Cybercrime is an ever-increasing risk for financial institutions. While the wealth management industry has thus far been less affected by major breaches than other sectors, wealth managers should be arming themselves with the right tools in the fight against hackers.

A DDoS attack is one of the biggest cyber threats currently faced by fintech companies. This ‘distributed denial of service’ occurs when cybercriminals flood a website with traffic in order to overwhelm it and shut down services. The very nature of their business makes financial institutions an obvious target for hackers; attacks are relatively easy to launch and smaller companies’ systems can be overwhelmed by them.

The motives for these attacks can vary but might include demanding a ransom in return for stopping the attack, or as a diversion to tie up security staff while hackers carry out a more significant assault. The good news for smaller companies is that, unlike their larger rivals, they are unhampered by cumbersome legacy systems. Agility, innovation and collaboration are key to combating cybercrime, and small firms can harness the power of cloud-based DDoS protection services.

It’s all down to your capacity

These services have a huge network capacity so they can filter out large amounts of DDoS traffic without being overwhelmed. This allows legitimate traffic from customers to get through without interruption. This can also be used to intercept scanning activity. ‘Scanning activity’ is used by hackers to attempt to scan a company’s computer systems by sending traffic to its network in the hope of finding software with known vulnerabilities that can be exploited.

Criminals may also try to gain access through social engineering. This often involves emailing or calling staff and tricking them into believing they are talking to a fellow employee. A workforce that isn’t sufficiently trained to know what to monitor for when it comes to phishing emails or other malicious tactics can leave its organisation very exposed.

While social engineering methods pose a major cybersecurity risk for any company, these malicious techniques are theoretically a greater threat to larger organisations with bigger workforces that are harder to train and monitor. Nonetheless, firms of every size and scale should have effective training and processes in place to help mitigate risks.

Combat the criminals

Increasingly sophisticated tools are available to combat the criminal on the street trying to log into, for example, a victim’s online banking or investment portal. A large number of financial services firms now use ‘panic password’ technology to protect their clients, whereby you can enter a special PIN code (i.e. not your actual password) if under duress, that will automatically notify your security teams that you are being coerced. Further to this, the app will appear to continue to work ‘normally’, leading the attacker to believe that they are able to steal funds and transfer them to a particular account.

Another way in which providers can protect clients is via two-factor authentication. Many large financial institutions require some extra information in addition to a password to log on to a service, often a one-time password or PIN that is sent to the customer’s phone via a text message or generated by an app on their smartphone. Other companies offer dedicated security tokens that generate a shortcode on a built-in screen.

Two-factor authentication provides better security than a password alone because even if a hacker can guess a user’s password, they can’t use it unless they have the smartphone or security token as well. This type of technology is relatively low cost, making it perfectly feasible for smaller fintech companies to implement. And in a world that is seeing an alarming rise in the size and scale of cyber attacks, firms must take every step possible to mitigate exposure.

Visa has announced that Revolut is issuing Visa cards to all new customers signing up to its standard prepaid offering. Visa and Revolut have provided contactless Revolut Visa prepaid cards to all 59 Team-GB athletes travelling to PyeongChang as well as the wider Team GB delegation accompanying them.

The card will allow the athletes and staff to complete seamless and secure payments with a simple tap at any contactless-enabled terminal in South Korea and across all the Games venues free of foreign exchange fees.

Suzy Brown, Marketing Director UK & Ireland at Visa, said: “Our exciting relationship with Revolut comes at a time when Visa is making great strides in delivering the next wave of payments innovations for consumers and businesses. It is appropriate then that we have been able to use this partnership to put a Revolut Visa card in the hands of every Team GB athlete and staff member. Visa is accepted in over 46 million merchant locations* worldwide, so the team’s Revolut Visa cards will allow them to make purchases both conveniently and securely when they are in PyeongChang, giving them one less thing to worry about as they aim to do the country proud.”

Launched in July 2015, Revolut now has over one million customers in 30 European countries.

A common goal

“We’re extremely proud to partner with Visa, not least because we share a common goal to use our innovation and technology capabilities to provide a seamless experience for our customers and clients,” said Nikolay Storonsky, Founder and CEO of Revolut. What’s more, with over a million people already signed up to Revolut, we’re very excited that more cardholders will benefit from the control and flexibility we provide.”

Team Visa athletes Elise Christie was among those from Team GB who received the contactless Revolut Visa prepaid cards ahead of travelling to South Korea.

Short-track speed-skater and Team Visa athlete Elise Christie said: “As a professional athlete, I am constantly travelling around the world and it’s easy to take for granted some of the things I have at home. At least while I am in South Korea I can rest assured that I’ll be able to tap to pay with confidence with my Revolut Visa prepaid card, just as I would do when I’m in the UK.”

In addition to providing contactless Revolut Visa prepaid cards to Team GB and as the exclusive payment partner of the Olympic Games, Visa is facilitating and managing the entire payment system infrastructure and network throughout all venues within the Games. This includes more than 1,000 contactless point-of-sale terminals capable of accepting mobile and wearable payments.

* Data provided to Visa by acquiring financial institutions and other third parties.

As the ATM is turning 50 this year, it is at the centre of a massive overhaul of the retail banking landscape. Banks have to completely rethink the way in which they interact with their customers while the digital revolution is taking hold of the sector. The speed at which this change is happening is breath-taking: Data company CACI predicts that the total number of mobile app log-ins by banking customers are going to increase from 427 million in 2015 to 2.3 billion in 2020, while the number of bank branch visits is expected to almost half to 268 million per year over the same period.

With the banking revolution right under way, most ATMs today are still based on a ‘cash and dash’ model with limited additional functionality. However, with the right software strategy, they have the potential to become a cornerstone for the omni-channel banking world as the last remaining touchpoints for banks in the majority of local communities.

Our survey of 13 major ATM operators, representing over 250,000 ATMs in 30 countries, shows that the industry is held back by IT challenges, with the largest one being the continuous change in operating systems. Every time a painful operating system change has been concluded successfully, the next one is already looming on the horizon. Software changes are a challenge in and of themselves, but if they also require changes to the core of the ATM IT hardware – the PC –, the costs for what is basically just a compliance initiative can be very high. The industry’s second biggest nut to crack is change management, as rolling out new functions requires long development times and complex integration with the existing, ageing host systems. Finally, with the sophistication of large scale attacks on the rise, security, especially around malware, is a pressing issue that the sector is currently trying to solve.

The fact of the matter is that the ATM industry needs to re-think the underlying architecture of its systems if it wants the ATM to stay relevant in a modern banking world. The answer to this problem can only be to move away from PC-based hardware to a cloud based model, which would give the ATM technology that is out there the breathing space to innovate at the same speed as other channels such as mobile banking.

In a cloud model, the role of the PC-core is reduced to manage the user interface, while the cloud controls the cash dispenser. This provides a higher level of security as the nerve centre is taken out of the ATM and placed within a safe distance. What is more, ATM functionalities could be based on an ‘app’ approach, which would speed-up product development and allow banks and ATM operators to add more features at lower costs.

Rethinking the system architecture under these premises will allow the ATM to develop its full potential rather than continuing to be a simple ‘cash and dash’ facility. Moving to the cloud would be a natural (and potentially vital) development for the ATM industry and the financial services sector as a whole. The first step in this direction would be for operators to agree and implement a standard API, which would provide a set of protocols for building software applications, specifying how software components should interact.

Cloud technology is high on the agenda of the next industry event ATM and Cash Innovation Europe and there are various other initiatives among the industry that are already well under way; all of which shows us that the cloud is the direction of travel for the ATM of the future.

Entitled. Lazy. Narcissistic. Me, me, me. If you threw those descriptors at anyone on the conference circuit in finance today they’d know exactly what you were talking about. “Millennials”, the tagline that’s a gift that keeps on giving for speakers and strategists. Banks “need” to target Millennials, they say. Give them selfie-pay, give them emoji-themed UIs, give them “bae” and “fleek” and watch them flock to your brand.

What banks and those who perpetuate this gross misunderstanding need to realise is that it’s not just wrong, it’s downright counterproductive. Many times, I’ve sat in a conference hall full of middle-aged bankers and technologists and watched as they tell me what I want. Yes, I am a Millennial but I’m also an individual. Just like not every baby boomer is to blame for the crash of the global economy, not every Millennial loves to take selfies and eat avocado on toast.

Not all snowflakes

As explained by the exceptionally concise Adam Conover, the easiest way to connect with a Millennial is to treat them like every other customer. If you respect their needs, talk to them as if they’re intelligent, well-rounded people and offer them services they desire, you’re going to get on great.

“But,” you may say, holding up the results of yet another survey into the wants and needs of the 18-35 age bracket, “Millennials want rewards, cashback, mobile-first services and convenience.” Why shouldn’t you give them those things?

The answer to that is “of course you should” but why target just Millennials? Those needs are cross-generational. In the UK, 69% of 18-24 year-olds use mobile banking, but 44% of 45-54 year-olds and 30% of 55-64 year-olds also use their mobile to do banking. Customer priorities across all age groups are ease of use (46%), speed (46%) and layout and design (41%).

Banks feel like they need to change their ways to entice young people to their side, worried by the high rate of attrition, but don’t realise that “Millennials” are just as loyal to banks that offer them the services they require. In the US, young people have a higher wallet share with their primary bank than any other generation. When a bank or credit union is found to engage with those users, they experience a boost of 25% or more in wallet share.

Not-so big spenders

The myth of the butterfly-minded young person, flitting from bank to bank spending money on games consoles, mobile phones and Starbucks needs to be addressed, too. 70% of “Millennials” are already saving for their retirement. According to FICO, they’re are also more likely than to have a home equity loan or line of credit, a credit card, financial planning or advisory services or a home mortgage loan.

While research from “The Millennial Mind” (urgh) says that 1 in 3 young people are considering switching their banks, more than half say that their bank isn’t offering anything better than the competition. Another half are looking for technology start-ups to overhaul the industry. Why is that the case? Banks have traditionally never taken a human-first approach to customer interaction.

Technology firms are offer personalised services that interact with their clients at every opportunity. Those in the age bracket of 35 and below are one of the most diverse segments of the global market. In the US, 42% of them identify as non-white, 15% are first-generation immigrants and the population identifying as Hispanic has tripled.

Banks need to re-engineer the way they operate to deliver mobile, personalised and targeted services to all segments of the market. Reducing the needs of one of the largest target demographics to “give them apps, give them selfies, give them shiny things” is a folly. Trying to lump them under one moniker and sell to them as a group, as opposed to a collection of individuals, is a road to failure.

The commercial card sector is growing strongly within a flourishing B2B payments market. Many banks recognise the opportunity that offering commercial cards to clients represents to grow revenues and enhance customer experience. However, there is more potential in commercial card schemes than end-user convenience and provider banks need to understand this by enhancing the technology used to support these schemes.

Today, though, even larger institutions with far-reaching commercial card programmes often lack the necessary systems to analyse spend per account, recognise potential to grow revenues from specific programmes or detect customers that are growing faster.

There are many reasons why banks should consider implementing technology to drive up value for themselves and their customers by achieving smarter insights into their commercial card programmes.

Payment automation

Providers that can give customer decision-makers a dashboard view of where spend is happening and identify trends deliver transparency where it’s most required. Payment automation and the ability to capture all spend types makes financial tracking easier, helping find sources of non-compliant spend and enabling financial directors to act quickly.

Beyond this, banks also have the potential to leverage enhanced technology to underpin commercial card offerings and use that to drive important customer analytics.

Metrics to track performance

Key metrics for a bank to track to improve card delivery and performance in this area while also enhancing client engagement include spend per account (SPA), average transaction value (ATV), operational costs and profitability.

A higher SPA is likely to mean improved profitability and ROI for the issuer and greater client satisfaction with the product. Higher ATV scores generally result in greater profitability for the issuer. Moreover, tracking operational costs helps identify controllable costs which can be rapidly minimised without impacting service, while monitoring profitability helps pinpoint opportunities to extend the surplus of revenue over costs.

Added to this, the technology has the potential to track further metrics. These include delinquency rates, which, if low, offer the potential to increase issuer profitability and end user ROI and also client retention, which, if high, will reduce costs and increase the net present value of accounts booked. Other key metrics include end user cardholder perception and client perception of the banking relationship.

Grow your customer base

Taken together, analysis of these metrics will help banks understand where greater marketing effort is needed and whether the products that the customer is using are fit for purpose. Beyond this, by being able to segment the customer portfolio, marketers can prioritise products and manage incentives to keep growing their existing customer base and share of budget.

Technology alone is not a sales point for any client or commercial card provider. However, the associated benefits from delivering convenience, analytics, speed and efficiency combine to improve client retention and their overall share of wallet.

Great experiences are key in the B2B environment. If a product is easy-to-use and provides added value, customers are less tempted by change. Card owners see their costs of client acquisition fall and lifetime value increase. Payments technology can deliver strong revenue growth for issuers, even within the context of budgetary constraints.

Before we get into the ‘smart’ bit, let’s recap. Tokenization is the security process that most recently unlocked the mobile payments market. All the major ‘OEM Pays’ (Apple Pay, Samsung Pay etc.,) use the technology to secure the transmission of payment data between device and terminal. The process itself however – of replacing sensitive data with unique identifiers which retain the essential information but don’t compromise security – can, in theory, be applied to any kind of transaction, from bank details, to health records, ID numbers – even to the idea of money itself.

The central idea is this: when tokenized, unlawfully intercepted payment authorization data is rendered valueless because it simply isn’t there; it is replaced by a token. This means the data can, in effect, hide in plain sight.

What is a smart token?

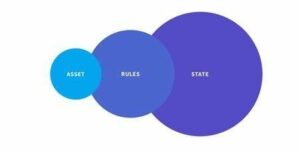

A smart token takes this idea a step further. It’s a regular token on steroids. It transmits the value and all the information needed to authorize the transaction together, in one go, including enhanced counterpart identity, transaction and invoicing data. It consists of three layers: an asset, a set of rules, and a state. Let’s break it down.

An asset is the source of value. Think of it as the ‘center’ of the smart token. Typically, it’s a bank account, such as your current or savings account.

Surrounding this asset are a number of rules. These rules, which can be programmed by the issuer, dictate who can access the asset, at what time, for what purpose and under what set of circumstances.

Imagine you’re buying a TV from Amazon. When you hit ‘buy’, your bank sends a smart token to Amazon which has the following rules: a €1000 payment limit and a two-week expiry date. In another transaction, the smart token issued in relation to the same asset (your bank account) could have completely different rules. If you’re buying a series of weekly Pilates classes, the token may have a six-month duration, enabling your gym to regularly draw down on that token as each class takes place.

That is the great thing about rules – they are the flexible layer that allow smart tokens to create an almost infinite number of unique and secure digital payment types at a fraction of the cost of today’s conventional payments infrastructure. Any existing payment method you can currently imagine – cash, credit card, cheques, and gift cards – can be emulated by a smart token, thanks to the rules. This is the flexibility that opens the door for banks.

Finally, a smart token has a state. This is the part of the token which tracks the value of the token according to its rules. After three months of Pilates classes, it’s the state that will record that 50% your payments have been made. The combination of asset, rules and state combine to provide banks with the power to tear up the rulebook and perform transactions faster and at a vastly reduced cost, without relying on third parties to validate the payment.

Suresh Rajagopalan, President Software Products, Financial Software and Services

The Indian market is one of the world’s fastest growing economies with US$2.2 trillion in GDP but still has more than 85 per cent of personal consumer expenditure made up of cash. Despite its growing middle class and relatively strong cardholder base of 645M cardholders, debit and credit cards usage at point of sale (PoS)) is 1.7 transactions per cardholder in India.

A principal reason for slow progress towards greater adoption of electronic payments is the absence of available acceptance locations, preventing greater usage of and spending via cards. Currently, India has an approximate 2.7M point of sale devices, resulting in spotty and underdeveloped POS infrastructure coverage. Further, the acceptance network and volume that exists is concentrated in India’s primary cities, which account for an estimated 70 per cent of terminals and spend. The India Central Bank has indicated the country needs an approximate 20M POS devices to create a card acceptance infrastructure equal in size to other BRIC countries.

Overcoming barriers to developing acceptance is a key imperative for the country seeking to further expand electronic payments. Currently, an approximate 90 per cent of non-cash payments are processed through established card network infrastructures. At the heart of the traditional POS payment acceptance network is the interchange fee averaging between 0.75 per cent and 2.5 per cent —usually charged by a consumer’s bank to a merchant’s bank to facilitate a card transaction. The rate of electronic payment acceptance is low, as the high processing fee renders the value proposition non-compelling, especially for micro and small merchants, who form the bulk of India’s retail sector, and are the most important in serving low-income consumer segments.

Aadhaar Pay leverages alternate clearing and settlement rails for person-to-merchant transactions originating at the point of sale. Rather than ride on traditional card rails, Aadhaar Pay leverages the real-time interbank network for transaction clearing and settlement. By disintermediating traditional interchanges and riding on less expensive bank rails, Aadhaar-based person to merchant payments lower processing fee and promote higher merchant uptake. The service uses Aadhaar, a unique national identity number issued by the Government to every citizen based on their biometric and demographic information, as a proxy for the customer’s bank account to facilitate transactions at the point of sale.

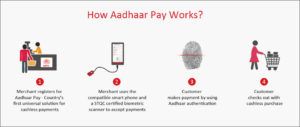

How it Works?

FSS Aadhaar Pay exploits three critical elements — bank accounts, mobility and digital identity — to disrupt traditional POS business models. The service leverages the universal availability of the mobile device and Aadhaar — India’s biometrically-enabled digital identity — that covers 99 per cent of the population to advance the growth of digital payments. Envisaged as an open platform, the Unique Identification Authority of India (UIDAI Stack), allows payment service providers to consume APIs, “on-demand” to authenticate customers. Besides leveraging Aadhaar for establishing user credentials, the national identity also serves as a financial address that can be directly linked to the customer’s bank account.

Any merchant with a biometric reader and an Android phone can download the Aadhaar Pay application, self-register for the service using e-KYC, and start receiving payments. Customers make payments by scanning the fingerprint and entering the amount at the point-of-sale (PoS) terminal. Aadhaar Pay uses Aadhaar APIs to authenticate the customer’s biometric credentials mapped to the social security number. On successful authentication, the transactions are routed to the customer’s issuing bank. In contrast to setting-up a POS terminal, which takes between two and three weeks, FSS Aadhaar Pay takes a few minutes to set-up. Further, the cost of the POS is 80 per cent lower than the cost of the conventional POS terminal.

Delivering a Multiplier Impact

Aadhaar Pay has a multiplier impact on the growth of the acceptance payment ecosystem by bringing quick-to-deploy, mobile-based affordable POS infrastructure to merchants whilst creating a seamless transactional experience for customers.

Specifically, it triggers a virtuous cycle of growth by:

Creating A Ready Market of 900 Million Captive Customers

Traditional acceptance networks need a large base of cardholders to be profitable. In emerging markets with a low base of carded users and unfamiliarity with digital payments, adoption remains slow. On the demand-side, Aadhaar Pay creates a ready addressable market of 900+ million customers by leveraging Aadhaar, as a primary transaction identifier. Customers can initiate payments using their fingerprint and Aadhaar number, eliminating hassles related to downloading multiple apps, swiping cards, remembering PIN/passwords, downloading e-wallets or carrying a phone.

Broadening the Merchant Ecosystem

On the acquirer side, Aadhaar Pay reshapes expensive acquirer distribution models by allowing banks to target previously under-penetrated micro-merchant segments with an efficient technology and commercial framework, easing the way for rapid onboarding and expansion of new acceptance points. The smallest street vendor, with the aid of a basic 2G phone and a fingerprint scanner device, can accept digital payments. To promote rapid uptake, there are no restrictions related to transaction amount, type of business, transaction volume, time, location, demography, and goods category

Offering a Low-Cost Solution

The cost of a point-of-sale (POS) terminal in India ranges between INR 8,000 (USD 120) to INR 12,000 (USD 180); countervailing duties and taxes account for about 20 per cent of the price. In addition, the annual operating cost per terminal ranges between INR 3,000 (USD 45) and INR 4,000 (USD 60). FSS Aadhaar Pay mobile application, in comparison, can be downloaded online even on a 2G Android phone, connected to a biometric reader costing INR 2,000 (USD 30). The significant reduction in Capex and OPEX makes it an ideal solution for all merchant segments, especially micro-merchants with a small turnover and low transaction volumes.

Delivering Differentiated Added Value Services

The “secret ingredient” to engineering the digital payments transformation is software. Hardware can be replicated easily, but software and services are much harder to copy, and this is where Aadhaar Pay brings a sustainable competitive advantage. Beyond the transaction, Aadhaar Pay potentially would take on a more sophisticated, innovative approach to VAS. Merchants, big or small, could benefit from a complete packaged business solution, with the ability to customize specific components. This includes:

support for QR codes

ability to dynamically configure offers and discounts

electronic invoices

analytics and reporting: to sift through payment transactions and make recommendations to merchants for optimal inventory ordering or delivering offers to customers based on buying patterns and preferences.

Settling Transactions in Real-Time

In the traditional interchange four-party payment models, settlement follows a typical T+1 cycle. Aadhaar Pay uses the bank account as a source of funds and all transactions are cleared and settled using the IMPS network (India’s real-time fund transfer network), ensuring immediate crediting of accounts, freeing funds and lowering working capital requirements for merchants.

Lowering Fraud Liability

As AadhaarPay leverages the bank account, it offers a low-risk product, with usage directly linked to the availability of funds in the customer’s account. For acquirers, there is no direct credit risk involved in processing transactions. This significantly lowers fraud liability and enables on-boarding of merchants traditionally deemed high-risk under the conventional acquiring models.

Whilst the service is in the initial rollout stages, Aadhaar Pay removes the multiple layers of friction that, merchants and customers encounter whilst making payments. For banks in India, who have recently opened Jan Dhan (no frills) accounts for the low-income demographic, a broad-based acceptance network would prevent instant encashment and improve the circulation of money in the digital format. Further, with the regulator waiving merchant fees, Aadhaar Pay would help to develop sustainable acceptance that can enhance and fast-track the benefits of electronic payments.

Taking an early lead in the market, FSS launched Aadhaar Pay in April 2017. Currently, one of India’s top merchant acquirers, with an approximate 20 per cent share of the total POS market, has implemented Aadhaar Pay.

Sources

JM Financial Report Card Penetration in India; March 2016

Reserve Bank of India; ATM POS Statistics; June 2017

World Bank, India Report — https://data.worldbank.org/country/india

Notes

A small merchant fee may be levied by UIDAI in the days ahead

Banking is steeped in tradition – particularly when it comes to image. It is hard to think of a dress code that evokes a stronger stereotype than the Gordan Gekko red braces, pinstripe suit and shiny silver cufflinks. But change is afoot, as a new wave of button-loosening fintech firms enter the market – and it is not just the dress code they are changing, it is also the old ways of working.

It is not wholly surprising that the wave of digitisation sweeping the industry has been met with a degree of caution by many senior figures. C-level execs find themselves leading new teams from a generation far more familiar with the technology, and it can be difficult to create a culture of digitisation from the top down.

Adapting to these digital changes and confronting them with efficient solutions across all lines of business is key to ensuring banks remain competitive. Bringing digital capabilities up to speed has become essential to a banks’ ability to adapt to the new market dynamic. However, the level of research and planning required to implement new services puts large banks at an immediate disadvantage. After all, the same rules don’t apply to smaller, younger, more technologically savvy companies without decades of technology debt to carry around. Moving too slow into digital may mean that the damage has already been done and the bank lost out on market share.

Integrated digitisation is necessary

Efforts to digitise can be seen across the industry – voice passwords, user-friendly apps and robo advisers are all positive steps. But for its full potential, digitisation needs to be incorporated throughout, not just in the customer facing channels. Integrating front-to-back technology frees up resources and streamlines business. Scanning paper into a PDF, for example, is not “digital” as it perpetuates content that cannot be easily processed by computers. Encouraging clients to use smart forms and submitting electronic orders, on the other hand, is clearly a better way forward. On top of this, c-level execs need to ensure that they and their employees have an understanding of new technologies while also encouraging innovation in day-to-day activities so that fluidity becomes the norm, taking a leaf out of tech giants books.

A key issue remains as to what the most effective way is to implement digital transformation. Banks who retain a quarterly ‘water-fall’ release cycles find themselves quickly behind the curve. This is why an ‘agile’ approach to IT solutions delivery and change is essential, asking project and IT operations teams to carry out small but very frequent modifications in an iterative process. This calls for a change in the business operating model, bringing the relationship and level of involvement between business and IT much closer to each other. It is a learning curve both ways and takes time to master. Business needs to accept that daily work with agile IT teams is part of their job. IT needs to learn to be much more business savvy. This is a cultural change that needs to be supported accordingly.

Modern technology is like fintech workers are to banking attire, very different from 10 or 20 years ago when many, if not most, current banking platforms were designed. The underlying database and application technologies, and the fundamental engineering behind them, have little to do with how firms such as Amazon, Google and Apple run their IT today. Few IT departments are fully up-to-date on the latest engineering options that could be used to build systems in more efficient and fast ways. As a case in point, the databases and integration fabrics underlying “big data” platforms can be used for building business applications in addition to analytics. All this requires mindset and skillset changes in IT. Going agile, without changing at least some of the technology platforms used to build and operate business applications, is akin to driving in the first gear only. You can get going, but you will not get far fast.

In this article, Fraedom chief commercial officer Henry Pooley shares his top five tips to help banks get more value from their commercial card programme.

1. Embrace Client data

If banks are going to begin to capitalize on opportunities within the fast-growing commercial banking sector, they must begin to achieve a fuller understanding and more comprehensive insight into their clients’ purchasing patterns and trends.

Client data is a tool that cannot afford to be underutilised, it allows banks to monitor parameters such as ‘Average Transaction Value’ (ATV) and ‘Spend Per Account’ (SPA), allowing them effectively to create an in-depth ‘DNA’ of each client. In turn, this enables them to identify potential commercial card opportunities and ultimately maximise the return on investment they can extract and solve any underlying issues such as high delinquency rates.

2. Simplify the payment process

By making the commercial card payment process easier and offering added value such as improvements to working capital, banks can strengthen the hand of the CFO by allowing them to clearly see the true benefits of using this method of payment – which will increase expenditure flows

Issuing banks must realise that by enhancing the technology used to support these schemes both from the end user and back end perspectives, they can help to drive up revenues.

Currently, many banks are falling short in this respect. Even larger institutions that may have commercial card programmes worth billions of pounds annually, often do not have any systems in place to analyse overall spend per account.

3. Transparency

Transparency is always highly valued, yet remains rare in the world of commercial finance. CFOs struggle to manage the constant stream of time consuming reporting techniques from different sources.

Issuers that can clearly highlight and track spending so CFOs can see at-a-glance where spend is happening, identify trends and dial up or down approval controls help deliver transparency and trust where it is most required. Payments automation and the ability to capture all spend types, not just card-based, makes financial tracking easier and more efficient, finding sources of non-compliant spend (leakage) and enabling financial directors to act quickly.

Even beyond this focus on the brand, banks have the potential to leverage enhanced technology to underpin their commercial card offerings and to use that to drive critically important customer analytics

4. Track the key metrics

Spend per account, average transaction value, operational costs and profitability are all key metrics for a bank to track to improve card delivery and performance in this area while also enhancing client engagement.

A higher SPA is likely to mean improved profitability and ROI for the issuer, greater client satisfaction with the product and better client references. Higher average transaction value (ATV) scores generally result in greater profitability for the issuer. Moreover, tracking operational costs help identify controllable costs which can be rapidly minimised without impacting service levels while monitoring profitability helps to pinpoint immediate opportunities to extend the surplus of revenue over costs.

Added to this, the technology also offers the opportunity to track further metrics from delinquency rates which if kept low offer the potential to increase issuer profitability and end user ROI to client retention which if kept high will substantially reduce costs.

5. Customers love a great experience

While technology might not be a direct selling point for any client or commercial card issuer, the associated benefits from delivering convenience, analytics, speed and efficiency cannot be underestimated.

Great experiences are as important in the B2B environment as they are in B2C sectors. If a product is easy to use and provides added value, customers are far less tempted by change. Card owners see their costs of client acquisition fall and lifetime value increase. Payments technology can deliver strong revenue growth for issuers, even within the context of budgetary constraints.

I do not pretend to be an expert in Distributed Ledger and Blockchain technology, however, I do see the huge potential in it. Although, in my opinion, currently only a select few can truly understand how the technology works and its applications, the same can be said about the internet, mobile phones and computers, back in the day. We live in an age where data is king and any move to protect that a good one, surely?

As mentioned, I do not hail from Silicon Valley and my first language is not Javascript. My job is to look and analyse investment trends and find ways to grow and protect my clients’ wealth. It is very apparent that over the last few years, cryptocurrencies like Bitcoin and Ether have been an increasingly popular ‘alternative’ to fiat currencies. It is very difficult to get the exact figures but I think it is safe to say that there have been more first-time investors, men and women who have never invested before, in cryptocurrencies than any other asset class. But do they really know what they are investing in?

The technology, and as a result, the currencies, were originally intended to form an easy way to make payments without the middleman taking a cut of your hard earned money. How long has it taken for that to fall by the wayside? Cryptocurrency exchanges are charging around 4% to buy and sell cryptocurrencies which is completely contradictory to why it was initially developed. And so begins other people making money off the back of new technology.

You may not be so lucky next time

I have seen my fair share of tech bubble bursts so am fully prepared for what is to come. I have experienced it first hand and I have to say, it is not pretty. I was one of the thousands and thousands of people who invested heavily in these new tech companies back in the late 90s and early 00s. I was also fortunate enough to have got out just at the right time because I was buying my first property. I know the signs and what I predict is a “Cryptocrash”.

The huge valuation of the currencies are not sustainable and with previous tech crashes, we have seen drops of around 90%. We have no reason to disbelieve that this won’t happen again. Mark my words – Cryptocurrency will be the next 2001 telco crash or the 2000-2002 dot-com crash. We are seeing the same symptoms – volatile spikes and crashes, huge amounts of money being invested, huge valuations. The fact that most savvy spokespeople and investors have all said that they do not know which way this is going to go should ring a few alarm bells.

Those in their 20s have never experienced a crash in the market before so they believe the hype and drive it up even more. You learn through experience in this game and the longer you go from a crisis the higher the number of market participants have never experienced a crash – this fuels the bubble further and means when the crash comes it will be much larger.

It doesn’t end with cryptocurrencies

It is not just cryptocurrencies, companies like Monzo and Revolut are developing pioneering technology but how long will they last? How long before the technology they develop is benefitted from by others? Ask Jeeves, Alta Vista, Lycos, AOL – same thing happened – the charts look almost identical to that of Bitcoin, Ether, Litecoin. The technology behind them was pioneering, however, other people benefitted from the development and where are they now?

We are living in very interesting times and are currently entering a behavioural finance phase driven by a herd mentality. This has the potential to be catastrophic but there will be lots of opportunities available. The real value and longevity is in the technology, not Cryptocurrencies. I predict the crash happening within the next 18-24 months. In the meantime, ride the wave but be prepared to cash out.

Entitled. Lazy. Narcissistic. Me, me, me. If you threw those descriptors at anyone on the conference circuit in finance today they’d know exactly what you were talking about. “Millennials”, the tagline that’s a gift that keeps on giving for speakers and strategists. Banks “need” to target Millennials, they say. Give them selfie-pay, give them emoji-themed UIs, give them “bae” and “fleek” and watch them flock to your brand.

Entitled. Lazy. Narcissistic. Me, me, me. If you threw those descriptors at anyone on the conference circuit in finance today they’d know exactly what you were talking about. “Millennials”, the tagline that’s a gift that keeps on giving for speakers and strategists. Banks “need” to target Millennials, they say. Give them selfie-pay, give them emoji-themed UIs, give them “bae” and “fleek” and watch them flock to your brand. The commercial card sector is growing strongly within a flourishing B2B payments market. Many banks recognise the opportunity that offering commercial cards to clients represents to grow revenues and enhance customer experience. However, there is more potential in commercial card schemes than end-user convenience and provider banks need to understand this by enhancing the technology used to support these schemes.

The commercial card sector is growing strongly within a flourishing B2B payments market. Many banks recognise the opportunity that offering commercial cards to clients represents to grow revenues and enhance customer experience. However, there is more potential in commercial card schemes than end-user convenience and provider banks need to understand this by enhancing the technology used to support these schemes. Before we get into the ‘smart’ bit, let’s recap. Tokenization is the security process that most recently unlocked the mobile payments market. All the major ‘OEM Pays’ (Apple Pay, Samsung Pay etc.,) use the technology to secure the transmission of payment data between device and terminal. The process itself however – of replacing sensitive data with unique identifiers which retain the essential information but don’t compromise security – can, in theory, be applied to any kind of transaction, from bank details, to health records, ID numbers – even to the idea of money itself.

Before we get into the ‘smart’ bit, let’s recap. Tokenization is the security process that most recently unlocked the mobile payments market. All the major ‘OEM Pays’ (Apple Pay, Samsung Pay etc.,) use the technology to secure the transmission of payment data between device and terminal. The process itself however – of replacing sensitive data with unique identifiers which retain the essential information but don’t compromise security – can, in theory, be applied to any kind of transaction, from bank details, to health records, ID numbers – even to the idea of money itself.