For a start, companies have moved from being hands-off to hands-on in managing their forecasts and FX hedging. It is seen as a concern across the business, impacting sales, procurement, and the supply chain. While the C-Suite are aware of the impact, it is often the board that is driving change in wanting to see a far more proactive approach in managing these risks.

The increased volatility in financial markets, is matched by increased uncertainty in business. Once stable supply chains now operate on much shakier terms if they haven’t disappeared altogether. It means there is no longer certainty around when you will be making a payment or how long you will need to hedge.

Richard Eaddy, CEO, Hedgebook

Businesses working on low margins can be significantly impacted. A cancelled order or significant swing in foreign exchange that has not been hedged, leaves the business dangerously exposed. All of this has meant UK companies are looking more regularly at their hedging positions and reviewing the risk.

Many businesses are acting responsibly and adding FX Management to their library of risk management policies. This gives the treasury team some real guidance as to the risk tolerance the business is prepared to work within. The ability to model FX hedging options against this policy enables faster and better decisions to be made – with minimised risk.

Remote working also removed the expectation of a monthly or quarterly meeting where such matters were generally discussed. The traditional round-the-table closed door reviews essentially disappeared during lockdown.

Very quickly, companies realised the need to proactively review their FX hedging positions and that players across the company needed to part of that. Over 80% of surveyed customers using our FX tools now engage with them at least once a month, with 10% checking in on a daily basis.

Working remotely has also seen companies move away from spreadsheets being the default tool for managing FX hedging. This is largely due to the increased risk around version control and data security when shared across multiple screens and locations.

But it also highlighted the spreadsheet owner as a potential single point of failure in the organisation. In many cases they were the only ones who could successfully run the formulas and manage the complex hedging situations the business was facing. As a result, companies have proactively started looking for online tools capable of managing this for them.

They want to view data in real time, have secure access to their hedging positions and for everyone involved to be working off a single version of the truth. Companies now say using online FX hedging reports and modelling saves them half to a full day per month – but the exponential value is in greater accuracy and faster, better decisions.

It is these companies that are driving change. They expect their banker to be able be onboard with managing foreign exchange hedging online. They want their broker to see the same information they are and be able to guide them through the options – modelling the different rates and hedging percentages as they go.

Even though cloud technology has driven the access cost right down, online treasury management is new technology for banks to become familiar with. Perennial slow adopters, banks are now realising they need to get onboard fast, or their customers will leave them behind – quite literally.

It really should be a win-win for everyone. Customers limit their FX risk and banks become even more valuable and responsive to their customers. It enables much better FX hedging decisions to be made faster and strengthens the bank’s relationship with its customers. A definite change for the better.

IBS Intelligence is partnering with Sopra Banking Software to promote the Sopra Banking Summit, which takes place 18-22 October 2021. The summit is tackling the biggest issues in the financial sector. This weeklong festival of FinTech will touch on the hottest topics in financial services and highlight the new paths industry leaders are taking.

Financial inclusion – its efficacy, implication and urgency – is becoming one of our industry’s biggest talking points. And this is a good thing. The more light that’s shed on the issue, the more likely we are as a collective to push its agenda.

by Nelly Kambiwa, Financial Inclusion Director MEA, Sopra Banking Software

However, there are still question marks over what exactly financial inclusion means. For some, it’s tied intrinsically to demographics; for others, it’s about politics. Most interpretations are not wrong, and almost all are well meaning, but perhaps the clearest and most succinct definition comes from the World Bank:

“Financial inclusion means that individuals and businesses have access to useful and affordable financial products and services that meet their needs – transactions, payments, savings, credit and insurance – delivered in a responsible and sustainable way.”

Nelly Kambiwa, Financial Inclusion Director MEA, Sopra Banking Software

Without this ‘access to useful and affordable financial products and services,’ people may not have a secure place to store money, no effective and free means of receiving payment, and no safe, reliable way to make payments.

And while great strides have been made around financial inclusion, there’s still a long way to go. According to the most recent Findex data, there are still close to 1.7 billion adults in the world without access to basic financial services

Financial inclusion in Africa

Of course, financial inclusion is not a challenge limited to a particular country, region or continent; rather, it affects areas all over the world. However, for the purposes of this article, we’re going to look at financial inclusion in Africa, and how digital lending can help to improve the financial lives of millions of Africans.

According to Global Finance, 50% of the African population is unbanked, equating to 350 million people. This is already a problem that needs addressing, but with the African population rising quickly – it’s set to double over the next 30 years, adding an additional 1 billion people – it could quickly go from bad to worse.

The role of digital in expanding access

Extending access to borrowers who are otherwise unlikely to receive it is key to improving the health of a society. Among all financial services, access to credit is perhaps the most important as it’s a force multiplier. To this end, innovative digital strategies and new technologies are enabling lenders to reach traditionally underserved people while securing their own interests.

Indeed, the use of big data, artificial intelligence, machine learning and open banking-enabled solutions is expanding the scope of what’s possible. Thanks to new products and soaring internet penetration rates, geographical limitations are being overcome. More sophisticated data analysis tools have come online and are enabling easier credit decisions in lieu of traditional credit scores.

This is particularly relevant to lending in Africa, where access to physical branches is an issue for many people. A recent white paper published by Sopra Banking explained how the rise in mobile money users in Africa is an opportunity and challenge that many incumbent financial institutions have yet to rise to.

Thankfully, that is changing, and many lenders are coming up with solutions that will allow them to provide digital loans to their customers in a safe and effective way for all parties. With the introduction of video KYC and account aggregators, lenders can easily access permissioned customer data and conduct better due diligence. And the digitization of the entire loan application lifecycle means that borrowers can apply for loans remotely—a benefit both in terms of reducing friction and expanding reach.

New-to-credit (NTC) customers

Historically, credit institutions have been cautious with NTC consumers, due to the lack of credit history to assess their probability of default. However, given technological advances, lenders can now more confidently lend to NTC borrowers. They can do this by leveraging some of the solutions mentioned above, solutions that afford new ways of analysing data, predicting a customer’s creditworthiness and gauging the risk involved in lending.

Analysing mobile and web data makes it possible to offer credit to individuals and SMEs without financial footprints. Over the past decade, this practice has emerged and really caught on in Africa, where FinTechs, microfinance institutions and traditional financial institutions like NCBA Group, Equity Bank and Orange Bank use SMS data to inform credit decisions.

While alternative credit scoring systems show great promise, they also bring up privacy and data reliability concerns. And in at least one case, have led to a large group of digital borrowers taking on unsustainable levels of debt.

Open banking as a catalyst

On the regulatory side, open banking is also driving improvement in lending processes. With access to more data (including non-financial data), lenders can do enhanced credit scoring and risk assessment. This provides additional insight, allowing lenders to assess a borrower’s eligibility more accurately. This not only drives down costs for the lender, but it improves the customer experience and, because it’s digital, it works in places without existing infrastructure.

For those most likely to be denied credit, the sub-prime loan application process can still be paper-heavy, involving the manual submission of payslips or statements. Furthermore, Covid-19 has underscored just how inefficient traditional loan processes are.

As an antidote, open banking is pushing financial inclusion solutions that make it easier to verify customer details in real-time—in some cases, going as far as automating the entire interaction. This makes the process easier for the user and significantly increases the chances of applications being accepted.

The good news is that African banks are taking notice of open banking and starting to take huge strides in furthering its implementation. For instance, in 2020, the Central Bank of Kenya – a country where 44% of the population is unbanked – included open banking as one of its main strategic objectives; and last year at the height of the pandemic, Nigerian startup Okra announced that it had received significant funding to develop an open banking infrastructure.

Such developments are becoming increasingly common throughout Africa and bode well for the future of financial inclusion across the continent.

Looking ahead

Digital lending is redefining the dynamics of the credit market in Africa. With a lower cost base and improved reach, financial institutions – including banks, MFIs, neobanks and Telcos – can simply do more with less. Digital lending cuts the cost of offering services and streamlines onboarding. It also enables instantaneous and remote approval and supports data-driven mechanisms to initiate repayment. At the same time, open banking facilitates greater access to data than ever before and unlocks new use cases.

Ultimately, expanding access to credit requires careful planning and is more of a journey than a destination. The use of alternative credit scoring is still in its infancy, and open banking is only a few years old. At its best, digital credit can be responsible, inclusive and affordable. And it’s something every financial institution should strive for, as it not only helps individuals and communities, but it drives economic growth, too.

Digital banking has long been considered the ‘future of banking’. We’ve seen numerous market entrants look to bring customer-led propositions to market to bring the experience customers have come to expect from all their online services.

By Sarah Carver, Head of Digital & Trevor Belstead, CIO Wholesale Banking & Post Trade, Delta Capita

This expectation has increased with the pandemic, which effectively operated a digital-first experiment, forcing banks and customers to embrace it. Over the past year, consumers have got used to doing almost everything online.

Trevor Belstead, CIO Wholesale Banking & Post Trade, Delta Capita

This has led to a fundamental shift in customers’ expectations with them now expecting this level of ease on everything, including their banking. In parallel, banks have seen the potential for both the NPS improvement and reduction in cost to serve through increased self-service by investing in their digital channels.

Digital banking is not a new trend; branch usage has been in a gradual decline as banks have continued to invest in digital channels and reduce branch density. However up until now this customer shift has been a gradual process and the experience (or lack thereof) hasn’t been sufficient to make customers switch en masse to digital challenger banks as their prime account. Albeit many have dipped their toe in the water with Monzo, Starling, Revolut amongst others as a secondary account. However, this shift has sped up over the last year with 27% now having an account with a digital-only bank in the UK.

So why are people opening digital-only accounts? Convenience is, as expected, reason #1 with 26% citing this, closely followed by users wanting a ‘secondary account’ and finally ease of transferring money. However, it’s not all about functionality and servicing; 1 in 10 consumers are still drawn predominantly by the brand, citing the ‘cool cards’ as a reason to get an account. This is a more challenging one for the heritage banks to contend with given their brand values driven by trust, security, steadfastness rather than a challenger which can ooze coolness with a neon or metal card and informal website copy which connects with customers on a more personal level.

Sarah Carver, Head of Digital, Delta Capita

How can heritage banks respond?

Ensure you are not held back by your legacy stack: This is the number one challenge we see with our clients. Where, in the desire to digitise and create that perfect customer experience, there’s a sidestep around their legacy technology. Without tackling this challenge, the spaghetti junction of systems can prevent the organisation from doing anything quickly or add a burden of cost which limits where the spend should be going, which is differentiating that front-end customer experience. It’s perhaps not the most glamourous part of the digital transformation for an organisation but it is a critical one.

Validate tactical tech: At the start of the pandemic, banks had to react and adapt in a very agile and quick manner. Depending on the level of digital maturity many had to quickly spin up digital banking solutions and embed new tech to deliver to their customers. However, now it’s critical to take a step back and ensure that all tech is strategic and integrated in a way that ensures it is future-proofed. This is a particularly challenging area given in some cases there has been large investments made but now is the time to ensure that what you’ve got is not just ‘good enough’ given digital banking will only grow over the coming years.

Really take the time to understand your USP: Partnering has become the standard in the industry with an increased appetite to partner or buy rather than build in-house. This has hugely expedited delivery and has also ensured organisations aren’t investing unnecessary budget in what is ultimately non-differentiating services. However, there is still a need to invest in research and understand your target customers. Stepping back with a critical lens is important because if you streamline your digital journey but it’s still essentially a non-differentiated vanilla offering, you’re not going to see the adoption you expect. This can be through many different guises, new product or service offerings, brand positioning such as sub-brands to target different segments and critically understanding and utilising your data to speak to your customers in a far more targeted way.

Do you have the right business model: The evolution to digital banking is not just technology, it is organisational and business focused as well. To really achieve a digital bank, the organisation itself must become digital and agile across the board. Traditional banking models that were previously used in the branch cannot just shift as is to meet the digital ecosystem the bank needs to operate in. The organisation needs to look at its business model across the board, starting at customer servicing, product development, operations, and technical delivery.

Driven by the accelerating expansion of smartphone capabilities − alongside consumers’ increasing levels of trust − the opportunity for FinTech’s is unravelling at varying speeds across different international markets. Siri Børsum, Global VP of Finance Vertical Eco-development & Partnerships at Huawei Consumer Business Group, explores the ways in which different markets are racing to adjust to this digital revolution, and how smartphones are at its very centre.

When we look at the markets prioritising FinTech’s and their development, across the board we’re seeing waves of innovation, a surge in consumer trust, and a solution to supporting the unbanked. It’s clear that FinTech’s are changing the game, although some markets have recognised this faster than others.

Europe – record-breaking investment, but some serious catching up to do

Siri Børsum, Huawei Consumer Business Group

Let’s take a look at Europe as an interesting example. Considered one of the fastest evolving continents in the FinTech sector, Europe’s capital investment reached a whopping €30 billion between 2014-2019 – Europe’s largest share of equity investment. This fed the growth of online and mobile banking startups, and now, online banking is becoming one of the most popular payment methods in Europe. Investment in this space shows no signs of curtailing, with data showing how the pandemic contributed to the acceleration of cloud services and similar solutions for the industry.

The Nordic FinTech scene, in particular, has shown immense strength. As stated in the FinTech Mundi report, some of the biggest names in financial technology came from the region. Northern Europe alone is home to 993 FinTechs, with several of its countries punching above their weight globally. The FinTech Mundi report also revealed that three Northern European countries (Lithuania, Sweden and Estonia) feature in the Global FinTech Index Ecosystem’s top ten, and all but Iceland feature in the top 50.

Yet, alongside the FinTech investment that we’re seeing in Europe, there’s the sobering realisation that we’re still very far behind. Europe’s FinTech development remains slower than other markets, with a plethora of challenges that need to be addressed. From consumers’ trust in traditional financial systems to relatively low interest rates depriving a mass-market adoption of alternative lending, lucrative investment opportunities are more complicated here − even when we consider the huge number of potential investors.

Banking and mobile technology still feels new in Europe. QR code payments, for example, saw an accelerated uptake as a result of the pandemic. But even now, they’re somewhat futuristic in this market compared to elsewhere, where a QR code payment is standard practice − and it’s been this way for a long time.

China’s flourishing FinTech sector, with smartphones at its core

So, if Europe isn’t leading the digital revolution through its investment and prioritisation of FinTech’s, who is? The answer is China. Thanks to the staggering rise of smartphones and online shopping, China’s FinTech revolution is in full swing, especially in the field of digital payments.

Historically, China has demonstrated fertile ground for a FinTech revolution – it boasts a growing and underserved SME market alongside escalating e-commerce growth. Combine this with a timely explosion in online and mobile popularity (we’re talking about 1.3 billion mobile internet users), and it’s clear why the Chinese market has spearheaded the boom.

We can trace the progression China has made back to 2016, by which stage, 40 per cent of consumers were already using new payment methods rather than traditional ones − 35 per cent of which were using FinTech’s to access products. Going back to QR codes, mobile payments in this way have been commonplace in China for a decade, while Europe’s most common payment method in 2010 was still debit and credit cards.

Now, China is leading in the digital payments and alternative lending sectors, both crucial to the progression of the FinTech industry, and it’s predicted to stay in the lead until at least 2025. Why? The country’s total digital payments transaction value is likely to hit over $4,185 billion by 2025, compared to the world total of $10,520 billion.

China ‘s FinTech success: all-inclusive technology So, what’s the point? Arguably, the most important question when assessing the possibility of FinTech’s is: what are the benefits to the end-user? How will FinTech’s improve our lives? Technology must be used to enhance our lifestyle and drive change in the areas where we need it most.

This is something that FinTech’s are confronting head-on. As more players enter the market, more solutions are becoming available to consumers. China’s FinTech sector for example is driving innovation which is leading to better technology and enhanced consumer experiences. Because of the market’s approach to alternative lending, accounting for 86 per cent of the global share in its transaction value, China can offer smaller FinTech players the chance to compete in a flourishing industry. This, in turn, promotes competition for innovation, which drives choice for consumers.

Markets that are prioritising smaller organisations’ access to funding are also the ones to see that investment returned – China’s growth rate shows no signs of slowing, with estimations that the country will account for a global market share of 88 per cent of Alternative Lending by 2025. The demand for alternative payment solutions will only continue to grow, meaning that as more organisations launch a greater choice of services, we can drive the prospect of global Financial Health into existence. As is always needed when addressing a lack of inclusion, smaller players must disrupt the industries previously dominated by traditional systems.

Open Banking creates innovative technology to connect the dots

From Europe to China, one thing is clear: FinTech startups are driving the financial revolution. And, when looking at achieving Global Financial Health, there’s an obvious solution at our fingertips. It’s never been more important to champion the smaller FinTechs and facilitate technologies such as Open Banking. This is something we’re committed to at Huawei, partnering with FinTech providers to support their development and growth while also offering our mobile users’ access to a choice of the services that they need the most.

Open Banking is a product of the growing competition and consumer-centric model in the FinTech sector, and a bridge to connect the technologies needed to meet customer expectations. It has the potential to help banks learn about customers’ patterns of behaviour, financial health and investment plans and goals, enabling them to create better services and products.

Industry leaders are being advised to make strategic partnerships to make the most from Open Banking, identifying new capabilities from partners that can help to enable compliance and operational readiness. Through forming third-party partnerships and gaining access to new resources including data-sharing, organisations can create more competitive products, services and experiences for end-users. We believe that we’re only at the start of an Open Banking future and better global financial health, and more competition in the FinTech sector will only help to drive this journey.

Driving global financial health for all

Financial Health means all individuals, businesses and organisations around the world having access to a choice of the financial services that work best for them. It’s our vision for the finance industry, and a top priority with AppGallery.

To drive Financial Health, FinTechs and banks around the world need access to a global audience, as well as the full-spectrum support, advanced technological capabilities and commercial opportunities needed to help them grow.

After three years, AppGallery is the third-largest app marketplace globally, with over 540 million MAU, so banking and FinTech app developers can trust that they’re tapping into a truly global audience from launch.

It’s through partnerships, competition and mobile technology that we, as an industry, can achieve global financial health together, bringing better solutions to every home, business and organisation.

Siri Børsum Global VP of Finance Vertical Eco-development & Partnerships

Huawei Consumer Business Group

Cloud is one area of innovation that holds huge potential for the financial sector and that can offer significant cost savings if used effectively.

By Tom Schröder, Director International Partners and Strategic Alliances, Serviceware

According to McKinsey’s Consumer Pulse Survey, digital engagement levels among European customers have increased by 20% since the beginning of the pandemic. However, despite the need to innovate, many financial organisations are yet to fully recover from the full impacts of Covid-19. Whilst vaccine roll-out has signalled fresh hope for some, recovery will be by no means immediate. With further economic turbulence on the horizon, it is crucial that financial services businesses leverage strategic cost measures to not only mitigate the impact of short-term pandemic fallout, but most importantly recover and succeed in the long-term.

Balancing cost and innovation

Many financial institutions already use cloud-based software for business processes such as customer relationship management, HR and financial accounting. However, the opportunity for cloud within core activities such as consumer payments, credit scoring, statements and billing is endless. In fact, from 2016 to 2018, Deloitte Global saw a threefold increase in the number of financial organisations adopting cloud to promote innovation.

Tom Schröder, Director International Partners and Strategic Alliances, Serviceware

Cloud-based services can reduce internal costs and optimise business growth by offering a much more scalable and reliable IT infrastructure that is specifically designed to streamline performance and support development and expansion. Cloud technology gives financial institutions the opportunity to continuously refine and improve services, according to changing customer demand and business need, whilst enabling them to assess how much is being used versus how much is being spent. For many organisations, cloud also provides the opportunity to achieve better value for money, as businesses only pay for what is being used.

With cloud now being seen as the digital backbone of many financial businesses, cloud solutions will continue to evolve. However, with this change will come increasing complexities – both in terms of the services available and also the variety of operating models. It is therefore essential that financial institutions have the right tools to continually monitor and analyse cloud spend (on average, 23% of IT expenses), in real-time, and with accuracy. Those who do will effectively pave the way towards growth.

Managing legacy spend

In today’s current economic landscape, optimising budgets is an absolute necessity. However, traditional ways of managing IT spend are simply not working. This is where maintaining a complete view across the whole organisation is required. The ability to manage cloud costs will be unlocked by reliable financial management tools, which can empower the financial industry to truly understand and evaluate cloud spend. By gathering real-time operational, project and vendor cost data, financial institutions will be well-equipped to make fact-based decisions to drive down costs – both now and in the future. From our experience, we’ve seen our clients easily shrink their running costs by 5% and reallocate these resources to more appealing and business-driving growth initiatives.

In light of these changes, financial companies must now take advantage of the tools that will enable them to evaluate the implementation and operational costs of technology to help stabilise business – including cloud, on-premise and even shadow IT. Whilst in theory, all software and IT assets within a business should fall under one centralised IT department, providing the CIO with ultimate visibility, the reality is often very different. Shadow IT, incurred in part by bring-your-own-device increase and the explosion of remote working, has seen a rapid rise and Gartner predicts it now accounts for 30-40% of IT spend in large organisations. As such, this is causing an ongoing headache for the people that are in charge of technology, security, and compliance, who need transparency across all applications to ensure cost transparency against value, not to mention security.

As we look to the year ahead, and competition within the industry continues to rise, it is vital that financial institutions free up budget to invest in digital programmes and secure growth. To achieve this, it is imperative to gain total transparency over business costs. This will be essential for companies to not only stay afloat, but also build for a successful future.

For many businesses, an integrated, high-performance and, above all, flexible solution is needed to create a holistic overview of business spend, on which decisions (about cost, process, operations and more) can be based. If that means an initial investment to analyse the value of legacy systems vs cloud-based solutions, then it’s a cost easily justified. Put simply, financial institutions that maintain an end-to-end view across their entire IT portfolio will be able to take back control of their running costs and streamline their budgets towards future growth – this year and beyond.

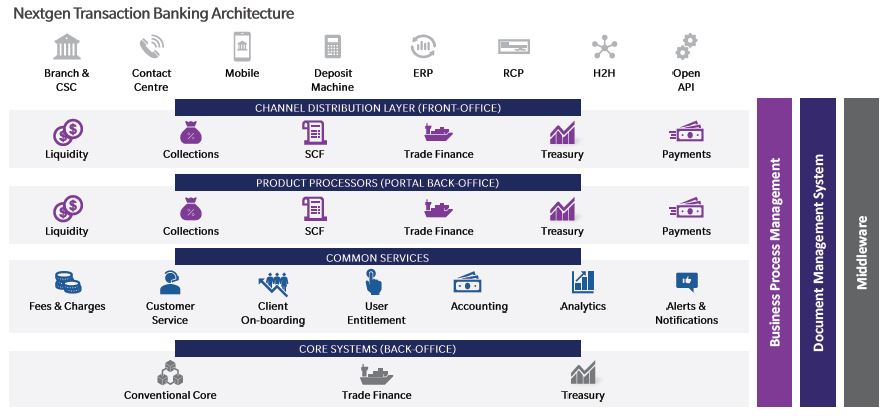

As corporate banks look towards a post-Covid era, what Innovations should transaction banking heads fast track in 2021?

By Chetan Parekh, Partner Cedar Management Consulting International LLC

Covid-19 slowed down corporate and institutional business and, together with lower interest rates, has created a margin squeeze for corporate banks. Corporate income pools are shifting in a big way from interest to fees-based income from global transaction banking (GTB) services. GTB platforms have not only become important from the fee income perspective but they also enable corporate banks to lower costs due to innovation and STP enablement. GTB cash management services like liquidity management, collections, receivables, and payments are expected to contribute 60-70% of global transaction banking market revenues followed by trade finance and supply chain. This is a $1 trillion opportunity globally and worth $8 billion in the Middle East, according to recent research.

GTB business services are going through disruption with FinTechs, which are playing a pivotal role, providing both complementary and competitive offerings to corporate banks. Areas such as trade finance and supply chain finance are moving from paper-based documentary credit business to blockchain-based smart contracts. Even banks’ supply chain finance businesses are moving from simple factoring products and supplier financing products to innovative buyer-led programmes, reducing the cost of risk for global corporate banks.

Why innovate?

It is imperative that banks look to digitising their corporate banking transaction volumes in order to remain competitive and improve accuracy and speed of transaction. The digital revolution is affecting the business at large and the choice is simple: either to be the disruptor or the disrupted! Innovation in services for a disruptor can offer an edge. Hence, many corporate banks are structurally moving income pools from interest to fees-based services through FinTech innovations. Note that JP Morgan invests $11 billion annually in ‘Future Tech’ to drive innovation.

How to innovate?

There are two major ways for corporate banks to transform their platforms: building a digital platform of choice using ‘agile’ practices greenfield; or, second, “buy/partner” with GTB platform and FinTech solutions. Each model comes with its pros and cons, and suitability based on size of bank, its clients, and its capabilities. For example, French bank BNP Paribas transformed and innovated its GTB platform with the latter approach, with an eco-system of FinTech players and a platform of repute from global solutions provider Finastra.

Innovation requires a bank to identify segments and key unmet needs or pain points and then apply a design thinking-based approach to identify and build solutions. FinTechs can be very handy to reduce time to build and provide sustainable solutions over the cloud. Most FinTech programmes have only 90-180 days launch time, offering quick-tomarket solutions for large corporates and SMEs.

Banks must start to innovate by building an architectural blueprint, which is flexible at multiple layers from front, middle and back offices, including common services and de-coupling, and leveraging their back office platforms like core banking, treasury, and trade finance. The plan should allow corporate banks to have multiple vendor solutions that can co-exist from build to buy and partnering with FinTechs through API based integrations through Open API.

Innovation 1 | Open B2B APIs

Many banks over the years have built monolithic transaction banking systems and proprietary Host-2-Host adapters with their corporate customers. These are now giving way to API-based B2B services. This is not only faster but much more economical. In a recent survey of banking executives, more than 60% of them are investing in B2B API solutions.

There is a clear business case for the B2B APIs in the areas of cash management, payments, invoice reconciliation, and working capital financing. The platforms being rolled out globally by regulators and, for example, unified payment systems in India are enabling banks to further leverage API platforms. Once moved onto a B2B API platform, a bank may consider how expensive and cumbersome H2H proprietary platforms may be retired in a phased manner.

Innovation 2 | Build smart onboarding by segment

Corporate banks have traditionally followed an RM and branch/ service centre-based opening of relationship. The time has come to innovate across segments and build a digital onboarding solution. Banks should look to develop a solution for self-service onboarding for small and medium size corporates in partnership with local chambers of commerce and registrars of companies along with start-of-the-art authentication solutions. Consider innovations such as “Click and Sign” (as already approved by the European Union). You may also bundle a small to medium size ERP solution.

Develop assisted onboarding for medium and large corporate and institutional clients, allowing RMs to have tablet-based apps with information services such as Moody’s being integrated for credit appraisal information. The objective here should be to make your RM invest most time in relationship building and offering customised solutions, and let his tablet CRM do the onboarding!

Innovation 3 | Drive your digital SME bank

The SME sector is an important business segment for corporate banks with 80-85% of clients falling within this segment for commercial banks. Financial institutions should strongly consider offering a digital SME banking solution, whereby onboarding, account services, salary processing, payments and certain basic trade services are offered through a digital platform well supported by virtual RMs and BOTs.

Innovation 4 | Digitise through blockchain and smart contracts

The trade finance business is being disrupted. Blockchain and distributed ledgers are here to stay. Documentation secured delivery and contracting were material pain points in the industry which are resolved through a consortium-based approach. Invest carefully, adoption needs to be measured to avoid the pitfall of investing in technology without measurable returns. Know your clients, understand the market realities and counter party readiness to transact. For example, in Citi’s CitiDirect BE trade services portal import L/C are assigned by a counter party digitally and processes automated, reducing both operational cost and the risks involved in physical documentation.

Innovation 5 | Partner with Cloud based SCF Platform with Ecosystem

Up to 10% of the revenue pool of corporate banks will be based on supply chain finance (SCF) products such as factoring, supplier finance, receivables finance and buyer-led programmes. These niche lines of businesses are very interesting and help banks in distributing risk across the SME customer portfolio. Many of these products may be offered via a platform with limited RM or operational interaction. Partnering with an SCF platform, within an ecosystem could be very rewarding for corporate banks as it brings in digitally originated and highly scalable business. Products such as distributor financing and buyer financing are low risk, high income products. There are multiple platforms available from suppliers such as Codix, HPD Lendscape, Neurosoft, Premium Technology, Aranova and Demica to name a select few. Banks also have the option to put this solution on cloud or on premise.

In summary, corporate banks must innovate, developing GTB platforms either by build or buy/partner with FinTech. They should create a flexible GTB system architecture, which allows the bank to invest into FinTech opportunities to build differentiated products and services for its business segments. Investment in next generation technology architecture offers the potential to disrupt the market, acquire clients at rapid pace and lead the way for industry rather than being disrupted!

Digital-first pressure for banks is well and truly on. Leading financial institutions know they must lead in both customer experience and operations en route to a digital-first future, while also recognising these as areas of strength for digital-native challengers and FinTechs.

by David Murphy, Head of Financial Services EMEA & APAC, Publicis Sapient

Today, almost everything is digital. The way we shop, interact, how we bank. A global pandemic made digital capabilities mission-critical, enabling banks to continue efficiently serving their customers remotely. And for the most part, this has been achieved with a great deal of success. However, before the pandemic, many banks were sceptical about their ability to pivot so quickly to a digital-first approach. They knew they needed to, but the ‘How?’ proved difficult as they were bogged down by legacy technology and cultural debt.

David Murphy, Head of Financial Services EMEA & APAC, Publicis Sapient

Banks have been aware of their digital-first future for quite some time, but many have simply struggled to get there, stalling at the first hurdle and giving away valuable market share to a wave of digital natives that are more agile, innovative, and free from the weight of traditional restraints; adapting and pivoting as required. So far, the market has been theirs for the taking, inspired by the likes of Amazon, Netflix and Airbnb which have disrupted entire industry sectors with their digital-first platform approach. They have successfully leveraged technology to create a superior customer value, offering slick and frictionless experiences that have appealed to a new generation of financial customers.

Recent research by Publicis Sapient showed that 83% of banks already have a clearly articulated digital transformation strategy in place, but the pandemic acted as a catalyst to act faster. According to the study, 81% of banks say the pandemic has made improving their digital skills and capabilities more urgent, and 70% say it highlighted weaknesses in their customer experience. Covid-19 has only served to reinforce the gaps in legacy banks’ customer experience and operational transformation. Banks are accelerating to compete with digital-first challengers like Monzo, Revolut, Chime and Nubank, while developing partnerships with FinTechs that can accelerate the provision of new customer propositions. Personetics, a firm that uses data and AI to enable banks to provide personalised insights to their customers is a great example.

Incumbent banks are however, far from complacent. Most say they must do more to keep up with these nimble, digital competitors while appealing to a new breed of digital-native customers. Leaders from the Global Banking Benchmark Study ranked digital-first challengers, FinTechs and consumer tech companies among the top five influencers of their own digital transformation strategy. “FinTech is the future,” as JPMorgan’s CEO, Jamie Dimon, wrote in a memo to shareholders ahead of the bank’s earnings numbers release.

Put simply, banks need to stop aspiring and start acting to counter the new competition ‘head on’ by transforming their technology, investing in appropriately skilled talent needed to make this technology work for them, and emulating the digital-first mindset and culture of the challengers. Crucially, they must digitalise and become truly customer centric. At the most basic level, they need to provide access to their services online and efficiently to customers entirely via digital channels. Not only basic services such as checking balances and making money transfers, but also more complex transactions such as mortgage lending. In this rapidly evolving environment, banks need to deliver superior customer experiences while being operationally agile enough to drive growth and give themselves a fighting chance to compete, which is not always easy. Look at N26, Starling, and Revolut, who have clearly demonstrated their ability to achieve a high level of digital maturity by creating digital-only propositions at speed while innovating on the product cycle in their area of specialization.

Banks need to optimise all areas of their customer experience and operations – from their business models and technology to their products and services and even their people in order to achieve both revenue growth and cost reductions in a post-pandemic world. This will also enable them to compete in an increasingly complex, digital-first financial services landscape. Banking of yesterday has gone, and to cement themselves for the future banks must innovate with customer experience top of mind.

How can banks learn from FinTechs?

Accelerate into a digital-first future. Know the competitive landscape. Banks need to understand their competition, then invest heavily in digital innovation to keep pace with them as digital-first challengers, FinTechs, and new entrants continue to reshape the financial services outlook.

Transform both people and culture. Leading banks recognise that investing in developing talent and skills to transform culture goes hand-in-hand with technology investments – they are not siloed. Lack of skills can be a key barrier to transformation.

Invest in a partner ecosystem and distribution network(s). Building partnerships will allow banks to scale and pivot at speed to compete with digital-first competitors.

Be agile to move and innovate at speed and scale. Leading banks have already grasped this shift and are now focused on building urgency – 40% of banks believe that agile product development is the key trait for digitally innovative financial services firms.

Move to a cloud-based model. Cloud is central to banks’ digital transformation strategies, whether for core modernisation, enabling personalisation or real-time payments. However, banks need to look beyond infrastructure and cost efficiency. Opportunities for customer innovation and cloud-enabled services must be seized. That said, adaptation will take time as sentiments steadily rise, 29% of bank leaders say cloud investment will be central to their digital transformation plans over the next 3 years.

Banks are aware of the impact that these new challengers and market entrants are having on the pace and priorities of their own digital transformation. In turn, flexibility is becoming increasingly important for digital competitiveness in the market. Banks need to prioritise investment in agile capabilities which will allow them to accelerate the rollout of new customer features and innovations.

While banks should not necessarily flock to follow the internal structures of digital competitors, it is crucial that they realise what has made them so successful: customer obsession. They have an established customer-led culture; a 360-view of customer data; they deliver omnichannel servicing and offer personalised experiences and products, but most importantly, they have a platform-based approach. The types of institutions that will be successful in the next 3-5 years are going to be institutions that integrate different parts of a large ecosystem into a platform experience. Banks must use data to deliver an in-depth understanding of the customer and their wants and needs, and banks must service those needs in a streamlined, seamless, ethical, and engaging way.

By learning from challengers on how to become customer centric, they can invest in and improve on their own CX. This requires investment into digital innovation to keep up. The good news is that it can be done. The pandemic has shown that banks can move incredibly fast when required and support their customers almost entirely digitally with no branch access. Customer needs and demands are constantly in flux. An iterative approach which works constantly to improve, update, and respond to customer desires is essential. This approach will see today’s banks best position themselves for the digital-first future.

Manish Patel, Chief Operating Officer, CRM, and James Mitchell, Managing Director (International), Tier1 Financial Solutions discuss why firms need to re-evaluate their technology requirements, and what is driving adoption of advanced CRM and compliance solutions in Europe.

With capital markets firms in EMEA already facing challenges on multiple fronts, why should they reassess their technology needs? And how has the Covid pandemic impacted working practices?

James Mitchell, Managing Director (International), Tier1 Financial Solutions

James Mitchell (JM): “There’s tremendous pressure on banks worldwide to deliver more with less. This is a pressing issue in EMEA, where research, sales and trading desks have seen budgets slashed and teams downsized. Many do not have the infrastructure to support advanced FinTech solutions that would enable them to maximise the value derived from client data, automate workflows and increase firm-wide collaboration.”

Manish Patel (MP): “The Covid pandemic highlighted the urgent need for digital transformation in capital markets. A year ago, we witnessed the rapid dispersal of entire workforces from the heart of Europe’s financial centres to remote environments, which in most cases meant home.

“Firms that were already well into their digital transformation journey, with tried and tested, integrated cloud-based systems in place, were able to adapt quickly. But for businesses heavily reliant on legacy systems and manual processes, the switch was far more challenging – not least because of the very specific and stringent security and compliance requirements of capital markets.

“As vaccine rollouts proceed and firms plan their tentative return to the office, they will need to decide which model – working from home, in the office or a hybrid of the two – is most appropriate for the business, its employees and clients. To ensure the business is flexible enough to adapt to changing circumstances, it will need robust technology solutions that are up to the task and a 360-degree view of clients that provides a more comprehensive picture.”

How can specialist CRM create value for capital markets firms?

JM: “The complex workflows of capital markets businesses require specialist solutions that can process huge, disparate datasets and securely deliver actionable, revenue-generating intelligence. European regulation, such as MiFID II, requires banks to have robust systems in place that enable them to track how they are servicing their buy-side clients.

“Specialist CRM can provide a ‘one-stop shop’ for managing everything from business-wide client interactions to corporate access events, delivering a comprehensive, 360-degree view of clients in a regulated, compliant manner. But we’re not talking about traditional CRM here; rather, capital markets-specific platforms – business intelligence solutions that enable firms to maximise the revenue-generating opportunities from client interactions, increase efficiency and productivity, and demonstrate their value to clients.”

MP: “The right, purpose-built solution will also enable increased transparency, collaboration, and connected data and workflows across financial institutions – from global banks to boutique shops. As a centralised hub for managing client information, the platform will deliver prompted insights, which in turn drives more informed, consistent and profitable business, and smarter client engagement.

“The adoption of new technology can be a complex, protracted and expensive undertaking – but with the right technology partner and solution, it doesn’t have to be. Pre-packaged solutions and an accelerated delivery model can ensure rapid, seamless integration in weeks rather than months, at a fraction of the cost of custom-built platforms.”

Looking ahead, how should firms be approaching compliance when it comes to CRM in Europe’s capital markets?

JM: “In just over a year, there has been a marked shift in the capital markets landscape. Mobility and virtual accessibility are more important than ever, and data is our most valuable commodity. As the innovation curve progresses, vendors need to deliver more specialised, interoperable and relevant solutions to address the challenges capital markets professionals in Europe are facing – including being able to turn oceans of data into actionable insights.

“Although firms in the US and Europe have many of the same needs, it’s important to be attuned to the differences and nuances of these markets. Regulations will continue to shift and it is going to be imperative that end-users and vendors stay nimble in their approach to technology and, more specifically, CRM.”

The article highlights how the proliferation of API-led possibilities has led to a tremendous potential in shaping up the new open banking business models in the banking industry.

by Sanat Rao, Chief Business Officer and Global Head – Infosys Finacle

Sanat Rao, Chief Business Officer and Global Head – Infosys Finacle

While the concept of Open Banking has been around for some years, the industry mostly espoused it for the sake of regulatory compliance. However, in the wake of the pandemic, there has been a definitive and rapid uptake of open banking approaches and adoption globally. For instance, in Covid’s devastating aftermath, many beleaguered borrowers – especially small businesses and individuals – have found the Open Banking ecosystem to be an easier source of credit. By authorizing their banks and various other institutions to share their data with third-party providers in real-time, the borrowers are able to tap a wider supply of credit on more favorable terms. And this is just one of the many forces driving an accelerated adoption of Open Banking that has made it a key transformational lever of our world today.

Along with this growing appetite for Open Banking, the scope of Open Banking has also enlarged in recent times. The early days of Open Banking saw limited information sharing and little else; today, as participants gain in compliance and confidence, they are offering a wide portfolio of offerings, including credit, payment and accounting solutions, with plans to introduce savings and investment products as well.

Two factors are supporting this growth – first, a regulatory push in many countries and second, the proliferation of open APIs. The numbers speak for themselves – in the first two quarters of 2020, Open Banking API platforms globally grew 49 percent QoQ1. In the latest EFMA Infosys Finacle Innovation in Retail Banking Study, financial institutions said Open Banking APIs will have moderate to very high impact on banking business in 20212. APIs are a huge enabler of Open Banking ecosystems, facilitating both efficient exchange of data between participants and a variety of offerings on third-party/ non-banking channels.

“APIs are poised to change the future of banking. They have tremendous potential to enable innovations in Open Banking led business models, that are most relevant to banking industry going forward”

The Growing Impact of Open Banking

Open Banking is changing the very nature of banking and banking institutions. At the highest level, it is dismantling the “pipeline” universal banking model and enabling a ‘platform’ model in its place. Consequently, banks, which traditionally manufactured their products and distributed them through their own channels to their own customers, are now offering a variety of financial and non-financial products sourced from other providers or distributing their own products and services on third-party channels. They are doing this by working with their external ecosystem in a variety of ways:

Creating joint products with partners: Examples include Paytm which has introduced a co-branded credit card with CitiBank (and VISA), and Marcus by Goldman Sachs (and Mastercard) which has collaborated with Apple to launch the Apple Card.

Embedding non-banking products within customers’ primary journeys: DBS is a great example, with successful marketplaces for used cars, property, travel and utilities that allow it to enter the customer journey well before the customer starts looking for a banking product.

Collaborating with third parties to deliver (even) rival products: Once again, consider the example of Paytm, which is working with IndusInd Bank and ICICI Bank on high value fixed deposits and digital loans respectively.

Banks are constituting their platform businesses into the following innovative models:

Banking-as-a-Service (BaaS): BaaS is a recent development, with the model still in an early stage of adoption. Possibly, its most famous exponent is Goldman Sachs, which offers a set of APIs for creating bank accounts, making and tracking payments, and accessing the details of their activity. Developers can leverage the Bank’s infrastructure to build financial experiences into their own front-end applications3.

Marketplace: The marketplace model is gaining popularity with many banks creating marketplaces selling best-in-class financial and non-financial offerings in one place. In a way the marketplace is the opposite of the BaaS model because here, banks – much like departmental stores – aggregate the best options from other providers to fulfil even the non-banking needs of their customers. Apart from the earlier mentioned DBS Bank, U.K.’s Starling Bank runs a successful marketplace featuring a variety of services, such as wealth management, pension accounts and accounting software.

Utilities: A very interesting spin-off is the utilities model where big banks capitalize on their scale and efficiencies to provide back-end infrastructure services to other banks/ providers who then focus only on front-end activities. Payment utilities are now quite common, and the action is picking up in banking as well. For instance, ABN Amro Bank has set up Stater NV providing mortgage services, such as collection, communication and loan management, to other small lenders and fintech companies.

APIs – Enabling the digital ecosystem, and fostering the open banking paradigms

The above business models, while different on the surface, are all powered by APIs on the inside. APIs work at several levels throughout the open banking enterprise: specialized internal APIs or microservices enable banks to solve problems and create new value for clients; APIs help in customer acquisition and product expansion; an API led architecture can enable banks to innovate on par with the best companies in the world.

Therefore, the importance of a sound API strategy can never be overestimated. While developing their APIs, banks should pay heed to the following:

APIs must be based on good design principles and values, such as user-centricity, reusability and end-to-end process coverage.

The strategy should produce a strong operating model, as well as a monetization model that supports key business values.

If the business is to adopt an API-first approach for delivering new features in the future, it must design APIs for maximum reusability, today.

A modern API management platform with clear ownership is essential, as is a sound governance mechanism for executing internal and external APIs.

Last but certainly not least, the bank’s leadership should nurture an API culture throughout the organization. Having the right talent and training resources is critical, because over time, the bank must have multiple agile teams, working across the enterprise, developing APIs.

What’s next for APIs and Open Banking

After a slow start driven by regulatory compulsion, Open Banking has started to come into its own. It is a significant opportunity. Open banking is set to become mainstream and will pave way for new possibilities such as open finance. It will eventually foster market competition and innovation creating a win-win proposition for both financial institutions as well as for varied customer segments.

Platformification is a relatively new business model happening in FinTech that is enabling companies to lift-out entire operations and benefit from mutualisation.

Platformification is arguably the love child of increasing consumer demands, constantly changing industry regulations and the emergence of a range of next-generation technologies. In banking, for example, the never-ending regulatory standards have made it nearly impossible for smaller and medium-sized banks to invest in the technology that larger banks can comfortably (and quickly) afford to build in-house. As a result, platformification has quickly become a lifeboat for many banks that are determined to keep up with the digital transformation taking place in the industry, while also maintaining profitability.

Andrey Yashunsky, CEO and Founder, Prytek

BOPaaS (Business Operating Platform-as-a-Service) describes an advanced style of platformification that combines the standard benefits of managed services, with advanced access to cutting-edge technology and leading industry expert advice. Through its adoption, firms immediately benefit from a vertically integrated ecosystem: new technologies are designed and built at the heart of this ecosystem, which can then be cross-leveraged across all the businesses connected to it. This technological innovation, which is made possible through the mutualised R&D costs, helps to entirely transform business operations and job functions. A recent example is Karbon, a customer lifecycle management (CLM) product that is currently being offered by Delta Capita, a global managed services, technology solutions and consulting provider. The creation of Karbon was made possible through Prytek’s investment in Blackswan.

A hybrid approach to managed services

The integrated nature of BOPaaS is what makes it special: It is a hybrid of technology-based managed services and recommendations, engagement and interactions with industry specialists. Both are equally important. The development of state-of-the-art technology would be wasted if it wasn’t in the hands of an expert that knows how to effectively implement it in a way that can transform operations, and ultimately enhance the end-user experience. It is also important to know that it is not just the financial services industry that can benefit. For example, Prytek also operates BOPaaS in the cyber-education and HR sectors, and has plans this year to expand its reach further. Ultimately any industry that relies on human data input, or expensive centralised models, and is determined to improve client satisfaction could benefit from platformification and BOPaaS.

Driving technological and service innovation

These types of platforms are not only driving technological innovation, but they are also enabling firms to spend more time engaging with clients and strengthening business relationships. They are taking over the responsibility of the businesses’ non-differentiating operations as well as the responsibility to monitor for changing regulations, customer demands and digital transformation opportunities. By freeing up more time and effort of employees, BOPaaS customers can focus on the aspects of their business that makes them truly unique – which is almost entirely the way it delivers its customer service.