Reimagining Corporate Banking: Meeting the Needs of SMEs in the Middle East and India

December 04, 2024

The Small and Medium Enterprises (SMEs) are the lifeblood of innovation and growth in the vibrant economies of the Middle East and India. However, despite their critical role, these businesses often face significant barriers in accessing the financial services they need to flourish. The Cedar-IBSi FinTech Lab, through the progress of its members have seen the transformative power of reimagining corporate banking to better serve SMEs.

Navigating Banking for SMEs and their challenges

SMEs in India and Middle East are incredibly diverse. However, they share common challenges – limited access to credit, cumbersome banking processes, and a lack of tailored financial products. Traditional banks with legacy systems and rigid structures often fail to meet the unique needs of SMEs.

- Credit Constraints: SMEs often find it difficult to secure financing due to stringent requirements and lengthy approval processes.

- Complex Banking: Traditional banking practices, such as onboarding and rigid credit scoring, hinder the SMEs’ growth.

- Limited Tailored Solutions: Generic banking products fail to address the specific needs of SMEs, leaving them underserved.

Reimagining Corporate Banking for SMEs

To unlock the full potential of SMEs, corporate banking must evolve to address their unique challenges.

- FinTech Partnerships: Collaborating with FinTechs can streamline processes, enhance credit scoring, and provide innovative solutions.

- Supply Chain Financing: By offering early payment options, banks can improve SMEs’ cash flow and strengthen supply chain relationships. This approach assists thin-file customers in securing credit.

- Embedded Finance: Integrating financial services into SMEs’ workflows can simplify their financial management and create more opportunities.

- Tailored Products: Developing flexible and scalable products, such as micro-loans and GST-flow-based lending (in India), can cater to SMEs’ specific needs. Flexible and scalable features to adapt to evolving nature of SMEs such as dynamic loan terms based on business cycles will help.

- Digital Transformation: Embracing digital banking can improve service delivery and empower SMEs with efficient financial tools.

Success Stories in Corporate Banking for SMEs

- Middle East Success Story: Mashreq Bank and Invoice Bazaar: Mashreq Bank in the UAE partnered with Invoice Bazaar, a FinTech startup, to it’s platform to offer early payment options for invoices, improving cash flow. The partnership has enabled Mashreq Bank to extend its reach to a broader SME customer base, providing them with much-needed liquidity.

- India’s Digital Revolution: ICICI Bank and InstaBIZ: ICICI Bank launched InstaBIZ, a comprehensive digital banking platform tailored for SMEs that offers a range of services, including instant overdraft facilities, business loans, and digital payments. Using AI and machine learning to streamline loan approvals and provide personalized financial solutions, it empowers SMEs to manage their finances more effectively and access a wider range of financial services.

- Regulatory Sandbox in Bahrain: The Central Bank of Bahrain (CBB) launched a regulatory sandbox in 2017 to foster FinTech innovation and to allow firms to test their solutions in a controlled environment with regulatory oversight. Tarabut Gateway, a FinTech company used the sandbox to develop and refine its open banking platform. This platform now facilitates secure data sharing between banks and FinTechs, enhancing financial services for SMEs.

- Regulatory Sandbox in India: The Reserve Bank of India (RBI) introduced its regulatory sandbox framework in 2019 to promote innovation in the FinTech sector. Cashfree, a participant of the program, tested its payment solutions to refine its products and ensure compliance with regulatory standards, ultimately providing more efficient payment solutions for SMEs.

By reimagining corporate banking, we can empower SMEs to thrive. By collaborating with FinTechs, offering tailored solutions, embracing digital technologies, and fostering innovation through regulatory sandboxes, we can create a banking ecosystem that supports the growth and success of SMEs.

The future of corporate banking lies in its ability to adapt and innovate. By addressing the unique needs of SMEs in the Middle East and India, banks can unlock significant economic potential, driving growth and prosperity in these regions.

A direct call to action for CXO bankers and FinTech founders: The time to act is now. Embrace the opportunities presented by digital transformation and FinTech innovation to better serve SMEs.

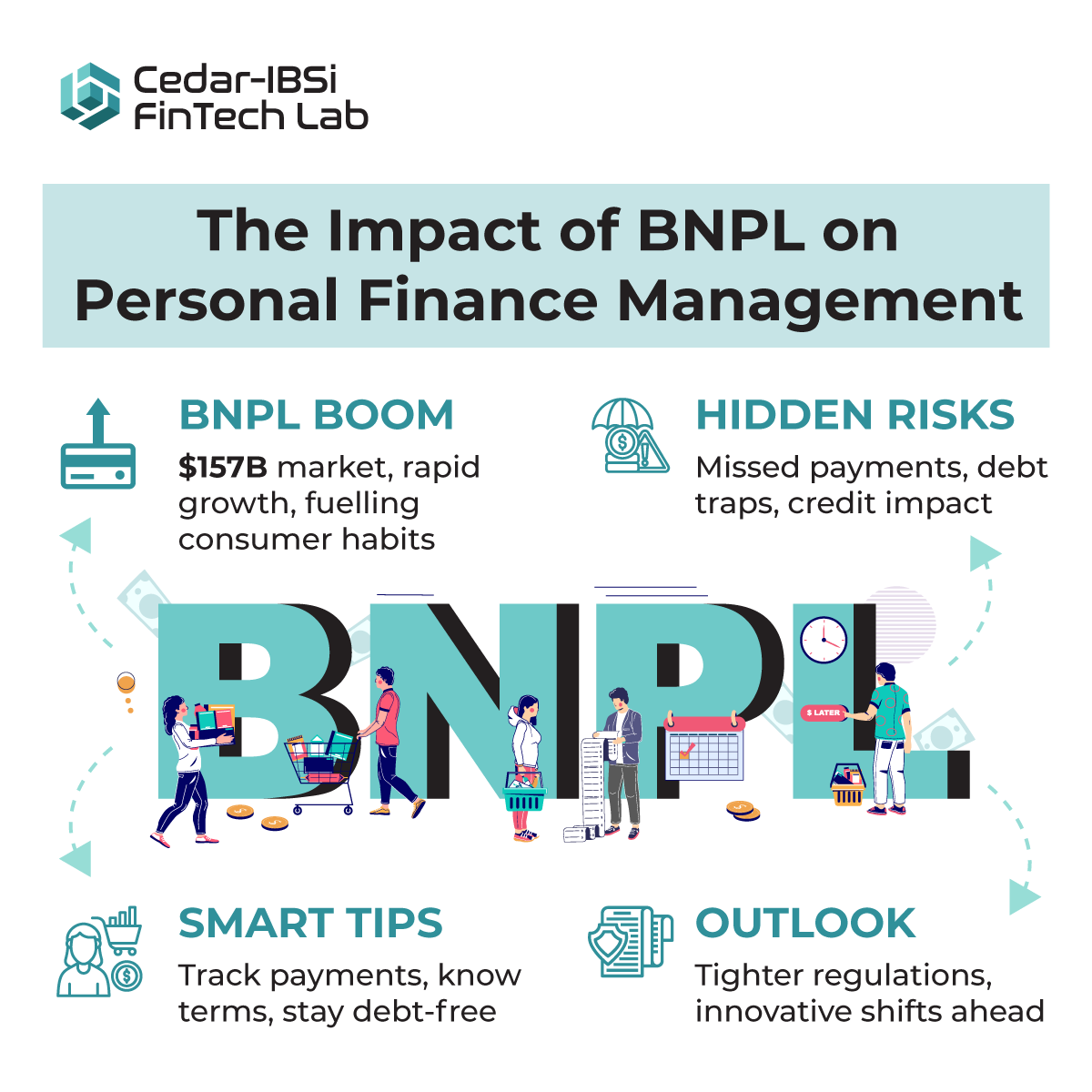

The Impact of “Buy Now, Pay Later” (BNPL) on Personal Finance Management

November 19, 2024

The rise of “Buy Now, Pay Later” (BNPL) services has revolutionized consumer finance, offering a convenient and flexible alternative to credit cards.. Platforms like Klarna, Afterpay, Affirm, and PayPal, enable a transformative way for people to make purchases and spread payments over several weeks or months, often without interest if paid on time.

The appeal is evident: convenience, flexibility, and the psychological ease of delaying payments. However, beneath this facade, BNPL also brings financial risks and challenges that require careful management and strategic thinking, especially in today’s fast-evolving digital economy.

Explosive Growth and Consumer Adoption

BNPL’s growth has been staggering. In 2023, the market was valued over $157 billion, projected to grow at a CAGR of nearly 25% over the next five years. E-commerce platforms have embraced BNPL, with over 60% of online merchants offering these options at checkout. In Australia, for example, BNPL transactions have become so pervasive that nearly 30% of online shoppers have used BNPL services at least once in the past year. In the U.S., reports indicate that BNPL accounts for over $100 billion in annual spending—a clear indication of how embedded these services have become in consumer habits.

This surge in BNPL adoption is driven by convenience, seamless integration into the checkout process, and strategic partnerships with major retailers. This is an attractive option, especially for younger generations like Millennials and Gen Z, who prefer to avoid traditional credit cards.

For merchants, BNPL boosts conversion rates and average ticket sizes. According to research from PYMNTS.com, merchants have observed a 20-30% increase in conversion rates and a 30-50% uptick in average ticket size when BNPL options are offered.

Drawbacks of BNPL

However, BNPL services come with potential drawbacks. One major concern is the risk of debt accumulation. A significant portion of BNPL users fall behind on payments, negatively impacting their credit scores. A study by Credit Karma in early 2023 revealed that 34% of BNPL users reported falling behind on at least one payment, and 72% of those who missed payments saw a negative impact on their credit scores.

The ease of use and perceived affordability of BNPL can lead to impulse spending, making it difficult to track overall spending and manage cash flow.

Another issue is the lack of regulatory oversight as compared to credit cards. However, with the rapid adoption of BNPL, financial regulators in regions like the United States, Australia, and the European Union are beginning to scrutinize these platforms.

Managing BNPL Responsibly

Given the growing integration of BNPL in everyday financial transactions, it’s crucial for consumers to use these services wisely. Here are some key strategies for managing BNPL responsibly:

- Track All BNPL Obligations: Use budgeting apps or financial tools to avoid missed payments.

- Treat BNPL Like Credit: Approach BNPL commitments with caution, as a traditional loan along with its total financial obligation.

- Avoid Overlapping Instalment Plans: Juggling multiple BNPL payments can lead to cash flow issues.

- Review Terms and Conditions: Understand the fees and potential penalties before agreeing to a BNPL plan.

As BNPL continues to grow in popularity, financial education becomes crucial. Consumers should be aware of the implications and use these services responsibly.

For FinTech founders, bankers, and technology vendors, the BNPL trend presents a dual opportunity: to innovate and cater to evolving consumer needs and foster responsible lending practices.

The future of BNPL likely involves tighter regulations, data-driven credit assessments, and innovations designed to empower consumers.