Before Covid-19 emerged, the way employees viewed work was limited. With defined working hours and fixed office space, it was hard to imagine the drastic change that was coming. Today, more workplaces have adopted both hybrid and remote working, as employers learnt just how much could be done from home, or at least outside of an office.

This has resulted in a decrease in full-time workers, with employees taking on more freelance and flexible roles. Beyond remote working, the way the workplace may evolve and change are hard to predict, but what we do know is that it will impact the payments industry.

The changing workforce

Remote working existed prior to the pandemic but was not adopted as widely as it is now. Employers are currently offering remote and flexible working to stay competitive in the market, with studies showing that 70% of the workforce will be working remotely at least five days a month by 2025 – but this is not the only change.

From Bark and Toptal to Upwork and Fiverr, freelance marketplaces play a key role in connecting freelancers with businesses looking to hire. With more organisations based around the world employing freelancers, cross-border payments will be required at a much higher rate. Cross-border payment services will be needed more than ever to collect money from international clients and pay overseas freelancers.

The financial payments space must set itself up for the growing globalisation of the workforce, and as the world embraces flexible working and freelancing, this creates greater opportunities for platforms in the cross-border space to provide their services. This is especially important given the forecasted rise in the value of cross-border payments over the next six years – with research from the BCG predicting that the value of cross-border payments will increase from almost $150 trillion (2017) to over $250 trillion by 2027.

With the reach of freelance marketplaces growing, they must ensure the best processes are in place in order for funds to be transferred successfully – this is where cross-border payments services come in. Freelancing platforms must work with multinational payment service providers to help advise on overseas regulations and also provide fast payment speeds, payment tracking, strong security and transparent pricing. This will ensure the platforms pay and get paid efficiently.

What caused the workforce revolution?

These changes are important to note, but the catalyst of these must be understood too. A key cause of the change in the approach to working is technology. Digital communications platforms such as Zoom and WebEx have meant that staff are able to work collaboratively without being in the same room. Of course, many of these apps existed before, but with the emergence of Covid-19, the public put them to the test and became reliant on keeping in contact with colleagues. This created a “new normal”.

While major events such as a pandemic cannot be predicted, the payments space can now prepare for changes to the workforce. The increase of both remote and freelance work is likely to stay, and businesses should do what they can to prepare themselves for the modern and future ways of working.

The Covid-19 pandemic triggered an unprecedented macroeconomic shock that impacted the global financial system. The resulting market turmoil, together with significant spikes in volatility and trading activity, presented particular challenges to the design and the resilience of risk management in Financial Market Infrastructures (FMIs).

by Adrien Vanderlinden, Executive Director, Systemic Risk Office, DTCC

With the benefit of hindsight, FMIs around the world have successfully navigated this real-life test. That said, these events have also highlighted 5 focus areas for FMIs and their participants to proactively manage risk in a post-pandemic environment.

First, it should be recognised that the market stress that emerged as the pandemic started to spread strained the ability of certain risk models that are based on historical data to produce reliable output. That said, models designed to function in ‘normal’ markets should not be discarded simply because they have limitations in extreme market circumstances. Instead, what this episode illustrates is a well-known fact that is not new by any standard: FMIs should have the requisite model performance monitoring, strategies, and governance in place to identify and address emerging model risk issues on an ongoing basis.

Margin procyclicality

Second, while margin procyclicality was already a topic of debate prior to the pandemic, the extreme market volatility we saw in March and April 2020 will likely make the issue much more prominent going forward. The most important goal for CCPs (central clearing counterparties) is to make sure that they collect enough margin to protect their members, underlying investors, and themselves in times of stress. It is also important to note that risk-based margining methodologies are naturally procyclical, as they tend to generate increased margin requirements during times of market volatility, which in itself is not inherently problematic. A potential mitigant is education so that FMI members are sufficiently prepared to anticipate the impact of volatility spikes and clearing activity changes on their margin requirements. As such, FMIs must further promote margin transparency through the continued availability of tools that allow their members to understand risk models and estimate margin requirements under a wide range of circumstances.

Sector-specific approach to managing credit risk

Third, FMIs need to take a more sector-specific approach to managing credit risk due to the significant divergence of pandemic recovery prospects across corporate sectors, geographies, and other variables. A key consideration is the extent to which banks and other financial institutions are exposed to sectors that have been particularly adversely impacted by the pandemic, such as travel and leisure. As a result, credit risk assessments need to include a sector-specific review, with a focus on firms with the greatest concentration of risk. In the banking sector, additional indicators of risk can be found by analysing stress test results, as well as reviewing macroeconomic and loan delinquency data released by various sources, such as the Federal Reserve and credit reporting agencies.

Continuous assessment of FMI members’ available liquidity

Fourth, given the spikes in volatility, trading volumes and margin calls, FMIs should continue to closely monitor clearing members’ financial resources, in particular available liquidity, on an ongoing basis, as this can change quickly in a crisis. Financial firms face trade-offs between maximizing profitability and ensuring they have access to sufficient financial resources in a crisis. While retaining surplus capital or maintaining sources of liquidity may appear suboptimal from a capital usage and profitability perspective, it can be crucial to surviving a crisis. FMIs must assess how their members balance these trade-offs and whether they have allocated sufficient resources for normal times, mildly stressful circumstances, and extreme events, such as the Covid-19 pandemic.

Impact of remote working on operational risk

Finally, FMIs must consider that remote work can create new operational risks that need to be managed on an ongoing basis. FMIs successfully transitioned their workforces during the early stages of the pandemic without material impact to services thanks to well-planned risk management strategies, as well as significant pre-pandemic investments in business continuity planning and supporting technological capabilities. An extended remote work environment and the development of return-to-office plans that may involve a change in staffing models will require developing and implementing new capabilities that support the identification, monitoring and managing of associated risks. Further, the growth of remote work in the future may create additional cyber security vulnerabilities that must be monitored and integrated into existing cyber risk management frameworks. FMIs will also need to evaluate strategies and controls to mitigate the operational risks created by a potential outage related to a critical third party.

The impact of the pandemic on financial markets created a real-life stress test for risk models as margins surged amid spikes in volatility. FMIs around the world clearly met this challenge, helping to safeguard global financial stability. While their robust financial risk management frameworks and BCP strategies proved effective, FMIs will need to continue to bolster efforts in these five areas to be prepared for the next market disruption or crisis.

Legacy systems can become a major barrier to progress. By maintaining outdated legacy systems, the UK government risks wasting between £13-£22 billion over the next five years. The figures come from an independent investigation into the government’s Digital, Data and Technology function published by the UK Cabinet Office.

by Andrew Barnett, Global Head of Product Strategy, RIMES

It’s a lesson that investment managers know all too well. Currently, in many legacy systems data is centralised within firms and constrained by costly technology, such as Enterprise Data Management (EDM) platforms, Extract Transform and Load (ETL) tools and data warehouses.

As data volumes explode, firms are finding it more and more difficult to govern, quality assure and distribute data across the organisation with legacy systems. It’s little surprise, therefore, that only 4% of investment managers are happy with their data management systems.

The solution seems clear: make a clean break from the legacy systems of the past and invest in agile and scalable alternatives. However, for many firms this is a case of ‘easier said than done’. Often, asset managers simply lack the people or budget required to overhaul legacy technology and the valuable data trapped inside it. In other cases, firms are wary of potential hidden costs associated with decommissioning legacy systems, or the risk of disruption to business-as-usual, which they worry will negatively affect client service.

Andrew Barnett, Global Head of Product Strategy, RIMES

The cloud offers an alternative. In addition to cost-savings and the appeal of consumption-based pricing, the cloud provides a range of benefits for firms that makes data management transformation a realistic prospect for all asset managers regardless of their size, existing investments or budget/resource limitations. These benefits include:

Ease of install. With a cloud-based delivery model, firms can avoid potentially disruptive upgrades of internal systems or being out of compliance with dated versions. Additionally, firms can migrate to the cloud one application or data set at a time due to the cost model and ability to operate over private and public clouds. As a result, they reduce risk by running legacy systems in tandem as they move to the cloud at a pace that suits them best without duplicating costs.

Access to expertise. With the cloud firms not only access infrastructure and services, in many cases they can also draw on the expertise of a cloud-based partner. At a time when data skills are scarce this is a significant value add, as it allows firms to focus their internal data resources on value-generating data analysis tasks rather than low-value data management.

Improved lineage and governance. Ensuring data governance, lineage and oversight is critical to compliance and staying in the terms of a licence, but it is often the area that firms struggle with most as legacy systems may not have the quality and governance needed in the modern highly regulated landscape. Cloud-based service providers can accelerate this process through automated services, delivering governed, high-quality data in a system-ready format.

Adaptability. As operational data management issues arise, such as the need to adapt to emerging data demands, such as ESG, or manage intense market volatility, firms invest in people and technology to find solutions – some of which do not work. Cloud-based models avoid this waste. Relying on their service provider, firms can lean on proven service models, data expertise and scale to solve problems quickly and efficiently.

Scale. A key reason these technologies have been allocated to the ‘sunsetting’ classification is that they do not have the cost-effective scale or flexibility that the cloud provides. We can’t predict the future but if we have a cloud-based cost model aligned with your revenue growth then we remove an important constraint.

It’s widely acknowledged that data insights will be essential to success in the investment management industry of tomorrow. Firms taking a legacy approach to data management will be at a disadvantage, hampered by uncontrollable cost increases and a dearth of talent needed to process data to then turn it into actionable intelligence. Coupled with the downward pressure on fees that continues to blight the industry, this approach is simply not sustainable.

Cloud-based managed data services offer an alternative by driving quality, efficiency, scale and adaptability across your data landscape, reducing waste and keeping a lid on costs. Make no mistake, firms need to oversee large scale changes to their data management systems. Fortunately, cloud-based managed data services make the case for this change stack up. More than that, they make it imperative.

Banks and financial institutions have been hesitant to adopt public cloud technology due to a fear of losing control. What are the psychological barriers facing financial services executives and how may they be overcome?

Accelerated by the global pandemic, the financial services industry is undergoing a period of intense technological transformation. The impact of Covid-19 is putting incumbent banks and financial institutions under cost, profitability, and operational stresses; regulatory requirements are growing in volume and complexity; and legacy systems are increasingly putting businesses at risk of service failure, loss events, and reputational damage.

In this environment, there’s no doubt that the future of financial services is in the cloud.

Its potential to deliver greater agility, cost effectiveness, efficiency, scalability, and speed to market provides new opportunities for growth and innovation. What’s more, a cloud-first approach offers firms the ability to better control their data and remain connected, freeing up highly stretched resources to focus on other business objectives. Migrating to the public cloud can play a critical role in strengthening operational resilience, too. In the face of increasingly high customer standards and, in the UK, new rules from the FCA coming into effect from March 2022, IT and system failures will simply not be tolerated in future.

So why are we still seeing a hesitancy towards cloud adoption among senior financial services executives?

Outsourcing functionality, not control

Neil Vernon, CTO, Gresham Technologies

For the most part, it is the fear of losing control. Regulatory changes are increasing the pressure to meet a greater number of more complex requirements. In line with that, the risk of more severe non-compliance and the consequences that follow are also increasing. Exacerbating this problem is a pandemic-induced move towards working-from-home or hybrid environments, leaving outdated legacy systems unable to cope with the agility this demands.

Ultimately, the data that banks and financial services firms handle is very sensitive, either regarding customers’ financial information or traders’ operations. If compromised, this could present significant financial and reputational risk. Capital One Bank’s 2019 data breach, for example, which affected 106 million people across the U.S. and Canada, resulted in an $80 million fine. And the reputational consequences were tangible: in the days following the breach, Capital One’s stock plummeted from over $100 to $85 – both a consequence and catalyst of the reputational damage that the bank suffered.

All of this means that data control is more important than ever. But the truth is that moving to the cloud does not mean sacrificing control.

It is critical for business leaders to understand that leaving processes on legacy systems increasingly exposes you to loss and failure events, and that outsourcing your data and processes to third-party cloud providers is actually a more secure alternative. It can significantly increase efficiency and reduce costs by simplifying processes, as well as reducing the risk of non-compliance while simultaneously avoiding expensive in-house IT projects, both in terms of time and money.

Gaining insight through connectivity

In fact, moving to the cloud can put you in more control by facilitating a holistic view of your relationships as your business grows.

Connecting to an ever-changing array of trading partners, venues, clients, and regulators – and ensuring these connections remain valid – is a dynamic process. What’s more, firms must manage, map, and maintain the widely diverse and constantly changing data formats that flow between these parties.

Navigating this complex data landscape can cost millions every year in internal resources or point solutions that become stale. Moving this process to the cloud can give you the scalability your business needs to grow its network with speed and ease.

Work with the cloud, not against it

Despite a reluctance to overhaul existing processes and the temptation to bend cloud software to fit your own objectives, executives must understand that, in order to harness the power of the cloud, you must work with it – not against it.

A flexible approach, whereby firms understand that successful cloud migration might require some upfront work, is key. Integrating cloud with non-cloud, or different cloud services with each other, is often complex. A rigid attitude will likely result in disappointing results and data migration complexities, costing time and money better spent servicing clients.

Part of this flexibility is understanding best practice around how to use the cloud. The Bank of England (BofE) has warned that additional policy measures may be required to mitigate financial stability risks from the growing concentration of power in the hands of global cloud providers, such as Amazon, Google, and Microsoft. In response, firms should be looking at the ways in which cloud service providers are different and playing to those strengths to diversify their cloud portfolio.

It’s vital that firms have the right partner to help them navigate the application of their cloud technology across the major providers with relative ease, flexibility, and portability. What’s more, in addition to new BofE policy, big providers could be dictating cloud terms and conditions to major financial firms in future. Understanding and reporting on these requirements will cost valuable time, money, and resources that are much better outsourced to cloud-native technology experts.

Ultimately, a fear of losing control shouldn’t act as a barrier for cloud adoption. Once properly understood, the power of the cloud and its potential impact on business performance cannot be overstated, offering unparalleled benefits that, in an era where data control, integrity, and connectivity rule, could make or break financial institutions across the globe.

Customer-centricity and financial inclusion remain a challenge for the financial services sector. With banking products offered to customers becoming increasingly commoditized, AI-powered analytics can help banks differentiate themselves, provide competitive edge and enable personalised customer experience. The coming of age of such technologies allows banks to develop a strategic and organizational focus in analytics and adopt it as a true business discipline.

by Krish Narayanaswami, President & Global Head – Banking at Azentio Software

The analytics and business intelligence (BI) software market grew by 10.4% to $24.8bn in 2019. The world of banking has encountered unprecedented change over the past few years, and trends show that this will be the norm for a while longer. Modern BI platforms continue to be the fastest-growing segment at 17.9%, followed by data science platforms with a 17.5% growth (Source: Gartner).

Krish Narayanaswami, President & Global Head – Banking at Azentio Software

Banks have been an early adopter of BI and analytics to drive business growth, reduce risk and optimise cost. With the rapid growth in digital banking, the velocity of transaction data has increased multifold. This data has now unlocked tremendous opportunities for banks in understanding consumer behaviour and tailor make specialised offerings by leveraging analytics as Decision as a Service

How will changes in banking laws and regulations affect profitability? Which stress scenarios should be considered? Who are the current ‘high-value’ customers? Which customers have the highest potential to ensure revenue growth? Can the bank create an early warning system to prevent fraud by identifying patterns? Increasingly, data analytics is seen as the answer that banking leaders are looking to, to successfully navigate this volatile environment.

Present Day Strategy and Key Drivers

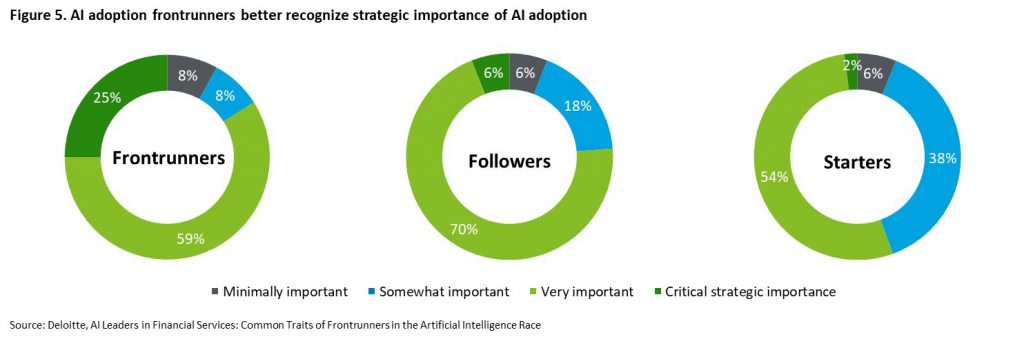

According to a recent Deloitte survey, frontrunners benefited from early recognition of the importance of analytics to the overall business success. This recognition has helped them shape a specific analytics implementation plan that considers holistic AI adoption across the enterprise. The survey indicates that many frontrunners launched analytics centres of excellence and established comprehensive, companywide strategies for AI adoption for their internal departments, recognizing the strategic importance of AI.

The following strategies should be taken into consideration while adopting an analytics framework across the organization.

Prioritize the focus areas

Identify key areas where data and analytics can have the greatest impact and obtain leadership engagement from the start (for example, customer, risk, finance). This must reflect in the immediate goals and vision of financial institutions.

Streamline your data

Provide an integrated view of high-quality data vs. siloed pockets across product and business lines (for example, single view of the customer, aggregated risk exposure by product). Setting up a data warehouse/data lake and further creating specialized data marts to make the data more structured and easily accessible to the respective stakeholders.

Integrate with decision management systems

The key is to develop data-driven strategies at every step to arrive at smart decisions. Analytical insights can be plugged directly into decision management systems to arrive at the next best action.

Onboarding the right skillsets

Finding the right talent for statistical modelling little data and big data is one of the biggest challenges. Develop a talent plan that builds on both existing internal talent and external sources.

Leverage the power of cloud

Leading cloud providers like AWS, Azure, OCI and GCP are providing powerful analytical offerings as services and have the power to run heavy compute. The ability to scale up infrastructure to run high loads and to bring it down when not required helps in optimising costs.

What is the way forward?

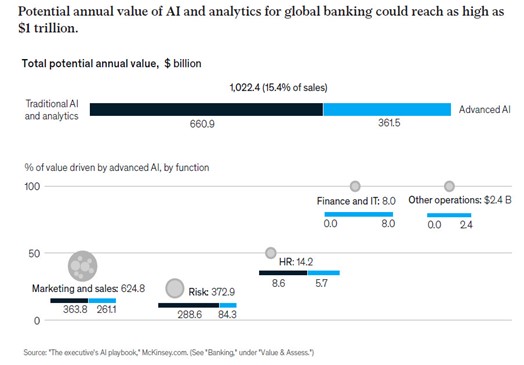

According to a 2020 McKinsey study involving over 25 use cases, AI technologies can help boost revenues through increased personalization of services to customers (and employees); lower costs through efficiencies generated by higher automation, reduce errors rates and improve resource utilization. It can uncover new and previously unrealized opportunities based on an improved ability to process and generate insights from vast troves of data.

The potential value creation for banks is one of the largest across industries, as AI can potentially unlock approximately $1 trillion of incremental value for them annually.

Realising the need for going mainstream with AI, banks internationally have already started harnessing the power of data to derive utility across various spheres of their functioning, including sentiment analysis, product cross-selling, regulatory compliances management, reputational risk management, and financial crime management.

AI and analytics will eventually become a part of every major initiative, in areas ranging from customers and risk, to finance, workforce, and supply chain.

Personalised experiences and products powered by advanced analytics and machine learning will be key to wooing customers in this era of intense competition. Banks have a chance to overcome the hurdles and join the analytics arms race before the frontrunners extend the gap that would be too far to bridge.

For a start, companies have moved from being hands-off to hands-on in managing their forecasts and FX hedging. It is seen as a concern across the business, impacting sales, procurement, and the supply chain. While the C-Suite are aware of the impact, it is often the board that is driving change in wanting to see a far more proactive approach in managing these risks.

The increased volatility in financial markets, is matched by increased uncertainty in business. Once stable supply chains now operate on much shakier terms if they haven’t disappeared altogether. It means there is no longer certainty around when you will be making a payment or how long you will need to hedge.

Richard Eaddy, CEO, Hedgebook

Businesses working on low margins can be significantly impacted. A cancelled order or significant swing in foreign exchange that has not been hedged, leaves the business dangerously exposed. All of this has meant UK companies are looking more regularly at their hedging positions and reviewing the risk.

Many businesses are acting responsibly and adding FX Management to their library of risk management policies. This gives the treasury team some real guidance as to the risk tolerance the business is prepared to work within. The ability to model FX hedging options against this policy enables faster and better decisions to be made – with minimised risk.

Remote working also removed the expectation of a monthly or quarterly meeting where such matters were generally discussed. The traditional round-the-table closed door reviews essentially disappeared during lockdown.

Very quickly, companies realised the need to proactively review their FX hedging positions and that players across the company needed to part of that. Over 80% of surveyed customers using our FX tools now engage with them at least once a month, with 10% checking in on a daily basis.

Working remotely has also seen companies move away from spreadsheets being the default tool for managing FX hedging. This is largely due to the increased risk around version control and data security when shared across multiple screens and locations.

But it also highlighted the spreadsheet owner as a potential single point of failure in the organisation. In many cases they were the only ones who could successfully run the formulas and manage the complex hedging situations the business was facing. As a result, companies have proactively started looking for online tools capable of managing this for them.

They want to view data in real time, have secure access to their hedging positions and for everyone involved to be working off a single version of the truth. Companies now say using online FX hedging reports and modelling saves them half to a full day per month – but the exponential value is in greater accuracy and faster, better decisions.

It is these companies that are driving change. They expect their banker to be able be onboard with managing foreign exchange hedging online. They want their broker to see the same information they are and be able to guide them through the options – modelling the different rates and hedging percentages as they go.

Even though cloud technology has driven the access cost right down, online treasury management is new technology for banks to become familiar with. Perennial slow adopters, banks are now realising they need to get onboard fast, or their customers will leave them behind – quite literally.

It really should be a win-win for everyone. Customers limit their FX risk and banks become even more valuable and responsive to their customers. It enables much better FX hedging decisions to be made faster and strengthens the bank’s relationship with its customers. A definite change for the better.

IBS Intelligence is partnering with Sopra Banking Software to promote the Sopra Banking Summit, which takes place 18-22 October 2021. The summit is tackling the biggest issues in the financial sector. This weeklong festival of FinTech will touch on the hottest topics in financial services and highlight the new paths industry leaders are taking.

Financial inclusion – its efficacy, implication and urgency – is becoming one of our industry’s biggest talking points. And this is a good thing. The more light that’s shed on the issue, the more likely we are as a collective to push its agenda.

by Nelly Kambiwa, Financial Inclusion Director MEA, Sopra Banking Software

However, there are still question marks over what exactly financial inclusion means. For some, it’s tied intrinsically to demographics; for others, it’s about politics. Most interpretations are not wrong, and almost all are well meaning, but perhaps the clearest and most succinct definition comes from the World Bank:

“Financial inclusion means that individuals and businesses have access to useful and affordable financial products and services that meet their needs – transactions, payments, savings, credit and insurance – delivered in a responsible and sustainable way.”

Nelly Kambiwa, Financial Inclusion Director MEA, Sopra Banking Software

Without this ‘access to useful and affordable financial products and services,’ people may not have a secure place to store money, no effective and free means of receiving payment, and no safe, reliable way to make payments.

And while great strides have been made around financial inclusion, there’s still a long way to go. According to the most recent Findex data, there are still close to 1.7 billion adults in the world without access to basic financial services

Financial inclusion in Africa

Of course, financial inclusion is not a challenge limited to a particular country, region or continent; rather, it affects areas all over the world. However, for the purposes of this article, we’re going to look at financial inclusion in Africa, and how digital lending can help to improve the financial lives of millions of Africans.

According to Global Finance, 50% of the African population is unbanked, equating to 350 million people. This is already a problem that needs addressing, but with the African population rising quickly – it’s set to double over the next 30 years, adding an additional 1 billion people – it could quickly go from bad to worse.

The role of digital in expanding access

Extending access to borrowers who are otherwise unlikely to receive it is key to improving the health of a society. Among all financial services, access to credit is perhaps the most important as it’s a force multiplier. To this end, innovative digital strategies and new technologies are enabling lenders to reach traditionally underserved people while securing their own interests.

Indeed, the use of big data, artificial intelligence, machine learning and open banking-enabled solutions is expanding the scope of what’s possible. Thanks to new products and soaring internet penetration rates, geographical limitations are being overcome. More sophisticated data analysis tools have come online and are enabling easier credit decisions in lieu of traditional credit scores.

This is particularly relevant to lending in Africa, where access to physical branches is an issue for many people. A recent white paper published by Sopra Banking explained how the rise in mobile money users in Africa is an opportunity and challenge that many incumbent financial institutions have yet to rise to.

Thankfully, that is changing, and many lenders are coming up with solutions that will allow them to provide digital loans to their customers in a safe and effective way for all parties. With the introduction of video KYC and account aggregators, lenders can easily access permissioned customer data and conduct better due diligence. And the digitization of the entire loan application lifecycle means that borrowers can apply for loans remotely—a benefit both in terms of reducing friction and expanding reach.

New-to-credit (NTC) customers

Historically, credit institutions have been cautious with NTC consumers, due to the lack of credit history to assess their probability of default. However, given technological advances, lenders can now more confidently lend to NTC borrowers. They can do this by leveraging some of the solutions mentioned above, solutions that afford new ways of analysing data, predicting a customer’s creditworthiness and gauging the risk involved in lending.

Analysing mobile and web data makes it possible to offer credit to individuals and SMEs without financial footprints. Over the past decade, this practice has emerged and really caught on in Africa, where FinTechs, microfinance institutions and traditional financial institutions like NCBA Group, Equity Bank and Orange Bank use SMS data to inform credit decisions.

While alternative credit scoring systems show great promise, they also bring up privacy and data reliability concerns. And in at least one case, have led to a large group of digital borrowers taking on unsustainable levels of debt.

Open banking as a catalyst

On the regulatory side, open banking is also driving improvement in lending processes. With access to more data (including non-financial data), lenders can do enhanced credit scoring and risk assessment. This provides additional insight, allowing lenders to assess a borrower’s eligibility more accurately. This not only drives down costs for the lender, but it improves the customer experience and, because it’s digital, it works in places without existing infrastructure.

For those most likely to be denied credit, the sub-prime loan application process can still be paper-heavy, involving the manual submission of payslips or statements. Furthermore, Covid-19 has underscored just how inefficient traditional loan processes are.

As an antidote, open banking is pushing financial inclusion solutions that make it easier to verify customer details in real-time—in some cases, going as far as automating the entire interaction. This makes the process easier for the user and significantly increases the chances of applications being accepted.

The good news is that African banks are taking notice of open banking and starting to take huge strides in furthering its implementation. For instance, in 2020, the Central Bank of Kenya – a country where 44% of the population is unbanked – included open banking as one of its main strategic objectives; and last year at the height of the pandemic, Nigerian startup Okra announced that it had received significant funding to develop an open banking infrastructure.

Such developments are becoming increasingly common throughout Africa and bode well for the future of financial inclusion across the continent.

Looking ahead

Digital lending is redefining the dynamics of the credit market in Africa. With a lower cost base and improved reach, financial institutions – including banks, MFIs, neobanks and Telcos – can simply do more with less. Digital lending cuts the cost of offering services and streamlines onboarding. It also enables instantaneous and remote approval and supports data-driven mechanisms to initiate repayment. At the same time, open banking facilitates greater access to data than ever before and unlocks new use cases.

Ultimately, expanding access to credit requires careful planning and is more of a journey than a destination. The use of alternative credit scoring is still in its infancy, and open banking is only a few years old. At its best, digital credit can be responsible, inclusive and affordable. And it’s something every financial institution should strive for, as it not only helps individuals and communities, but it drives economic growth, too.

For a start, companies have moved from being hands-off to hands-on in managing their forecasts and FX hedging. It is seen as a concern across the business, impacting sales, procurement, and the supply chain. While the C-Suite are aware of the impact, it is often the board that is driving change in wanting to see a far more proactive approach in managing these risks.

Richard Eaddy, CEO, Hedgebook

The increased volatility in financial markets, is matched by increased uncertainty in business. Once stable supply chains now operate on much shakier terms if they haven’t disappeared altogether. It means there is no longer certainty around when you will be making a payment or how long you will need to hedge.

Businesses working on low margins can be significantly impacted. A cancelled order or significant swing in foreign exchange that has not been hedged, leaves the business dangerously exposed. All of this has meant UK companies are looking more regularly at their hedging positions and reviewing the risk.

Many businesses are acting responsibly and adding FX Management to their library of risk management policies. This gives the treasury team some real guidance as to the risk tolerance the business is prepared to work within. The ability to model FX hedging options against this policy enables faster and better decisions to be made – with minimised risk.

Remote working also removed the expectation of a monthly or quarterly meeting where such matters were generally discussed. The traditional round-the-table closed door reviews essentially disappeared during lockdown.

Very quickly, companies realised the need to proactively review their FX hedging positions and that players across the company needed to part of that. Over 80% of surveyed customers using our FX tools now engage with them at least once a month, with 10% checking in on a daily basis.

Working remotely has also seen companies move away from spreadsheets being the default tool for managing FX hedging. This is largely due to the increased risk around version control and data security when shared across multiple screens and locations.

But it also highlighted the spreadsheet owner as a potential single point of failure in the organisation. In many cases they were the only ones who could successfully run the formulas and manage the complex hedging situations the business was facing. As a result, companies have proactively started looking for online tools capable of managing this for them.

They want to view data in real time, have secure access to their hedging positions and for everyone involved to be working off a single version of the truth. Companies now say using online FX hedging reports and modelling saves them half to a full day per month – but the exponential value is in greater accuracy and faster, better decisions.

It is these companies that are driving change. They expect their banker to be able be onboard with managing foreign exchange hedging online. They want their broker to see the same information they are and be able to guide them through the options – modelling the different rates and hedging percentages as they go.

Even though cloud technology has driven the access cost right down, online treasury management is new technology for banks to become familiar with. Perennial slow adopters, banks are now realising they need to get onboard fast, or their customers will leave them behind – quite literally.

It really should be a win-win for everyone. Customers limit their FX risk and banks become even more valuable and responsive to their customers. It enables much better FX hedging decisions to be made faster and strengthens the banks relationship with its customers. A definite change for the better.

Starting and running a business is no small feat, and as we all know, cash flow is the core fuel that powers any business. A set marker for identifying a healthy and thriving business is strong cash flow, and the importance of this particular resource is not lost upon any entrepreneur

They say that the first five years are extremely crucial for any business, and generally determine whether a company will crash or float. The question therein is why do various businesses that have a strong financial foundation and good initial investment, end up failing within five years?

The answer to this simply lies in their cash flow, so much so, that a recent study conducted in the US concluded that 82% of the time, poor cash flow management ends up contributing to the failure of an SME.

To understand how SMEs can manage their cashflow effectively, let us first take a look at the challenges:

Cash flow management challenges faced by SMEs

Underestimating Start-Up Costs: Having unrealistic estimates and low cash reserve gets most SMEs started on the wrong foot. Obtaining capital and then not calculating realistic costs becomes like quicksand – quite difficult to get out of.

Managing Receivables: Receivables, as most are aware, is the amount that is due to a company. Inefficient management of it ends up in a huge amount of outstanding receivables, which end up hampering cash flow.

Managing Payments Efficiently: According to a study, almost 66% of SMEs revealed that the biggest impact on their company’s cash flow is due to the amount of time that it takes for money to process post receiving payments, with some of them having to wait more than 30 days for payments to clear. Thus, due to the time taken, if not managed well, it becomes a huge cash flow challenge for upcoming and ongoing projects.

Ignoring Overhead Costs: A company with high overhead costs such as rental, travel, etc. will notice the profits depleting quickly. To cover such costs and break even, the organization will have to and hence, make more sales. Thus, to make a long-term difference to the business’s profitability and cash flow, overhead costs cannot be overlooked.

Low-Profit Margins: While they say that pricing is an art, the first step is always understanding your numbers. This means that knowing your profit margin is an extremely important metric for analyzing your prices. A low-profit margin implies that either business’s costs are too high or the pricing is too low or it could even be both. The lack of a sustainable and strong profit margin means that a business will always battle cash flow issues.

Having talked about the cash flow challenges faced by SMEs, let us talk about how FinTech can assist in overcoming them.

5 ways FinTech helps small businesses better manage their cashflow

Easier Business Lending: Traditional lenders, usually hesitate when handing out loans to SMEs with smaller loan amounts and what they consider to be inconsistent earnings, thus risky. Apart from this, the entire application process for the loan is quite time-consuming and cumbersome. With the advent of FinTechs, it has now become easier for SMEs to bypass the conventional loan obtaining methods and scale their operations faster owing to easier business lending. Thus, bridging the gap, with offerings such as through P2P lending platforms, FinTechs are making the lending space much more dynamic.

Simplified and Faster Invoicing Systems: Having access to simplified and faster-invoicing systems, it is now easier for businesses to thrive. Besides saving them from existing revenue losses or accumulation of bad debts, an efficient management system helps firms collect payments effectively, irrespective of the location or currency, thus, creating a sustainable flow of operations and cash flow.

Efficient Account Management Tools: Owing to FinTechs, SMEs now have access to a lot of options to help them control their costs and expenses. With the help of online accounting systems, they can monitor their cash flow in real-time, and ensure the smooth running of operations. Taking out the guesswork from running the business, FinTechs with the help of expenses and invoices apps, aid business owners in focusing on expansion and growth instead of other small details.

Transparency: The proliferation of the internet and mobile, has helped FinTechs in creating digital banking solutions that reduce both the cost of transferring funds as well as the need for paper currency for conducting any kind of financial transaction. This aids in making the financial system much more transparent, and reduces the chances of tax evasion or other negative practices, thus ensuring that the business ecosystem becomes robust.

Increased Profit Potential: Post the advent of FinTechs, capital markets have witnessed a huge growth in terms of technology infrastructure. Irrespective of the industry or the type of organization, a reduction in costs ends up aiding an increase in revenue and profits eventually. The union of technology and finance has led to the rise of trading platforms that via ‘collection and analysis of market’ and ‘user data’ can help in uncovering trends, providing aggregated views of the market, and enhancing forecasting capabilities that eventually maximize the profit potential for firms and traders alike.

With FinTechs now making it possible for businesses to serve their clients irrespective of location, monumental strides have been made in the areas of payments, inventory management, invoicing, cost-reduction, etc. which were previously unimaginable. Many components of FinTech are now intertwined in business operations that can help in cash flow management for SMEs tremendously. Thus, offering capabilities to leverage technology, FinTechs can really make a difference for companies in keeping their cash flow positive even in times of crisis.

Digital banking has reached such levels of disruption that the disrupted are unaware of disruptors racing ahead.

By Indranil Basu Roy, Chief Business Officer, Modefin

Next to the “new normal,” the most overused term could be digital banking. What’s the tipping point of technology or service delivery that makes a bank truly digital? Net banking? Yes and No, as its entry dates to an earlier era. App-based access? You must be joking. Cashless payments… now we are talking.

Indranil Basu Roy, Chief Business Officer, Modefin

Let’s take one step back to understand digital banking. Over time, as fintech progressed from state-of-the-art, to cutting edge, to leading edge, services offered by banks migrated from conventional delivery channels to online.

Banks, in their eagerness to keep pace, ensured they incorporated every facet of digital banking in their ecosystem. Somewhere down the line, the music stopped. After all, customers were not complaining – no branch visits, no staying on hold in the helpline, no relationship manager to deal with – banking was no longer a chore but a breeze.

Not just retail or personal banking, the transformation had encompassed corporate banking as well, and had eased the procedures in document-oriented products such as Trade Finance.

Should we conclude that all is well, and congratulate the fraternity? Can we compliment the far-thinking CTOs and CMDs on their vision for digitization? Can we name the top 10 digital-driven banks and announce such other lists that make the jury glow and winners feel good?

If we do, we are falling into the trap that others have already got into. Let’s get this straight, digital banking has reached such levels of disruption that the disrupted are unaware of disruptors racing ahead.

As a banking institution, how do you gauge or ensure you are not left behind? Here are three test questions (don’t look for synergy, this is a random round):

How equipped are you to compete with a wholly-digital bank that does not have a single brick and mortar branch?

To enhance your digital capability, has your bank partnered with, or invested into non-financial players, such as a fintech enterprise, data analytics firm, mortgage-software start up or any other disruptor?

Here are five terminologies that are the latest in fintech applications: If you have to look up any, you are labeled “behind,” if you have implemented one or more you are “ahead.”

Here we go: Social Banking, Digital Queue, Conversational Banking, Peer to Peer Payment Systems, Facial Recognition Banking.

Assuming that banks cannot endlessly invest in technology (tech is not their domain) the answer is cross-industry collaboration with fintech players who focus on agile solutions. If the engagement process gets further delayed, the next wave will be fintechs playing the role of banks in certain product areas (we already have several online lending platforms which are not backed by a bank). Look closely, lending platforms of today are replicating services that banks pioneered five years ago by offering instant loans based on a review of credit history.

Looking back, IBM, the one-time mainframe behemoth, proved elephants can dance by making a dramatic turnaround in the mid-1990s. Now is the turn of mammoth banks to appreciate that digital transformation calls for more than online banking. If not, they may as well recall the story of a humble ant that troubled the mighty elephant by entering its trunk (can’t think of a better disruptor-disrupted metaphor).

Beyond folklore and stories of yore, here’s a reality check reflected in a research report on ‘Digital Banking in Asia,’ published by Mckinsey & Company:

“The disruption caused by digitization can create or destroy significant value for banks, depending on their starting positions and how well they respond to shifting consumer behavior and other trends. Experience is showing that 30 to 50 percent of net profit is at risk.”

The findings are disquieting. Rather than assuage your anxiety, I end with a call to action. Start with an audit of your bank’s digital platforms and products, benchmark against the best in the industry, get to know where you feature, and get to work on greater transformation.

If the fraternity fails to keep pace, faster adapters, disruptors and other innovators will get ahead. No marks for guessing who could laugh all the way to the bank.