April 25, 2025

Every time you click, swipe, or tap, you’re participating in an evolving financial experience. The embedded finance market in GCC is expected to grow to USD 2 bn by 2030 at a 30% annual growth rate from USD 250 m in 2022 (Source: Roland Burger). Financial products are becoming invisible and being embedded into everyday platforms, or vice versa. And the fundamental change isn’t just technology—it’s how financial products are delivered and, more importantly, where they are delivered.

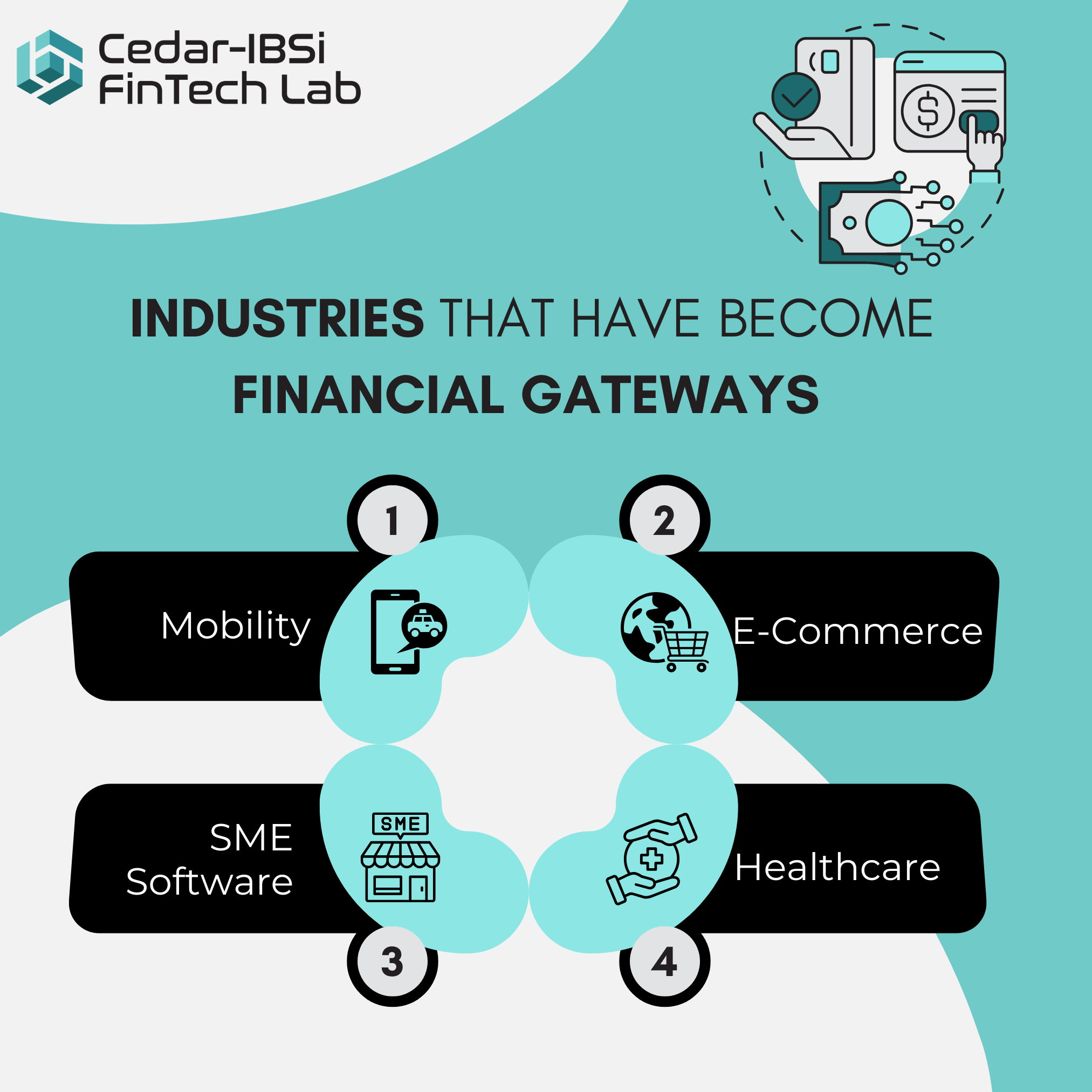

When Industries Become Financial Distribution Channels

What makes this evolution so powerful is that platforms are becoming the new distribution channels for financial services.

Take mobility platforms offering car loans to drivers. Or a software platform becoming the gateway for SME banking. Even a healthcare app embedding insurance into treatment plans. These industries have emerged from channels to ecosystems that customers trust and engage with daily.

Take mobility platforms like Uber or Ola, which now offer vehicle loans and insurance products directly to their drivers, often faster and more conveniently than traditional lenders. Shopify, originally an e-commerce enabler, has evolved into a powerful financial services hub, offering merchants embedded banking, lending, and payments through Shopify Capital. Zoho and Tally, popular among Indian SMEs, are increasingly integrating financial tools like invoice financing and payment reconciliation directly into their core accounting software.

Even healthcare apps are moving into this space — Practo and 1mg, for example, are exploring insurance partnerships that allow patients to finance treatments or access micro-insurance at the point of care. These industries have evolved from being mere service providers to trusted ecosystems that customers interact with daily, becoming natural gateways for financial products.

And here’s the reality: they’re doing a better job of capturing user attention than banks are.

Why Banks Can’t Sit This Out

Embedded finance changes the role of banks from financial product distributors to financial product enablers, manufacturers, and compliance layers. And unless banks adapt, they risk becoming invisible. The products may still be theirs, but the customer experience, the journey, the loyalty? That could belong to someone else.

The winners will be the banks that evolve:

- From product manufacturers to experience enablers

- From owning the customer interface to powering ecosystems from behind the scenes

- From chasing users to meeting them exactly where they are

It is imperative for banks to consider building the rails, the compliance layer, the intelligence and integrating them seamlessly into someone else’s digital experience.

The FinTech Opportunity: Build the Plumbing, Not Just the App

For FinTechs, the play is clear. The bigger opportunity lies in becoming the infrastructure layer—the rails and intelligence that power finance behind the scenes.

Think decision-making engines for marketplaces. Real-time credit embedded into platforms. Smart KYC workflows are triggered inside CRMs. This is where scale lives—and where future value will be built.

Case in Point: Mashreq’s Embedded Supply Chain Financing

We’re already seeing this play out in the GCC. In the UAE, Mashreq Bank has partnered with Invoice Bazaar to offer supply chain financing directly embedded into B2B ecosystems.

Instead of applying for credit separately, SMEs get access to working capital at the point of invoice generation. The underwriting decision is instant with a frictionless experience. Finance becomes part of the workflow, not a step outside of it. It’s finance reimagined to match the tempo of modern business.

What Leaders Need to Ask Now

For decision-makers in banks and FinTechs, this shift demands bold thinking and fast execution. Some questions to bring to the next leadership offsite:

- Are we integrated into the digital journeys our customers already live in?

- Can someone use our financial products without ever visiting our app?

- Are we seeing non-financial platforms as competition or as our next growth partners?

The Bottom Line: Finance Has to Follow the Customer

Here’s the truth: the future of finance is being built inside digital platforms where users shop, work, move, and live.

Those who embrace embedded finance will lead it.

Already, in sectors like retail, logistics, and healthcare, financial services are being woven directly into digital experiences — often invisibly to the end user. Andreessen Horowitz highlights that embedded finance has the potential to boost customer engagement and retention by up to 20% as financial services become part of native workflows. Staying relevant means adapting to a world where banking is a feature embedded seamlessly in digital workflows.