How AI Is Rewriting Lending Models

March 28, 2025

Lending decisions involve assessing both a borrower’s ability to pay (capacity to repay) and their willingness to pay (intention to repay), with lenders evaluating factors like income, credit history, and business plans to determine creditworthiness.

For decades, lending decisions have relied on a rigid framework of determining borrowers’ ability to repay with factors like credit scores, financial statements, and collateral. While effective for traditional borrowers, this model excludes millions of viable businesses and individuals who lack extensive credit histories. The rise of artificial intelligence (AI) and alternative data is forcing banks and fintech firms to rethink risk assessment, unlocking new opportunities in credit access while demanding a fundamental shift in underwriting strategies.

The Limitations of Traditional Credit Scoring

Credit scoring models—primarily driven by FICO frameworks — are backward-looking. They assess past borrowing behaviour but often fail to capture a borrower’s current and future financial health. This creates inefficiencies:

- Thin-file and no-file borrowers: Millions of small businesses and individuals lack sufficient credit history, making them invisible to traditional lenders.

- Static risk assessment: Traditional models rely on historical repayment data rather than real-time financial activity, missing dynamic changes in a borrower’s ability to repay.

- Collateral dependency: Many lenders still require collateral, excluding businesses that operate on cash flow rather than fixed assets.

With the explosion of digital transactions and AI-driven analytics, these limitations are no longer justifiable.

AI and Alternative Data: A New Approach to Credit Risk

AI is transforming credit risk models by incorporating alternative data—real-time financial behaviours, digital interactions, and business performance metrics that go beyond static credit reports. This approach allows for a more dynamic and inclusive assessment.

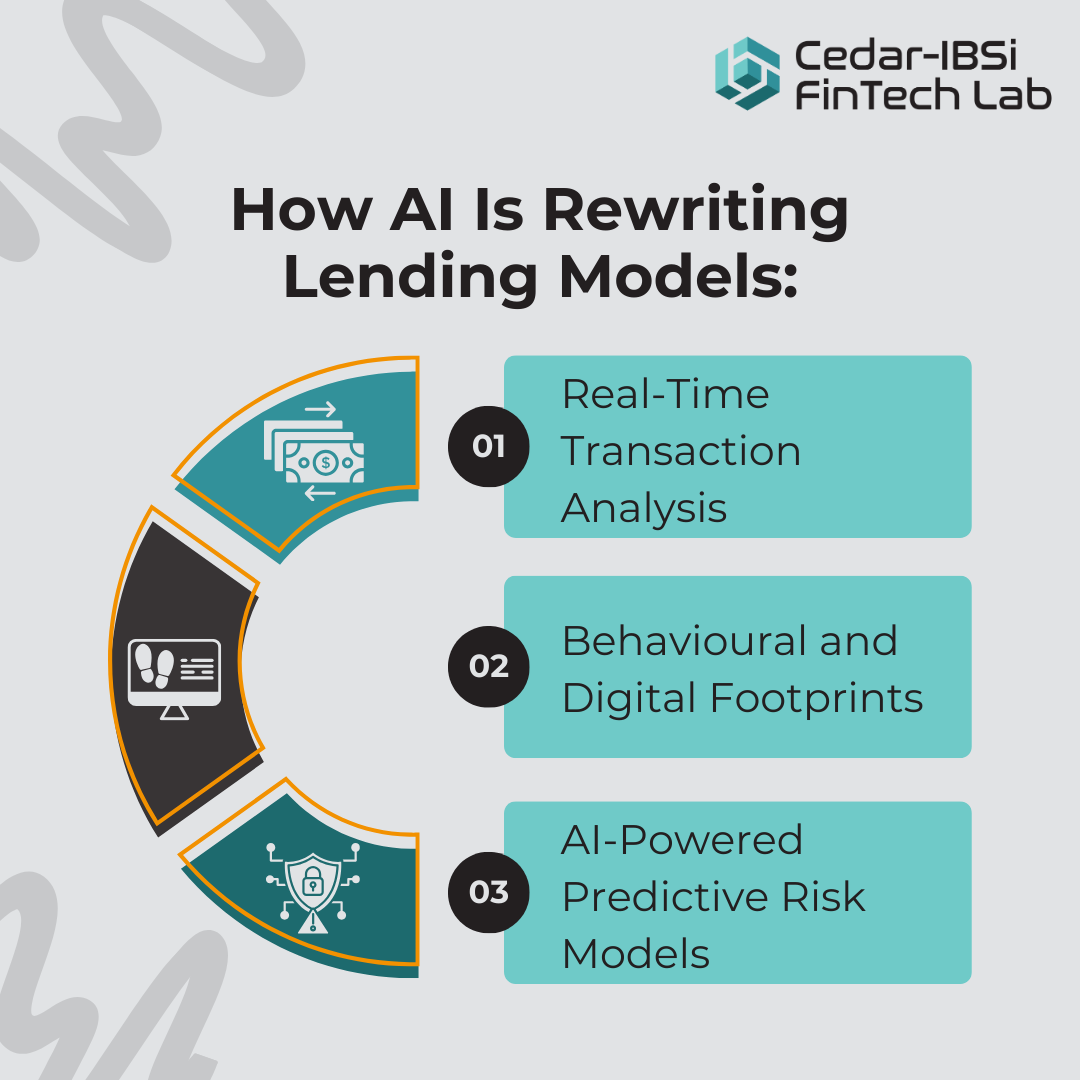

1. Real-Time Transaction Analysis

AI-powered models analyse continuous transaction flows from bank accounts, payment processors, and accounting software. Rather than focusing solely on past credit events, lenders can assess real-time cash flow, spending patterns, and revenue consistency. This is especially valuable for small businesses that may not have years of financial statements but demonstrate healthy, recurring income.

2. Behavioural and Digital Footprints

With machine learning, lending models can evaluate signals beyond traditional financial statements:

- E-commerce sales and platform reviews: A business’s performance on platforms like Shopify, Amazon, or Etsy can indicate stability and growth potential.

- Social media and customer engagement: Frequent, positive customer interactions and online presence suggest business vitality.

- Utility and rental payments: Regular, on-time payments for rent, electricity, and internet provide alternative indicators of creditworthiness.

3. AI-Powered Predictive Risk Models

AI excels at recognizing patterns that human underwriters and legacy algorithms miss. By analyzing billions of data points, AI-driven credit models can:

- Detect early warning signs of financial distress.

- Adjust risk scores dynamically based on real-time data.

- Identify low-risk borrowers that traditional models might reject.

For lenders, this translates into lower default rates, more precise risk pricing, and increased lending opportunities.

Birds Eye View on Middle East – Where is the adoption?

While banks are catching up, regulators are front running the push towards adoption. The Central Bank of Egypt (CBE) has permitted banks to incorporate alternative data sources into their credit scoring models, including customer behavior, social data, and financial and non-financial transactions. By leveraging such diverse data points, Egyptian banks can offer tailored financial products and expand credit access to underserved segments of the population.

Similarly, Mashreq Bank analyzes six months of bank statements using an advanced analytical engine. This process provides a comprehensive 20-line summary, offering insights into turnover trends, buyer and supplier relationships, payment regularity, and the frequency of bounced checks. By focusing on transactional data, Mashreq Bank gains a nuanced understanding of an SME’s operational dynamics and financial behavior, leading to more accurate credit evaluations and expanded access to financing for SMEs that might otherwise be excluded due to inadequate financial documentation.

Challenges and Considerations

While AI and alternative data offer a more inclusive and predictive lending model, they also introduce new complexities:

- Regulatory scrutiny: Financial regulators demand transparency in AI-driven credit decisions. Lenders must ensure their models are explainable and free from bias.

- Data privacy: The use of alternative data requires strict compliance with privacy laws like GDPR and CCPA. Borrowers must have clarity on how their data is used.

- Model accuracy and fairness: AI models can inadvertently reinforce biases if not trained on diverse, representative datasets. Continuous monitoring and recalibration are essential.

AI and alternative data are not just enhancing credit assessment—they are rewriting the rules of lending. Banks and fintechs that fail to embrace these innovations risk losing market share to data-driven competitors. The future of credit is:

- Proactive, not reactive—Lenders will assess borrowers based on real-time financial health, not outdated reports.

- Inclusive, not exclusive—AI-driven lending will extend capital to underrepresented small businesses and individuals.

- Dynamic, not static—Credit models will evolve continuously, adapting to economic shifts and borrower behaviors in real time.

Traditional credit scores are becoming obsolete. The question is: Will your institution adapt to the new era of lending, or will it be left behind?