During the height of the crypto boom, everybody from Paris Hilton to the Venezuelan government seemed to be either setting up or promoting ICOs as token values skyrocketed. Even ICOs that were blatant jokes like the Useless Ethereum Token reportedly raised $200,000. Those days are over.

The crypto winter has given the blockchain sector the opportunity to step back, take stock, and mature. In this market, only blockchain firms with a solid business case and sound tokenomics will attract investment. Here are 5 things you need to know to run a successful blockchain start-up:

1. Think about whether you really need blockchain or whether your project could be implemented more efficiently with a conventional database. The most important consideration here is whether trust between users is a major concern. In a field where immutable, time-stamped records are important to all parties, like supply chain management or legal data storage — blockchain could be useful. If you plan to deploy the system internally within an organisation, a normal database would probably be better.

2. Develop a compelling value proposition. Remember that most people don’t care about blockchain technology as much as you do. Many blockchain startups fall into the trap of being too tech focussed and forgetting about the customer. A good value proposition should clearly state who your target market is and how your product will help them.

3. Create a roadmap that sets out how you will scale your project. It is great to dream big, but think about whether your user base will need to reach a critical mass before your platform is useful. If so, you will need to establish a compelling reason for early adopters to come onboard. This may involve altering your business model in the short term to create incentives for users to adopt your technology while the user base is smaller.

4. Think about whether you really need a utility token or whether a security token would be more appropriate. A utility token needs to play an integral role in the future operation of your platform. Don’t try to shoehorn a utility token into a preconceived business model: if you just want to raise capital, issue a security token instead.

5. Simplify your tokenomics. The speculative bubble is over. Investors will only invest in an ICO or STO if the token is clearly linked to a useful digital service or underlying asset. Less is more: your white paper needs to be simple, clear and explicit about the link between the token and its underlying value.

By Mattias Hjelmstedt, CEO and Co-founder of Utopia Music, blockchain-powered music tracking and attribution platform, which was recently ranked among the 15 new companies in the Crypto Valley Top 50.

Digitalise or die. It may not be such an overstatement considering the current state of the banking industry. Banks have been getting on the digital bandwagon for over a decade now. However, with the ever-evolving technology and the fintech start-up revolution, the role of digital technology has changed from a good-to-have to a must-have. Last year was particularly notable in this respect, with technology investment by banks reaching a maturity that was not seen until a few years ago.

Large global banks jumped headlong into their automation and artificial intelligence-related initiatives. Many of the larger banking groups such as Citi, Morgan Stanley, US Bancorp, HSBC, Deutsche Bank and so on have reportedly set aside dedicated funds in the range of $2-$4 billion for digital platforms and technology innovations. JP Morgan reportedly had a tech budget for 2018 of $10.8 billion, with $5 billion set aside for new investment majorly into AI. There was a marked rise in Core Banking modernisation and digital banking solution sales in the US, especially within community banks and credit unions indicating that even mid-sized banks were getting serious about executing their digital strategy.

Investments in last year’s much-hyped blockchain technology saw a long-expected correction with banks and governments alike realising that the real applications of distributed ledger technology were beyond cryptocurrency trading and dubious ICOs. It was no surprise then to see the price of bitcoin crashing from last year’s intraday peak of $20,000 to as low as $3,500. On the flipside, the year saw increased collaboration within banking associations to develop practical applications of blockchain in areas such as trade finance and so on. Of note was the European Commission launching its own blockchain initiative in order to develop a common approach on blockchain technology for the EU with participation from major banks such as Santander and BBVA.

However, the most notable of all the developments this year was the Open Banking PSD2 regulation that became effective in January. With this, the stage is set for the rise of true marketplaces and APIbased

banking systems. Considering the major developments discussed above, much of the technology investments trends in 2019 are bound to be dictated by cascading effects of last year’s developments. For banks, strengthening their competitive positioning will be the primary driver for investing in technology. On that note, some of the key banking technology investment areas that are likely to be in the limelight next year are as follows:

1. Open Banking and rise of marketplaces: The Payment Services Directive 2 (PSD2) was singlehandedly responsible for springboarding the Open Banking culture within the banking industry and forcing banks to open up their systems to fintech. Being a regulatory requirement, with deadline for compliance to the technical standards set at September 2019, most European banks will be focusing on upgrading their systems to be compliant with PSD2 requirements. There is also a major initiative among the larger global suppliers that are developing fintech marketplaces and partnering with smaller fintech start-ups in order to offer a one-stop solution for an API-ready bank industry.

2. Greater emphasis on regtech: 2018 was an eventful year for banks regulatory wise, with PSD2, GDPR and MiFID II all coming into effect in the same year. Compliance and regulatory reporting requirements left banks scurrying for quick-fix compliance solutions that they could implement without too much investment. These solutions offered by large global suppliers as well as specialist niche suppliers will continue to be in demand even in 2019 as banks ramp up their systems and look to remain compliant.

3. AI and automation: While large banks have already been intensively focusing on developing automated solutions using AI, the technology itself is far from being perfected. As this solution gets developed further, the applications of AI are also expected to grow exponentially. Almost all the large banks now have deployed a virtual assistant that uses machine learning and predictive analytics. In 2019, one can expect banks to invest further in enhancing their chatbots, making them more intelligent and integrating them with all their services. Small and mid-sized firms are also going along the automation path, but the solution of choice for them is likely to RPA which are the first steps towards automation without the need of complex requirements of an AI deployment.

4. Cybersecurity and fraud management: The challenge with large scale digitalisation, API banking and third-party collaboration is the increase in the vulnerability across the banking ecosystem to potential data breaches. The recent HSBC data breach at its US business is only one such example. To make a successful transition towards a digital economy and digital banking will mean that banks and their partners will together have to invest in robust fraud prevention and cybersecurity solutions. This is likely to be the most critical technology investment banks would have to make in 2019.

5. Digital-only banking platforms: For many of the banks across the globe, the Core Banking systems currently in use are as old as 30 years with heavy customisation, which make upgrading their Core Banking system a daunting task due to cost and manpower involved. The recent TSB debacle was a prime example of how badly a complete Core Banking system overhaul could go wrong. Most industry experts are averse to the idea of a complete overhaul and instead recommend a piecemeal approach starting with one process, one product, one function at a time while maintaining the overarching focus of building a customer-oriented digital infrastructure. A popular strategy that is increasingly prevalent among larger banks is to build a separate digital-only bank that can cater to the digital savvy customers. Examples of this approach are seen around the world – JP Morgan with its mobile banking platform Finn in the US, Santander with its digital-only bank Openbank in Europe, Standard Chartered with a retail digital-only bank in Africa, DBS with online bank Digibank in India and Commercial Bank of Dubai with CBD Now in the UAE. This is likely to be the trend even in 2019, especially with the success of incumbent banks and digital-only challenger banks.

The banking industry is replete with digital transformation initiatives and this will continue even in 2019. Besides the areas highlighted above, there are numerous other technology initiatives that are being pursued on a smaller scale but are likely to come into focus in the future, depending on their disruptive capabilities. However, these technology investments are, as with any other investment, impacted by the macroeconomic factors – the Brexit outcome and the US-China trade wars are among some of the factors that will play a decisive role in the quantum of technology investments that banks are able to make in the next year.

Data is widely acknowledged to be one of the business’ most valuable assets. Yet even data can depreciate in value. Like currency itself, it is always changing and evolving with new types appearing. Just as the financial industry has witnessed the rise of alternative and cryptocurrencies, businesses are trading on a recent boom of new forms of structured and unstructured data. Whether it has been digital or voice, every time a new channel is created a new kind of data is born alongside it.

Yet this has consequences for the data that came before, and for the businesses that continue to store it. As technology advances, old data gets harder to read and slower to utilise. Eventually, it becomes obsolete and less care is taken to properly manage it. Once it has fallen off the radar, we call it dark data. When data goes dark, conditions can become very dangerous for an organisation. To overcome this challenge, financial services companies will need a more strategic approach to data management and an increasingly robust use of technology.

The dark age of financial data

From the days of the earliest banks, financial services companies have always used data to improve and streamline the customer experience. We have come a long way from personal customer information written on paper documents, to credit scores, purchase histories and the telematics data used by an increasing number of insurance companies. Yet, this long history of data collection is part of the problem.

As financial services companies evolve, old data loses its strategic and business value – going dark. With today’s limitless cloud storage systems, it is far easier to make use of digital data than it is physical written records. Inevitably, the latter is filed away and eventually lost. Yet dark data never completely goes away.

Financial services companies are particularly vulnerable to the rise of this dark data. Indeed, the industry holds huge backlogs of stale data, 20% of which are made up of old document files. As smart contracts and blockchain transactions grow in popularity, this type of old data is rapidly losing its relevance and value.

The financial services industry’s heavily regulated environment is partly responsible for creating a culture that is cautious to delete anything. The result of this ‘save everything often’ mentality is that old data takes up valuable storage space.

The out of sight, out of mind nature of dark data also means it stops being properly managed, maintained and protected. Over time, this can pose a major security risk to financial services companies and their customers.With data privacy regulations like GDPR now in effect, consumers are more likely to take action against irresponsible financial services firms than any other sector, so dark data represents a ticking time bomb for data security.

How good data dies

To fight the dark data problem, businesses must stop it at its source. Ultimately, dark data stems directly from a lax data management strategy. This is not a new phenomenon; indeed, it has long been an aspect of development culture in financial services. Historically, mainframe systems were siloed and when a new application was to be built it would be done in a separate environment. Unsurprisingly, the data these companies hold is now spread across many different databases found in the cloud and on-premises.

When data becomes dark, it is not because of negligence but the complexity of keeping it organised in deeply fragmented IT environments. Research shows that employees regularly struggle with an overabundance of data sources and tools, as well as a lack of strategy and backup solutions. According to our research, the majority (81%) of organisations think their visibility and control of data is unsatisfactory and even more (83%) believe it is impacting data security. Not only is this fueling the rise of dark data, but it is also hurting the ability of employees to find and utilise valuable data, resulting in missed business opportunities and wasted resources.

A better way to manage data – Creating a data management strategy

As data becomes more siloed and fragmented, it is harder to find, manage and protect. This is how dark data turns into a risk. To stop this happening in the first place, financial services companies must create data management strategies that accommodate both recent and obsolete data. At the same time, they have to resist the temptation of a ‘save it all’ strategy. Instead, they should take advantage of new tools and platforms that can locate, automatically classify and manage data across multiple environments.

Introducing and enforcing data management policies

Data management policies should be put in place and enforced from the bottom to the top. This means everyone knows what the data types and formats are and where they should be saved at all times. But it is equally important that these boundaries are not too restrictive. Data is changing all the time, so standards too will need to adapt. Employees should be allowed some freedom of action as long as they stay within the goal posts.

Using the right technology

Financial services companies should also be willing to adopt data management technologies for increased efficiency and protection. A single, unified data management platform can make use of intelligent automation, helping employees locate the data they need faster. This not only makes data less likely to become dark, it gives the company a strategic edge and the ability to make better business decisions faster.

It is not only old, established players that should fear the rise of dark data. Disruptive payments providers and challengers may be on the cutting edge now, but they are just as subject to time and the depreciation of data. Finding new ways to utilise and safeguard data is at the heart of digital transformation. It is the key to creating opportunities and value for a business. Good policies and a structured, automated approach will not only prevent the rise of dark data in financial services but also help financial services companies truly harness the power of their data.

Having positive cash flow is a must for any business. Get it wrong and you put the existence of the entire organisation in jeopardy. Get it right, however and you open up a wealth of new opportunities for your company from unlocking new business deals to driving incremental revenue streams and fuelling investment.

Often, the blame for poor cash flow is laid firmly at the foot of traditional banks for not agreeing to extra lending rapidly enough. That can be a contributory factor, of course, but the real scourge is not keeping a tight rein on spending and not developing, or sticking to, accurate forecasts.

To ensure their cash flow remains healthy, businesses need a single point of visibility over all the money going in and out of their accounts. Without this, it will be difficult for them to make informed financial decisions or to plan ahead efficiently and effectively. However, enhanced cash flow visibility is not always easy to achieve.

Organisations typically make use of multiple different payment types from credit cards to cheques to bank transfers – and often have no clear overall picture, either at a snapshot level or historically, of all the transactions they are making. Often, they are using outdated methods of dealing with payments, expenses, invoicing and reporting, or, worse still, have no planned approach. All this slows down the ability for the business to react, to access revenues and redistribute in the event of unforeseen circumstances. It also offers little in terms of up-to-date analysis.

This is why integrated payment management or consolidation is critical to businesses that want real time visibility of their expenditure and the kind of insight into cash flow that drives long-term business success.

Empowered to Spend

The concept of integration is a familiar one, of course. Enterprise Resource Planning (ERP) systems have been around for decades now. ERP, and variations on the theme, is now a ubiquitous technology across large corporate enterprises and increasingly across SMBs also.

Yet at the same time as this enhanced level of control was being exerted on back-end processes, we also witnessed a counter trend where employees were armed with credit cards and cheque books and empowered to make significant business purchases.

This has clearly helped drive operational flexibility and business agility. But more important still, it has driven cash flow which remains key for any business today. So, more businesses will be looking to leverage lines of credit and tap into free funds for a period to help with cash management. This will make it even more vital that businesses have real time insight into all this activity.

The best way to achieve this is through a digital expenses platform and integrated payments tools, both of which should almost by default improve a business’s approach to how it manages cash flow. By having an immediate oversight through live reporting of all spending from business cards and invoice payments, as well as balances and credit limits across departments and individuals, organisations can foresee potential problems more quickly and react accordingly. At Fraedom, we provide this kind of technology to many of our customers across banking and financial services sectors.

Digital trail for reporting

This kind of approach also allows management to categorise spending and quickly see where costs are getting out of control or where they need to put in place cash flow targets to help ensure solvency. Cards can be cancelled or at least suspended quickly and easily, negating the need of having to go through to the issuing bank, while invoices can also be automated to streamline business payments. This enables business to keep hold of money longer and pay creditors faster.

Moreover, digitally transforming business expenses and payments, encompassing everything from receipt capture through to automated payments and invoicing, means there will always be a digital trail that can be collated and reported on quickly and easily. This also means that at any moment in time, management can use fresh data to accurately forecast cash flow, which in turn helps eliminate nasty surprises and should also lead to fewer business failures.

The ongoing digitisation of systems is also likely to result over the long term in greater take-up of emerging trends in artificial intelligence and analytics-driven technologies. In turn, this will help organisations more accurately predict their future spend, thereby giving them early insight into potential upcoming cash flow issues and enabling them to look ahead into what may be happening in the market moving forwards.

It’s another example of how technology can play an important role in helping businesses gain more insight into their cash flow and better manage their cash in general. If they get that right, they are likely to access new investment opportunities; drive competitive edge and survive and thrive both today and long into the future.

by Russell Bennett, chief technology officer, Fraedom

Personal identification numbers (PINs) are everywhere. These numeric versions of the password have been at the heart of data security for decades, but time moves on and it is becoming evident that the PIN is no longer fit for purpose. It is too insecure and is leaving consumers exposed to fraud.

Why bin the PIN?

In a world that is increasingly reliant on technology to complete even the most security-sensitive tasks, PIN usage is ludicrously insecure. People do silly things with their PINs; they write them down (often on the back of the very card they are supposed to protect), share them and use predictable number combinations (such as birth or wedding dates) that can easily be discovered via social media or other means. And this is entirely understandable: PINs must be both memorable and obscure, unforgettable to the owner but difficult for others to work out. This puts PIN users — all of us, basically — between the proverbial rock and a hard place.

Previous research has shown that when people were asked about their bank card usage, more than half (53%) shared their PIN with another person, 34% of those who used a PIN for more than one application used the same PIN for all of them and more than a third (34%) of respondents used their banking PIN for unrelated purposes, such as voicemail codes and internet passwords, as well. In the same study, not only survey respondents but also leaked and aggregated PIN data from other sources revealed that the use of dates as PINs is astonishingly common1.

But if the PIN has had its day, what are we going to replace it with?

Biometrics

Biometrics may seem to be the obvious response to this problem: fingerprint sensors, iris recognition and voice recognition have all been rolled out in various contexts, including financial services, over the past decade or so and have worked extremely well. In fact, wherever security is absolutely crucial, you are almost certain to find a biometric sensor — passports, government ID and telephone banking are all applications in which biometric authentication has proven highly successful.

However, PINs are used to authenticate any credit or debit card transaction, and therein lies the problem. For biometric authentication to work, there has to be a correct (reference) version of the voice, iris or fingerprint stored, and this requires a sensor.

It is one thing to build a sensor into a smartphone or door lock, but quite another to attach it to a flexible plastic payment card. Add to that the fact that cards are routinely left in handbags or pockets and used day in and day out, and it becomes clear why the search for a flexible, lightweight, but resilient, fingerprint sensor that is also straightforward enough for the general public to use, has been the holy grail of payment card security for quite some time.

Another key advantage of fingerprint sensors for payment cards is that the security data is much less easy to hack, particularly from remote locations, than is the case with PINs. Not only are fingerprints very difficult to forge, once registered they are only recorded on the card and not kept in a central data repository in the way that PINs often are – making them inaccessible to anyone who is not physically present with the card. In short, they cannot be ‘hacked’.

Your newly flexible friend

Fortunately, the long-held ambition to add biometrics to cashless transactions has now been achieved, with the production and trials of an extremely thin, flexible and durable fingerprint sensor suitable for use with payment cards. The level of technology that has been developed behind the sensor makes it very straightforward for the user to record their fingerprint; the reference fingerprint can easily be uploaded to the card by the user, at home, and once that is done they can use the card over existing secure payment infrastructures — including both chip and ID and contactless card readers — in the usual way.

Once it is registered and in use, the resolution of the sensor and the quality of image handling is so great that it can recognise prints from wet or dry fingers and knows the difference between the fingerprint and image ‘noise’ (smears, smudging etc.) that is often found alongside fingerprints. The result is a very flexible, durable sensor that provides fast and accurate authentication.

The PIN is dead, long live the sensor

Trials of payment cards using fingerprint sensor technology are now complete or underway in multiple markets, including Bulgaria, the US, Mexico, Cyprus, Japan, the Middle East and South Africa. Financial giants including Visa and Mastercard have already expressed their commitment to biometric cards with fingerprint sensors, and some are set to begin roll-out from the latter half of2018. Mastercard, in particular, has specified remote enrollment as a ‘must have’ on its biometric cards, not only for user convenience but also as means to ensure that biometrics replace the PIN swiftly, easily and in large volumes2.

And so, with the biometric card revolution now well underway, it is time to say farewell to the PIN (if customers can still remember it t, that is) and look forward to an upsurge in biometric payment card adoption in the very near future. Our financial futures, it seems, are at our fingertips.

I began this three-part series on 871(m) by quoting one of America’s most famed political characters and Founding Father, Benjamin Franklin. In order to round this series off in the same fashion, I’ll turn to another American political figure, this time: Abraham Lincoln. He was once quoted as saying “you cannot escape the responsibility of tomorrow by evading it today”, which I think quite accurately summarises the mantra that banks should be taking when it comes to 871(m), Transaction Tax processing and looking to the future.

So where do we stand currently with 871(m)? Banks must comply with the first part in the here and now and although the second part may still be under review, there’s absolutely no indication that the rule will be dropped in totality. I stand by what I said in the first blog – if banks are to wait until the full outcome of the review, they will only open themselves up to a plethora of problems later on. Banks do not want a repeat of five years ago, when they decided to implement tactical solutions for the French and Italian Transaction Taxes.

Of paramount importance for preparing for a post-871(m) world is that banks have software in place that can assist in facilitating a flexible ‘rules-based’ workflow solution which can easily adapt to changing legislation. From our extensive investigation of the intricacies of this, and other regulations which are on the increase, we found that due to the complexities of all, it makes little sense for firms to have multiple interfaces with the same derivatives and trading systems going to siloed tax solutions e.g. an FTT system in one place and an “871m machine” or system in another place.

It, therefore, makes much sense to feed it all into one solution and processing engine, rather than having a whole host of separate systems and trying to interface them all, which leads ultimately to more static, more cost and more fails (i.e. transactions). By taking a centralised or utility approach, banks are also in a good position to deal with even more potential incoming Transaction Taxes which is key in preparing for the future.

A resourcing and knowledge challenge

Alongside the need to assess which systems will be best placed or built to cope with 871(m), there are significant amounts of data that need to be pulled together, including dividends and trades across many different instrument types, potentially creating large integration projects for in-house teams. Place these needs against the backdrop of other current in-house IT initiatives that banks are aiming to achieve regulatory compliance with, and it becomes an even more complex resourcing and knowledge challenge.

Unfortunately, 871(m) is just one of many tax headaches facing banks, and more are certain to crop up further down the track. This is why taking a ‘future-proofing’ mentality is key here. Platforms and technology need to be fit to cope with other incoming regulations, so banks need to look at who can help them overcome these compliance headaches and who can demonstrate that they truly understand the needs and will provide “safety in numbers” when the regulator “comes knocking”.

871(m) won’t simply disappear by not thinking about it now. It’s the banks’ responsibility to prepare for the tax world of tomorrow, today.

By Daniel Carpenter, head of regulation atMeritsoft

Chris Rauen, Senior Manager, Solutions Marketing at SAP Ariba

If you have an electronic invoice system that just about meets the needs of the accounts team, but operates in complete isolation from the rest of the company, is that a system that provides much value?

It might do — if you’re doing business in the 1990s. Since then, a plethora of electronic invoicing systems have entered a crowded marketplace, all looking to streamline the complex way of processing invoices globally.

In today’s digital economy, new business value comes from linking invoice data to contracts, purchase orders, service entry sheets, and goods receipt for automated matching. Furthermore, automation of the invoice management process must extend beyond enterprise operations to include suppliers. Yet few platforms enable this. By treating accounts payable as a department, many e-invoice systems fall short of their potential.

So, how can linking electronic invoicing with a company’s other operational systems, and to suppliers, unlock this value? It turns out that an interconnected approach to invoice management in a digital age reduces costly errors, strengthens compliance, and facilitates collaboration both within the organisation and among trading partners.

A cloud-based network can assess trading partners against hundreds of criteria, including whether they can root out forced labour from their supply chain to how well they document the use of natural resources, and even giving work to minority suppliers. Of course, while software alone cannot ensure compliance with the ever-changing policies that continue to come into effect, it remains a powerful tool towards efforts in achieving it. Compliance, once a tedious task, now can be managed from a dashboard.

To reduce invoice errors effectively, a digital network must rely on intelligence — not just the human kind, but through smart invoicing rules that are essential to a business network. These rules effectively validate invoices before posting for payment to streamline processing, reduce operating costs, lower overpayment and fraud risk, and maximise opportunities for early payment discounts.

By enabling real-time collaboration between buyers and suppliers, digital networks not only bridge the information gap that can delay invoice processing, but they also reduce the complexity often associated with compliance. That includes effectively screening suppliers and monitoring business policies automatically before a transaction takes place.

However, perhaps the greatest advantage of digital networks is collaboration. Issuing an invoice, even when accurate and on-time, can sometimes be a one-way, asynchronous conversation. A buyer receives an agreed-upon product or service from a supplier, who at a later date sends out an invoice and, at an even later date, receives payment. This scenario has been the same for decades. But digital networks challenges that. The immediacy of network communications begs the question: Should electronic invoicing merely replicate the age-old process that postal mail once facilitated? Or shall it improve upon it?

We continue to see chief procurement officers choosing the latter. Through their day-to-day experience with digital networks, they have come to view invoice processing as just one part of the wider exchange of information among trading partners. An electronic invoice reflects a snapshot of the multi-party collaboration that networks enable, and — through intelligent business rules — alerts of potential errors or exceptions relating to the transaction. As we move forward in the digital age, and buyers and suppliers extend their relationship to include product design, innovation and product delivery, they are able to expand the scope of electronic invoicing to capture up-to-the-minute progress reports on the teamwork within and across organisations.

Ultimately, your electronic invoicing system shouldn’t focus only on accounts payable, it should give open visibility onto the rest of your operations and even who you do business with – so that mutual growth can be achieved and positive collaboration can flourish.

The author is Chris Rauen, Senior Manager, Solutions Marketing at SAP Ariba, the company behind the world’s largest business network, linking together buyers and suppliers from more than 3.4 million companies in 190 countries

Buzzwords such as ‘Artificial Intelligence’, ‘Machine Learning’, ‘Chatbots’ and ‘Robo-Advisors’ are rather ubiquitous among bankers and non-bankers alike. They are prominently echoed in boardrooms and earnings calls of large corporations, and increasingly feature in their quarterly reports. A few years ago, these ideas were merely discussed and not much was done to act on any of them. This could either be because of the lack of knowledge regarding the potential benefits these new technologies brought in, or because of the supposedly more important ‘strategic’ initiatives piled up on the desks of top management. This attitude has significantly changed over the past few years – one can notice a tectonic shift in the adoption of disruptive technologies for streamlining business processes, and in turn reducing costs and increasing efficiency. Large enterprises are implementing sophisticated solutions to internal processes, as well as to customer facing services, by using automation to replace repetitive, human tasks.

One such improvement in recent years has come in the form of Chatbots. The word ‘chatbot’ is a beautiful amalgamation of two of mankind’s most recent obsessions: messaging (chat) and robots (bots). Until recently, chatbots featured more in science fiction than in the real world. Few were able to fathom the explosive growth that was to occur. With the introduction of Siri, Alexa, and Google Assistant a few years ago, this bit of science fiction became a reality.

Chatbots are software programs that use real-time messaging as an interface. With extensive, and precise mapping of (potential) conversations, chatbots pose a serious threat to the age-old concept of a contact center. We now live in an instant gratification society, where waiting for an attendant at the opposite end has become a hindrance. In a world inhabited by digital natives, EVERYTHING IS INSTANT; from Instant Coffee & Noodles, to the more recent, Instant Customer Service. Chatbots are trying to address the latter, by providing real-time responses to customer queries. Be it rule-based or AI-driven, chatbots are slowly becoming the preferred form of communication for customers of all ages.

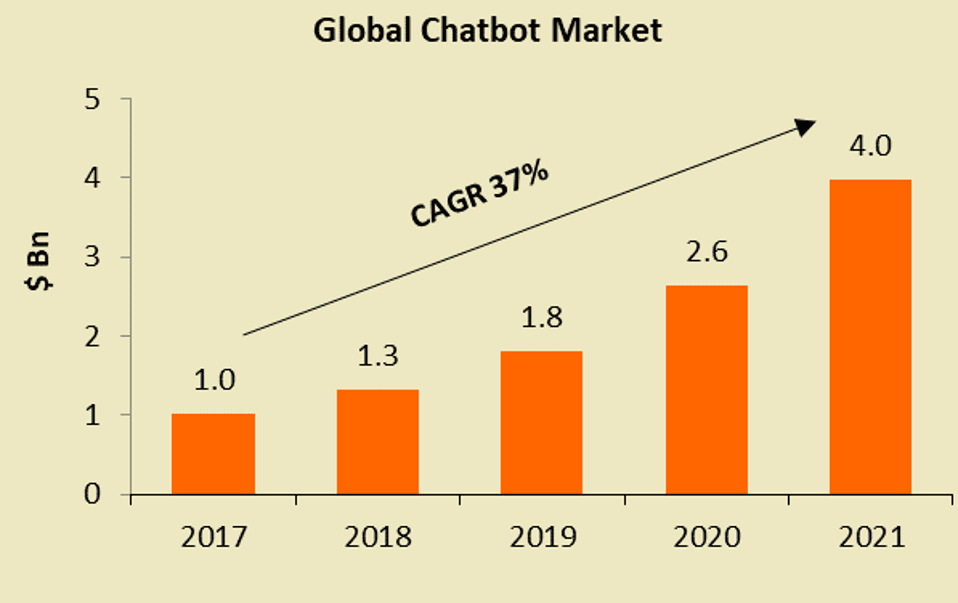

As a market valued at a little over $1 Bn in 2017 and predicted to reach $4 Bn by 2021, chatbots are set to grow at a CAGR of 37% over the coming 4-5 years. Looking at India for instance, in 2017, there were over 150 million users of messaging apps. This number is expected to grow at a CAGR of 17% over the next 3-4 years to 231 million users. With such rapid growth expected, companies are poised to ride the ‘chatbot’ bandwagon. This growth is driven by an increasing number of users relying on messaging apps, such as Facebook Messenger, Slack, and Telegram. In terms of cost reduction, chatbots will be responsible for annual savings of ~$8 Bn by 2022. And in terms of increased efficiency, a chatbot inquiry will save more than 4 minutes per call in comparison to traditional call centers. Is it surprising then, that enterprises are increasingly moving towards chatbots to reduce costs?

For any company, cost reduction and increased efficiency are in fact, imperative to its bottom line. What a chatbot, an automated chat interface, brings to the table is the ability to replace archaic contact centers, with a modern, instant service platform, at a fraction of the cost. A testament to the growth of messaging apps, and in turn to the rise of chatbots, is in its popularity; the top messaging apps garner a larger daily/monthly audience than the top social networks.

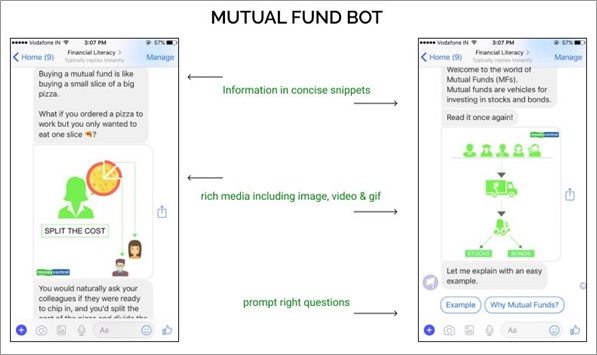

Translating this growth into tangible results for the financial services industry, is what many institutions are trying to unravel. Selling financial concepts is difficult, not because of the competition, but because of the prevalent status quo of doing nothing. There is a ton of information available, but this information is not designed to be digested by millennials, as well as by senior citizens. This is where Chatbots jump in! They can be positioned as utility tools to promote ‘Financial Literacy’, and disseminate information based on customers’ needs. For e.g., a Brokerage house can use chatbots to ‘educate’ new/existing users about the convoluted world of equity markets. Using an automated chat interface, complex financial terms and concepts can be simply explained, even to a novice. Typically, a chatbot determines the suitability of a product for a customer by assessing the financial health of his/her portfolio, along with the respective goals. The chatbot then recommends what products the customer should invest in, and what proportion of his/her wealth should be invested in different product types. The core objective is to empower the end user, who can then make informed monetary decisions after thorough assessment of the relevant products. The idea is to systematically break down complex financial content into conversational snippets within a chat interface. The content should be designed to enable the user to understand concepts and financial processes with ease, so as to bridge the gap in his/her understanding.

Source: Mpower.chatLet’s take Mutual Funds as an example. In India, Mutual Funds are becoming commonplace, given that they strike the right balance of being highly profitable, yet relatively safe. The share of MFs in the overall asset pie is increasing. There are numerous first-time investors looking to channel their moderate savings into high yield investments.

Although, the process of investing in Mutual Funds may seem straightforward, it is riddled with roadblocks (e.g., lack of financial know-how), some of which can easily (and rapidly) be countered with the help of chatbots. An effective chatbot can resolve certain customer queries within seconds, and if executed accurately, can put the customer at ease, thereby increasing his/her propensity to move ahead with that particular product or service.

On the banking side of things, large financial institutions such as Citi, Bank of America and Capital One have implemented their versions of chatbots, which customers can access through the respective mobile apps, Facebook Messenger, Twitter or regular text messages (SMS). At Citi and Capital One for example, customers can check their account balances, recent transactions, payment history, credit card bill summary, and avail many other non-financial services. Answering FAQs is one of the other key service areas where banks have excelled. All of these services collectively provide the user with real-time, easily accessible customer information. As a natural move forward, albeit on the slower side, banks are now implementing chatbots that allow customers to carry out financial transactions on their platforms; something that seemed generations away, doesn’t seem that far-fetched after all.

The need of the hour is communication, with its delivery through messaging applications dominating the social media & messaging landscape. These applications have far surpassed social media in terms of total users as well as total time spent. There are over 300 million people across India alone that have access to the Internet on their smartphones today, and India is embracing the Internet in a way we could not have imagined before. Keeping this development in mind, imagine a world where we use automated chatbots to not only breakdown financial concepts for seasoned smartphone users, but also help new internet users navigate through a plethora of financial information. The idea is to spread financial literacy, and create a more meaningful customer journey, from curiosity to execution. And chatbots make this accessible, by reaching customers via apps they already use – WhatsApp, Facebook Messenger, and Twitter – rather than making clients download additional apps.

The advent of chatbots (messengers, as well as voice recognition applications) has allowed companies to penetrate, through smartphones, the potential user base like never before. The primary use case for chatbots, in this day and age, is non-financial in nature. Most financial institutions allow customers to access only basic product information, and information regarding certain processes on their chatbots. However, with regulatory authorities taking a closer look at integrating such technologies into financial transactions, it won’t be too long until we can safely say “Alexa, please transfer $500 to Patrick this Thursday”, and rest easy.

By Abhijit Aroskar, Consultant, Cedar Management Consulting.

Data volumes are not just growing, they are exploding. Now measured in zettabytes – which could become yottabytes in the not too distant future – it’s not surprising they are causing more than a headache for today’s organisations. These vast pools of data are also putting traditional database architecture to the test.

Nowhere is this problem felt more acutely than in the banking industry, where the situation is exacerbated by a complex raft of issues. For example, many banks have had the same legacy systems in place for decades.

Often these are not fully-integrated with others in the organisation and, consequently, many applications still run in a siloed environment. In a recent study by analyst firm Enterprise Strategy Group (ESG), commissioned by InterSystems, 38% those polled reported that they had between 25 and 100 unique database instances, while another 20% had over 100. Although this was a general survey, not confined to the banking industry, it does give some idea of the scale of the problem.

So although many banks own these vast amounts of data, many of them are unable to do anything with it, especially analyse it in real-time. Which means that often they just don’t have the capability to provide the open banking demanded by new regulations such as PSD2.

Banks have been addressing new regulations in a piecemeal fashion for too long and this approach is now catching up with them. With each new ruling they have put a new siloed application in place to meet its specific needs and no more – but there’s a limit to how long this can continue. Today’s regulations are demanding an end to data siloes with integration enterprise-wide and the ability to analyse data in real-time.

These are broad-brush requirements. At a more granular level, banks must think through the step-by-step processes needed to meet compliance. Typically, they will need to bring information in from multiple applications, run reporting on this data on a real-time basis and generate that in a format that meets the regulator’s precise requirements.

As a result, banks must seek out a data platform that can ingest data from real-time activity, transactional activity and from document databases. From here, the platform needs to take on data of different types, from different environments and of different ages to normalise it and make sense of it. The platform they select must be about to reach out to disparate databases and silos, bring the information back and then make sense of it in real-time.

This platform must also have the agility to separate out the data they need from the data they don’t need to access. It is also the case that, as businesses migrate systems and applications to the cloud, they are beginning to use software to ‘containerise’ their applications and modules. Once these containers have been set up in the cloud, they are then reusable by other applications.

It is crucial that a data platform enables data to be interrogated even if it is in large data sets and stored in different silos. This capability is important to enable the bank to comply with regulatory requirements such as answering unplanned, ad hoc questions from the industry regulators, for example.

The advantage of working this way is that it can take the bank far beyond compliance. It will now have a secure, panoramic view of disparate data which can be used for distributed big data processing, predictive and real-time analytics and machine learning. Real-time and batch data can be analysed simultaneously at scale allowing developers to embed analytic processing into business processes and transactional applications, enabling programmatic decisions based on real-time analysis.

So although many banks and other financial services organisations may feel they are being swallowed up by data, the need for compliance will ensure this doesn’t happen. The more they are storing on legacy systems, the more they are going to need an updated data platform. If they think carefully about selecting the right one, the move could result in improvements across data management, interoperability, transaction processing and analytics, as well as the means to address today’s and tomorrow’s regulatory demands.

By Jeff Fried, Director, Product Management – Data Platforms, InterSystems

Karen Wheeler, Vice President and Country Manager, Affinion

It would come as no surprise if internet retailer Amazon announced it was taking over the world tomorrow. There seems to be very little that it can’t offer customers, whether it’s conquering Christmas lists, watching boxsets through Prime or managing life admin through the intelligent personal assistant Alexa, almost everyone uses one or more Amazon service on a regular basis.

One common denominator that defines Amazon’s success across all of its platforms is customer experience – providing simple, convenient and engaging solutions that go that extra mile to ‘wow’ customers and retain their loyalty.

Banks, however traditional or modern, can take a leaf out of Amazon’s book when it comes to engaging with customers and harnessing innovation to continuously improve their offering.

Here are five important lessons banks can learn from Amazon.

The customer always comes first

Listening to what the customer wants has been the driving force behind many of Amazon’s products and developments. McKinsey’s CEO guide to customer experience advises that the strategy “begins with considering the customer – not the organisation – at the centre of the exercise”.

This can often be quite a challenging ethos for the banking sector to buy into, particularly for the more traditional bricks-and-mortar companies where the focus is often on the results of a new initiative, rather than the journey the company must take its customers on to get there.

It’s a case of convincing senior management that the initiative is a risk worth taking and just requires some patience. Amazon originally launched Prime as an experiment to gauge customers’ reactions of ‘Super Saver Shipping’ and it was predicted to flop. Nowadays it’s one of the world’s most popular membership programmes, generating $3.2bn (£2.3bn) in revenue in 2017, up 47 per cent from 2016.

Create trends rather than follow them

To stay ahead of the curve amidst the flurry of digital fintech start-ups, banks need to come up with their own innovative customer experience solutions, rather than allow newcomers to do so first and then follow suit.

From the customer’s perspective, a proactive approach will always go down better than a reactive one. Amazon CEO Jeff Bezos has previously spoken about tech companies obsessing over their competitors and waiting for them launch something new so that they can ‘one-up’ it. He once wrote: “Many companies describe themselves as customer-focused, but few walk the walk. Most big technology companies are competitor focused. They see what others are doing, and then work to fast follow.”

What sets Amazon apart is listening to what the customer wants and prioritising them over competitors.

A great example in the banking sector is mobile-only bank Starling, which recently announced partnerships with several financial service providers that customers can quickly access via its in-app ‘Marketplace’. The first to become available is PensionBee, a digital pension provider that aims to consolidate pension pots into one. Others, including a digital mortgage broker and a digital wealth management service, are soon to follow.

Ultimately, Starling listened to and understood its digitally-minded customer base who, like most people, see shopping around for financial providers complicated and admin-heavy. One central app where you can seamlessly select a trusted digital partner would no doubt go down as good customer experience.

Use customer data to form any new idea

It’s no secret that Amazon is one of the leaders that has paved the way for analytics. It’s through the company recognising the need for them which has led to customers becoming accustomed to personalisation and expecting it as soon as they have had their first interaction with a business.

Banks are no exception to this and, while it may seem like a scary commitment to more traditional firms, it doesn’t have to be complicated. A classic, simple example is Amazon storing customers’ shopping habits and sending them prompts for new products similar or related to those they have purchased in the past.

In the financial world, digital bank Monzo is leading the charge by monitoring customers’ spending habits to offer them financial advice to help them save money and budget responsibly. For example, its data once showed that 30,000 of its customers were using their debit cards to pay for transport in London – so Monzo can advise them they could save money if they invested in a year-long travel card, for instance.

There are endless things banks can do using customer data to provide the customer with an experience unique to them, rather than continuing to make them feel like just another cog in the wheel. At Affinion we believe in ‘hyper-personalisation’, in that these days it’s no longer good enough to just know a customer’s history of transactions with a company and when their birthday is.

Customers are getting more tech-savvy by the day and are expecting real-time responses with a deep insight into their interactional behaviour – they won’t remain engaged if follow up contact is irrelevant and untargeted. Customer engagement has moved on from companies communicating to the masses, it’s about creating tailored, intuitive relationships with them on an individual basis.

Widen the offering beyond traditional banking

The way we live as a society is forever changing and, as we get busier and busier, any small gesture to make life that little bit easier goes a long way. The consolidation of services such as banking, insurance, mobile phone networks, utilities and shopping is a great way to ensure customers remain loyal to a brand as it will – if done right – add value and reduce hassle to their lives.

As an expert at disrupting industries, Amazon has taken note of this growing need for convenience over the years and has expanded its offering for customers, allowing them to carry out multiple day-to-day tasks with one account. In the last few months alone, Amazon has hinted that it may acquire a bank to break into the financial industry and potentially start its own healthcare company.

Regardless of size, banks should always be looking for new areas they could tap into to broaden their offering and show customers that their needs are at front of mind.

Engage with customers through goodwill

A rising factor in the way that customers align themselves to a brand is its stance on ethical issues and its contributions back into society. It’s a shift that seems to be most prominent with Generation Y, as the Chartered Institute of Marketing found that 81 per cent of millennials expect companies to make a public commitment to good corporate citizenship and nine in 10 would switch brands to one associated with a good cause.

Amazon has gone that one step further, with its AmazonSmile initiative that allows the customer to choose a charitable organisation that it will donate 0.5 per cent of eligible purchases to. Not only does this show Amazon’s commitment to charitable causes, it gives the customer control of where their money ends up.

This is an easy win for the banking sector, given that one of its sole purposes is to look after money and move it around. For firms that target younger generations in particular, looking at ways to involve customers in charitable donations in a fun, transparent and seamless way is a no-brainer for increasing loyalty and advocacy.

It’s time banks took customer engagement even more seriously

For many people, personal finance is perceived as a chore and often quite complicated. Improving the customer experience and building in programmes to engage them can help greatly with this and banks need to adopt the ‘customer first’ ethos that Amazon showcases so effortlessly. With new fintech disruptors creeping into view, keeping customers loyal and engaged has never been so important.

By Karen Wheeler, Vice President and Country Manager UK, Affinion

During the height of the crypto boom, everybody from Paris Hilton to the Venezuelan government seemed to be either setting up or promoting ICOs as token values skyrocketed. Even ICOs that were blatant jokes like the Useless Ethereum Token reportedly raised $200,000. Those days are over.

During the height of the crypto boom, everybody from Paris Hilton to the Venezuelan government seemed to be either setting up or promoting ICOs as token values skyrocketed. Even ICOs that were blatant jokes like the Useless Ethereum Token reportedly raised $200,000. Those days are over.