and track spending so CFOs can see at-a-glance where spend is happening, identify trends and dial up or down approval controls help deliver transparency and trust where it is most required. Payments automation and the ability to capture all spend types, not just card-based, makes financial tracking easier and more efficient, finding sources of non-compliant spend (leakage) and enabling financial directors to act quickly.

Even beyond this focus on the brand, banks have the potential to leverage enhanced technology to underpin their commercial card offerings and to use that to drive critically important customer analytics

4. Track the key metrics

Spend per account, average transaction value, operational costs and profitability are all key metrics for a bank to track to improve card delivery and performance in this area while also enhancing client engagement.

A higher SPA is likely to mean improved profitability and ROI for the issuer, greater client satisfaction with the product and better client references. Higher average transaction value (ATV) scores generally result in greater profitability for the issuer. Moreover, tracking operational costs help identify controllable costs which can be rapidly minimised without impacting service levels while monitoring profitability helps to pinpoint immediate opportunities to extend the surplus of revenue over costs.

Added to this, the technology also offers the opportunity to track further metrics from delinquency rates which if kept low offer the potential to increase issuer profitability and end user ROI to client retention which if kept high will substantially reduce costs.

5. Customers love a great experience

While technology might not be a direct selling point for any client or commercial card issuer, the associated benefits from delivering convenience, analytics, speed and efficiency cannot be underestimated.

Great experiences are as important in the B2B environment as they are in B2C sectors. If a product is easy to use and provides added value, customers are far less tempted by change. Card owners see their costs of client acquisition fall and lifetime value increase. Payments technology can deliver strong revenue growth for issuers, even within the context of budgetary constraints.

I do not pretend to be an expert in Distributed Ledger and Blockchain technology, however, I do see the huge potential in it. Although, in my opinion, currently only a select few can truly understand how the technology works and its applications, the same can be said about the internet, mobile phones and computers, back in the day. We live in an age where data is king and any move to protect that a good one, surely?

As mentioned, I do not hail from Silicon Valley and my first language is not Javascript. My job is to look and analyse investment trends and find ways to grow and protect my clients’ wealth. It is very apparent that over the last few years, cryptocurrencies like Bitcoin and Ether have been an increasingly popular ‘alternative’ to fiat currencies. It is very difficult to get the exact figures but I think it is safe to say that there have been more first-time investors, men and women who have never invested before, in cryptocurrencies than any other asset class. But do they really know what they are investing in?

The technology, and as a result, the currencies, were originally intended to form an easy way to make payments without the middleman taking a cut of your hard earned money. How long has it taken for that to fall by the wayside? Cryptocurrency exchanges are charging around 4% to buy and sell cryptocurrencies which is completely contradictory to why it was initially developed. And so begins other people making money off the back of new technology.

You may not be so lucky next time

I have seen my fair share of tech bubble bursts so am fully prepared for what is to come. I have experienced it first hand and I have to say, it is not pretty. I was one of the thousands and thousands of people who invested heavily in these new tech companies back in the late 90s and early 00s. I was also fortunate enough to have got out just at the right time because I was buying my first property. I know the signs and what I predict is a “Cryptocrash”.

The huge valuation of the currencies are not sustainable and with previous tech crashes, we have seen drops of around 90%. We have no reason to disbelieve that this won’t happen again. Mark my words – Cryptocurrency will be the next 2001 telco crash or the 2000-2002 dot-com crash. We are seeing the same symptoms – volatile spikes and crashes, huge amounts of money being invested, huge valuations. The fact that most savvy spokespeople and investors have all said that they do not know which way this is going to go should ring a few alarm bells.

Those in their 20s have never experienced a crash in the market before so they believe the hype and drive it up even more. You learn through experience in this game and the longer you go from a crisis the higher the number of market participants have never experienced a crash – this fuels the bubble further and means when the crash comes it will be much larger.

It doesn’t end with cryptocurrencies

It is not just cryptocurrencies, companies like Monzo and Revolut are developing pioneering technology but how long will they last? How long before the technology they develop is benefitted from by others? Ask Jeeves, Alta Vista, Lycos, AOL – same thing happened – the charts look almost identical to that of Bitcoin, Ether, Litecoin. The technology behind them was pioneering, however, other people benefitted from the development and where are they now?

We are living in very interesting times and are currently entering a behavioural finance phase driven by a herd mentality. This has the potential to be catastrophic but there will be lots of opportunities available. The real value and longevity is in the technology, not Cryptocurrencies. I predict the crash happening within the next 18-24 months. In the meantime, ride the wave but be prepared to cash out.

Since its invention 50 years ago in the UK and in Sweden, the ATM has become a friendly robot cashier to millions of cardholders worldwide. With an installed global base of over 3.2 million ATMs and a new one arriving about every 3 minutes, it has changed the way money is distributed and managed forever; automating cash distribution and account access on a monumental scale across all seven continents, including Antarctica.

The ATM has always been at the forefront of automation, born to provide convenience. Now it stands on the threshold of reinvention. In the next few years, the ATM will undergo an extreme make-over, from its interface to its operational software.

The core concept of ATMs is shifting from simple vending to smart banking. In an era when a leading nation like the UK has lost half of its bank branches since 1989, and with the decline in bank branch numbers accelerating since the 2008 financial crisis, the ATM needs to evolve into a branch in a box, fulfilling most of the transactions which today can be carried out in a branch, including applying for a new bank card. ATMs, in short, are becoming smart consumer banking touchpoints.

There’s a vast array of account-related functions currently available at ATMs including balance inquiries, mini statements, statement requests, account transfers, PIN management, chequebook ordering, money remittances, funds transfers (both international and national), new account opening and the securing of loans and mortgages. The ATM is well on its way to becoming a bank in a box, complete with virtual tellers connected to the customer through video conferencing. CaixaBank ATMs in Spain, for example, now offer about 200 different transactions.

I don’t think the bank branch will ever be a dinosaur but in future, there will be far fewer branches, and those that remain will be mostly smart, retail-style places with video teller services, robot-advisers, self-service devices and a handful of customer services personnel doing the high-level selling. Metro Bank, for example, often uses the term “store” rather than a branch. David Smith, Business Development Manager of Auriga, a leader in branch transformation strategies based on software re-engineering, sees these retail bank branches as essential for maintaining a relationship of trust with customers.

In this evolving context, ATMs will continue to automate convenience, becoming ever more intelligent. That’s because they will be linked to APIs (Application Programme Interfaces) and Cloud architecture, which will greatly expand the services they can provide. In addition to these powerful levels of software, there will be payment hubs to enable different kinds of payments through the ATM. There will be account management hubs where a customer can carry out a range of transactions such as managing insurance policies, mortgages, funeral policies, loans, etc. The new generation of ATMs will even be able to use AI via the Cloud to secure systems against hacking and to provide the capacity for “Big Data” analysis.

ATMs will need to stay competitive in their transaction time, especially in light of faster payment initiatives by numerous national payment systems around the world. While the ATM knows how to deliver convenience, the ATM industry is currently gearing up for increased demand for quick, efficient and convenient services in its new global initiative of agreeing to an industry blueprint for its next generation of products. I can attest that a wide degree of consensus on this blueprint among major vendors, banks and independent operators has already been reached. We foresee an increasingly interoperable API ecosystem supporting an App based model for ATMs which connect to customers through mobile devices.

While the ATM is fast becoming a Consumer Banking Touchpoint, it still carries out the original goal of its co-inventor, John Shepherd-Barron, which was to issue cash around the clock outside of traditional bank opening hours. With a bright future ahead for the ATM, and cash in circulation growing at rates significantly higher than average GDP rates, cash is definitely isn’t going into the museum in this generation or the next.

by Michael Lee, CEO of ATMIA and Full Member of the Association of Professional Futurists (APF)

Most success stories around Robotic Process Automation (RPA) are larger than life: cost savings of 60 to 80 per cent, projected ROI in three digits, or turnaround times that go from days to minutes. But there is a flip side to consider: 30 to 50 per cent of initial RPA implementations fail.

In the financial services industry and in other industries, the reasons for the underwhelming performance of RPA range from lack of scalability and excessive reliance on IT to inadequate preparation to unrealistic expectations and short-term thinking. Also, a big problem is that enterprises often choose the wrong processes for automation.

Still, the financial industry is understandably excited. According to arecent global study, 33 per cent of major enterprises, and 44 per cent of banking and financial services companies, have committed serious investments in RPA within the next two years.

Implementing RPA in large financial services organisations takes careful consideration and diligent planning. The following is a list of top ten tips for selecting processes for RPA to help guide financial services organisations to successful implementations:

Assess processes consistently across the enterprise: rather than shopping for use cases at random, enterprises should employ a standardised, “top down” process hierarchy to assess the right candidates for automation.

Estimate effort accurately: enterprises should base their business case for RPA on current and accurate data on the effort, number of steps, and manpower needed to complete different processes. This assessment relies significantly on inputs from process subject matter experts, and would also benefit by factoring the results of time and motion studies, activity based costing, and average handling time/ effort analysis.

Minimise process variation: a number of RPA implementations go over budget and miss deadlines because processes vary so greatly. Financial services organisations should address that by mitigating the usual causes, such as multiplicity of systems and interfaces; variation in the extent of process centralisation across different country operations; proliferation of country-specific processes shaped by legal or local requirements; and lack of standardisation in the formats and processes employed by different vendors.

Build a solid business case: broad brushstrokes and gut feel have no place in process selection. Rather, the decision should be grounded in a comprehensive business case, which takes all costs, benefits, complexities (e.g. number of systems, data types etc.) and risks (e.g. legal, regulatory etc.) into account.

Factor in other strategic technology and business programs: large organisations have many simultaneous digitisation initiatives, which may impact some of the processes selected for robotic automation. It is vital to take that into consideration before going ahead with RPA.

Think end-to-end: in RPA, the sum is greater than the parts. When assessment is conducted in silos, a process that occurs in or draws data from two or more functions is in effect treated as two (or more) separate processes. This is suboptimal from an automation standpoint. For example, a key process called balance sheet control is part of the financial controller’s domain. However, to make up the balance sheet account totals, the process needs transaction data from other functions, which is sent to the finance team for reconciliation. An organisation trying to automate ledger “proofing” without an end-to-end view will automate only the activities of the finance function, leaving all the feeder activities in the other functions to be performed manually or automated in a separate exercise.

Measure complexity, so you can manage it: since no two RPA use cases are of the same complexity, enterprises cannot base their calculations on general assumptions. They should create a continuum of activities that are graded by complexity to assess feasibility and decide priorities.

Include solution analysis in process assessment: after assessing the complexity and nature of a use case, the organisation should analyse the various solutions available to identify an appropriate toolset. This has a direct bearing on the business case since implementation costs and timelines vary by tool.

Review and redesign: walking through a process will help to identify its pain points. The enterprise should then try to determine the “dominant root cause” of each before proceeding to redesign the post-RPA process. For instance, are pain points caused by policy and procedure, organisation design, or poor error detection.

Perform assessment in “sprint” mode: often, organisations try to complete the assessment and identification of use cases in a single iteration, which creates a long gestation period until implementation by which time the opportunity might have stalled or the process itself might have changed. There is also a risk of misinterpreting or dropping information required for the implementation. The ideal approach is to take up RPA in “agile mode” – maintaining a process backlog that allows the development team to plan for the next few sprints as well as account for any feedback from the previous iteration.

Here’s an example of a large financial services company, which turned around an RPA implementation that was headed nowhere. The company’s shared services unit had run into serious problems with its robotics-led initiative, which had not operationalised even a single process yet. The reasons for this included wrong selection of processes, unrealistic cost saving expectations and a team that was totally unprepared for the job.

The company then with some help from external partner set out to define the right RPA demand generation model, compute the business case, design the post-implementation operating model and flows, and execute the project in agile mode. Thanks to this exercise, the unit now has a clear line of sight into RPA backlog and a sound business case. Having found the right RPA solution, it is now implementing several RPA projects and is on the way to meeting its cost saving targets.

Following as many of these tips as possible, financial services organisations should identify the right automation tool and partner to achieve their goals.

Ten Nepal-based bank have signed up to use SWIFT’s Sanctions Screening service to underpin their sanctions compliance. The banks join a group 600 strong, built up since the service’s launch in 2012 as the first of SWIFT’s financial crime compliance portfolio.

Sanctions Screening is a hosted utility service that screens financial transactions in real time, according to SWIFT. It holds information up against “more than 30 up-to-date lists of sanctioned individuals and entities from all the major regulatory bodies, including OFAC, the United Nations, and the European Union.”

The service is aimed at small and mid-sized financial institutions as well as corporations and payments businesses.

“SWIFT is a valued and trusted partner in our sanctions compliance efforts,” says Ashoke SJB Rana, Chief Executive Officer of Himalayan Bank Limited, one of the banks to sign up. “Using Sanctions Screening helps us focus on core parts of our business while actively ensuring we are meeting our sanctions compliance obligations, reducing manpower and costs.”